business resources

India Data Center Market: Comprehensive Analysis and Investment Outlook (Part 1)

26 Jan 2026

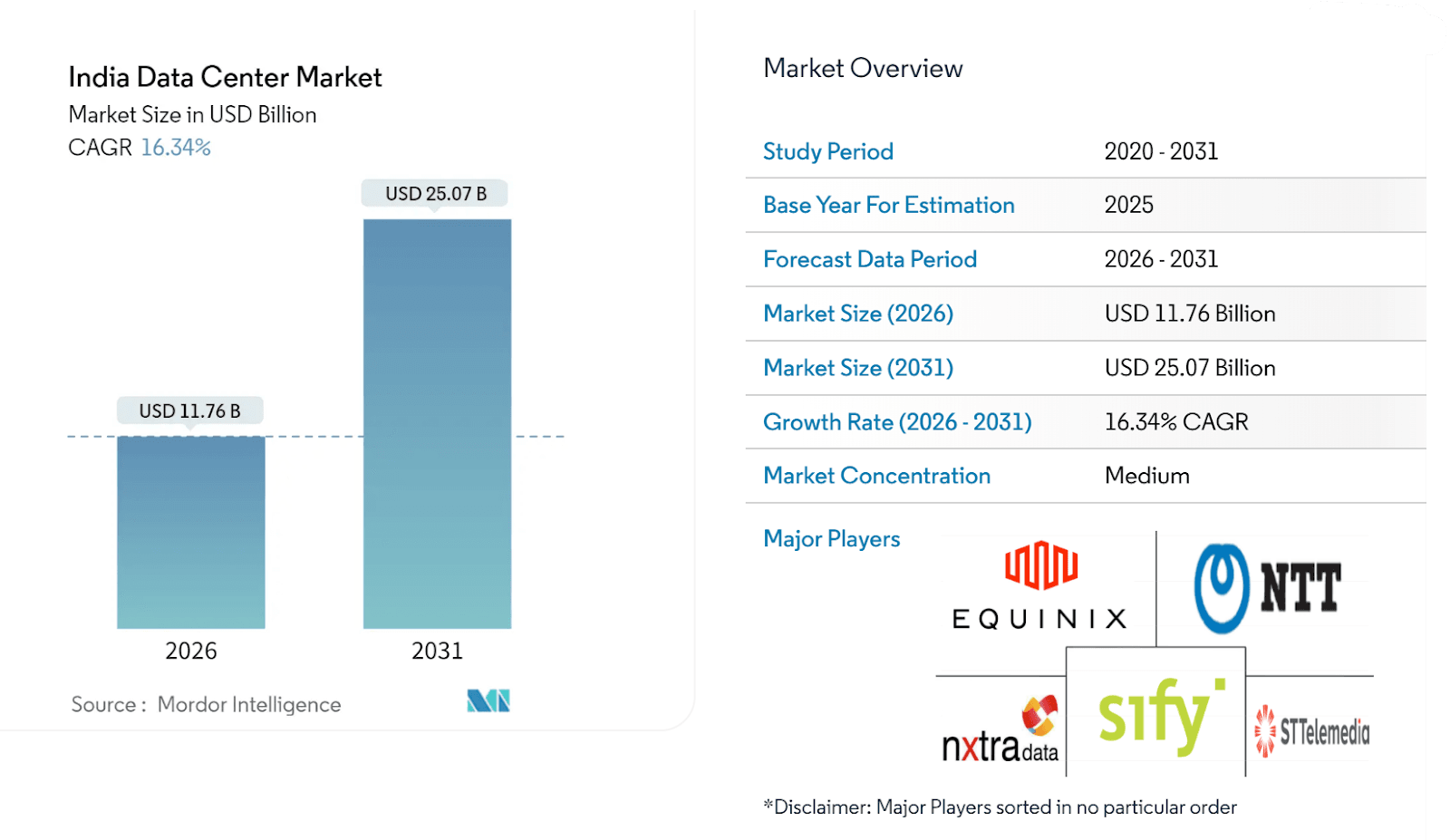

India's data center market is experiencing explosive growth, reaching USD 11.76 billion in 2026 with operational capacity of nearly 2 gigawatts. The sector is being propelled by a compelling investment thesis: India generates 20% of global data but stores only 3% locally, a massive gap that regulatory mandates and AI adoption are forcing closed.

This disparity, combined with new data localisation laws and surging AI workloads, is creating investment demand that far exceeds current supply. By 2031, analysts project the market will reach USD 25.07 billion at a 16.34% CAGR, with operational capacity expanding fivefold to 9.2 gigawatts. Real estate investment alone is expected to exceed USD 5.7 billion in 2026.

The Investment Case: Scale and Velocity

The numbers tell a compelling story. The market expanded from USD 10.1 billion in 2025 to approximately USD 11.8 billion in 2026, 16% year-on-year growth driven by hyperscale cloud demand, regulatory compliance, and AI infrastructure buildout.

Operational capacity reached 1.5–1.6 GW in 2025 after adding nearly 400 MW, India's largest annual commissioning to date. For 2026, industry forecasts point to another 200–250 MW addition, bringing total capacity to the 1.85-2.0 GW range. But the real transformation happens 2026–2030, when projections suggest India could hit 8–9 GW, requiring USD 25–30 billion in cumulative infrastructure investment.

What makes this particularly attractive is the compute intensity shift. IT load capacity is projected to jump from 4.5 GW in 2025 to over 12 GW by 2030, a 20%+ CAGR driven by AI rack density, GPU deployment, and high-performance workloads. This isn't just capacity expansion; it's a structural shift in facility economics.

The capital intensity is significant: each megawatt now requires INR 60–70 crore (USD 7–8 million) including land, electrical infrastructure, cooling, and specialised systems. This positions data centers among India's most capital-intensive infrastructure plays, comparable to the telecom tower boom of the early 2000s but with substantially higher returns per unit.

Market Fundamentals: Why India, Why Now

The Regulatory Catalyst

India's Digital Personal Data Protection Act (DPDPA) and Reserve Bank of India mandates have transformed data localisation from optional to mandatory for sensitive sectors. The BFSI sector alone accounts for 33% of data center demand, creating non-cyclical, compliance-driven revenue streams less vulnerable to economic downturns.

The Global Arbitrage

India maintains structural cost advantages: construction costs around USD 7 per watt (among the world's lowest) and electricity prices roughly 20% below U.S. rates. Combined with infrastructure status enabling preferential financing and faster approvals, India offers compelling unit economics for operators.

The Connectivity Hub

Mumbai and Chennai serve as international data gateways with 17 subsea cables and 14 landing stations, providing high-capacity, low-latency global connectivity. This positions India not just as a domestic market but as a regional hub for ASEAN and Middle East traffic.

The Utilisation Story

Capacity utilisation jumped from 82% in 2019 to 93% in 2023, while operator revenues grew at 25% CAGR from FY2017 to FY2023. These aren't speculative builds—capacity additions are demand-driven, reducing investment risk.

Investment Highlights: Key Metrics

- Market Size: USD 11.76 billion (2026) → USD 25.07 billion (2031)

- CAGR: 16-17% (among highest globally)

- Capacity: 1.7-2.0 GW (2026) → 8-9 GW (2030)

- IT Load Growth: 4.5 GW (2025) → 12.5 GW (2030) at 20%+ CAGR

- 2026 Infrastructure Investment: USD 5.7 billion

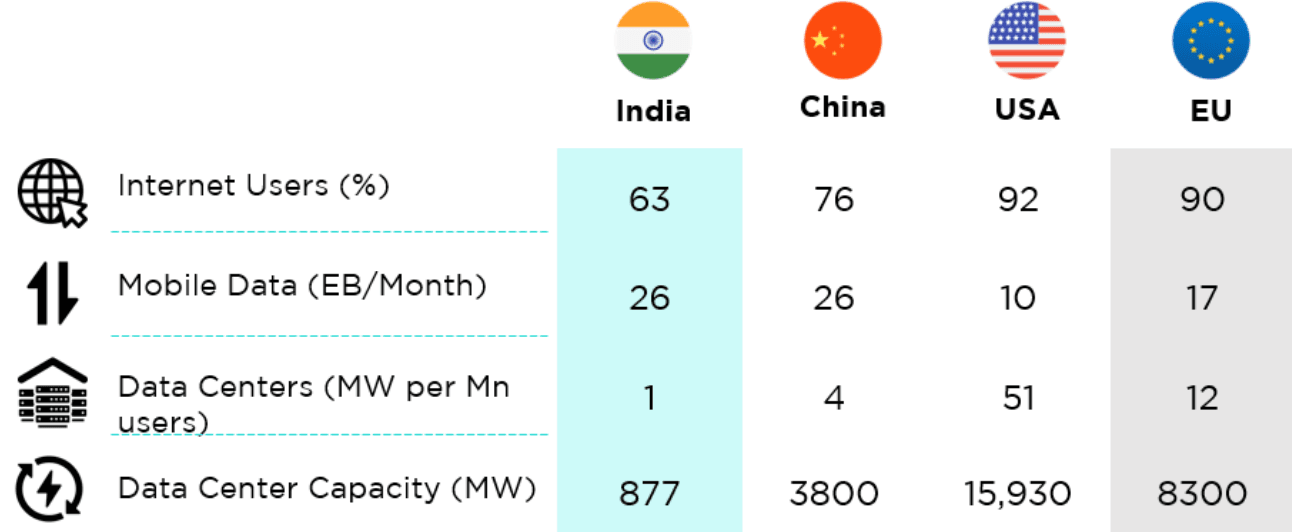

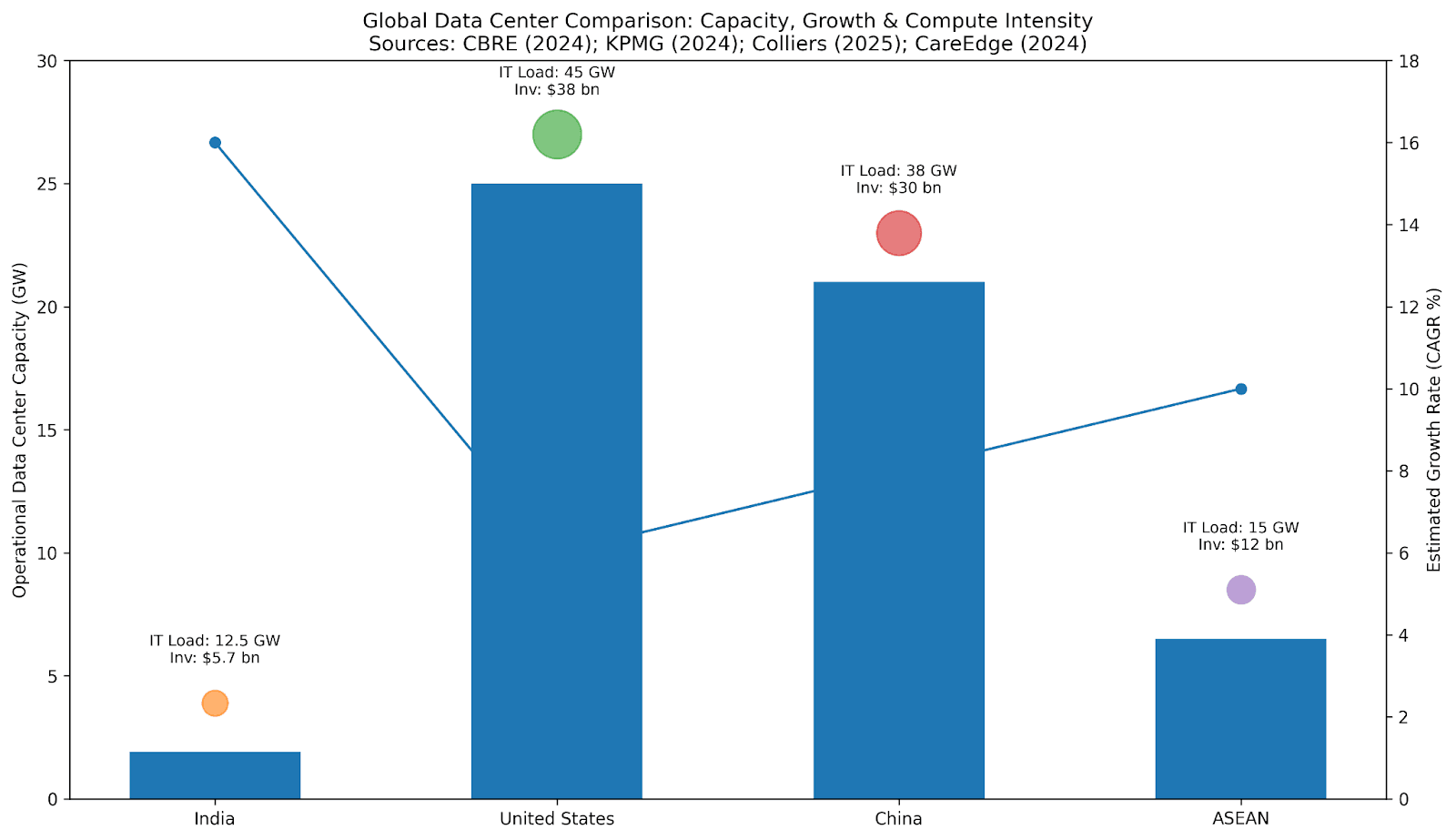

- Global Context: India remains massively under-scaled vs. U.S. (25 GW), China (20-22 GW), ASEAN (6-7 GW)

Growth Drivers Creating Investment Momentum

- Digital India & AI Imperative: Government allocation of ₹10,371 crore for 10,000 GPUs signals serious infrastructure commitment, creating anchor demand for AI-optimized facilities.

- Data Sovereignty Requirements: DPDPA and RBI mandates force domestic storage across BFSI, healthcare, telecom, and government—creating predictable, long-term demand.

- OTT & Edge Expansion: With 966 million internet connections and growing rural penetration, latency-sensitive applications are driving edge data center deployment in Tier-2 cities.

- Renewable Transition: Long-term renewable PPAs (10-20 years) provide price stability, transforming sustainability from cost center to competitive advantage and hedge against energy volatility.

Market Trends Reshaping the Landscape

- Supply-Demand Imbalance: Capacity expansion isn't keeping pace with data generation, creating sustained pricing power for operators.

- Market Diversification: New entrants are breaking incumbent dominance, creating M&A opportunities and partnership potential.

- High-Density Economics: AI workloads driving racks from 5-10 kW to 50-120 kW, requiring liquid cooling and advanced infrastructure, raising barriers to entry while improving economics for sophisticated operators.

- Geographic Winners: Mumbai, Hyderabad, Chennai, and Pune dominate due to connectivity and power reliability, but Tier-2 cities offer compelling cost arbitrage for edge and overflow capacity.

State Competition: The Policy Advantage

State-level competition for data center investment is creating attractive incentive packages:

| State | Strategic Advantage | Investment Draw |

|---|---|---|

| Maharashtra | Highest capacity, subsea cable density | Capital subsidies, duty exemptions |

| Telangana | Tech ecosystem, fast-track approvals | Power tariff incentives, progressive policy |

| Andhra Pradesh | Data Centre Policy 4.0 | Concessional land, 200+ MW pipeline |

| Tamil Nadu | Coastal connectivity, cable stations | Infrastructure support, business reforms |

| Gujarat | Renewable energy access | Green DC focus, tariff support |

| Uttar Pradesh | NCR proximity | Large pipeline, AI-campus focus |

State-level policies increasingly determine capacity allocation. While Maharashtra and Tamil Nadu lead current supply, Andhra Pradesh, Telangana, Gujarat, and Rajasthan are emerging destinations with lower costs and better renewable access.

Tier Classification: Understanding Risk-Return Profiles

| Tier | Uptime | Redundancy | Growth | Primary Market |

|---|---|---|---|---|

| Tier I-II | ≤99.75% | Single path | Declining | Non-critical, cost-sensitive |

| Tier III | 99.982% | N+1 maintainable | Market standard | Enterprise, cloud, telecom |

| Tier IV | 99.995% | 2N/2N+1 fault-tolerant | 20-22% CAGR | BFSI, healthcare, government, AI |

Tier IV growth at 20-22% CAGR reflects regulatory requirements and AI sensitivity—these command premium pricing and longer-term contracts, creating more stable cash flows.

Investment Implications

- For Infrastructure Investors: This is early-stage positioning in a multi-decade buildout. The 2026-2030 window represents the initial acceleration phase, not the peak. USD 25-30 billion in required infrastructure investment over four years creates substantial deployment opportunity.

- For Private Equity: Market diversification and new entrants create roll-up and consolidation opportunities. Tier-2 expansion offers geographic arbitrage plays with lower entry costs.

- For Strategic Investors: Vertical integration opportunities abound—data centers + renewable power + connectivity models are emerging as competitive moats (see AdaniConneX). First-mover advantage in AI-optimized facilities creates switching costs.

- For REITs and Yield Investors: Infrastructure status enables long-tenor financing. Regulatory-driven demand reduces cyclicality. Renewable PPAs provide inflation hedges. Mission-critical nature creates sticky, predictable cash flows.

Risk Factors and Mitigation

- Power Reliability: Grid delays are the primary execution risk. Mitigation: Target states with proven grid capacity; build captive generation capability.

- Water Scarcity: Growing constraint in urban markets. Mitigation: Closed-loop cooling, treated water sourcing, Tier-2 geographic diversification.

- Talent Shortage: Specialised skills in short supply. Mitigation: Training partnerships, automation, operational excellence programs.

- Regulatory Fragmentation: State-level policy variability. Mitigation: Multi-state portfolio diversification, strong government relations capability.

The Bottom Line

India's data center market offers a rare combination: structural demand drivers, regulatory tailwinds, attractive unit economics, and massive under-capacity relative to data generation. The 16%+ CAGR to 2031 understates the opportunity, compute intensity growth at 20%+ CAGR suggests superior economics for well-positioned operators.

This isn't a trade; it's a multi-year infrastructure thesis. The winners will be operators and investors who combine execution capability, power strategy, regulatory expertise, and sustainability credentials. With over USD 20 billion in announced commitments and government backing through the IndiaAI Mission, the capital is committed. The question isn't whether India's data center market will scale—it's who will capture the value.