resources

Insurers Vs. Inflation: Why Your Premiums Keep Rising

12 Sept 2025

Are you confused about why your insurance premiums keep going up each year? Inflation pushes prices higher, and that includes the cost of many insurance policies. This blog will explain how inflation affects coverage types.

How Inflation Impacts Insurance Premiums

Inflation raises the cost of materials, labor, and services. This leads to higher insurance premiums for everyone.

Rising Costs of Repairs and Replacements

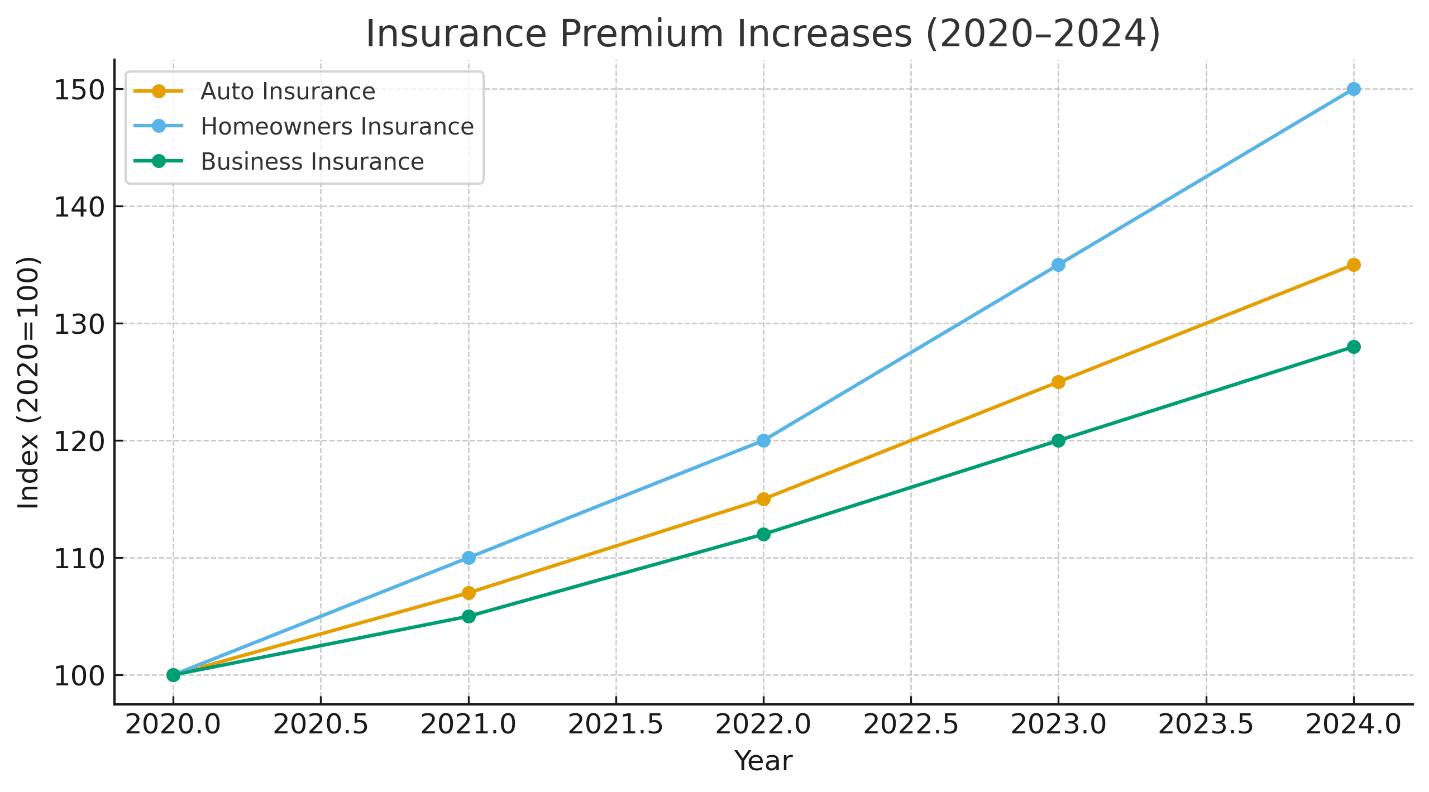

Car parts, building materials, and labor have all gotten more expensive in recent years. The U.S. Bureau of Labor Statistics reports a 19 percent increase in vehicle repair costs from 2021 to 2023.

Lumber prices for homes surged during the pandemic and many supplies still cost more than before. Higher repair bills force insurers to pay out larger claims after accidents or damages.

Many replacement items now take longer to arrive because supply chains face delays and shortages—from auto glass to roofing shingles. Shortages make repairs harder and can cause costs to climb even higher each year.

As a result, insurance premiums often go up so companies can cover these larger payouts.

Average collision repair costs hit $5,243 in early 2023, says CCC Intelligent Solutions.

Increased Frequency of Severe Weather Events

Hurricanes, floods, and wildfires happen more often now than before. In 2023, the United States saw 28-billion-dollar weather disasters. Storms damage homes and cars in many states each year.

After every major event, insurers pay huge claims to fix or replace property. Insurance companies pass these higher costs on to customers by raising premiums.

Climate change makes strong storms and heavy rainfall more common. More people file claims after such events, which pushes costs up for everyone who pays for insurance coverage. This trend affects both homeowners insurance and auto insurance rates across the country.

Effects on Different Types of Insurance

Insurance costs can change based on type. Homeowners and auto insurance might rise due to inflation, affecting coverage options.

Homeowners Insurance

Homeowners insurance has become more expensive lately. The price of building materials and labor keeps rising. Lumber prices went up by 40 percent in 2021, which made repairs cost much more.

Storms and wildfires damaged thousands of homes in recent years, leading to more claims. Insurance companies raise premiums to cover these bigger bills.

A standard policy may not fully cover new repair costs if inflation is high. Many people find their coverage does not match the true value to rebuild their home after a loss. Checking your policy each year can help you keep up with changes in value and cost.

Higher risks from weather events also push rates higher for many homeowners across the country.

Auto Insurance

Homeowners insurance faces pressures from inflation. Auto insurance also feels these effects. Costs for car repairs and parts are rising. Many accidents lead to increased claims, which raises premiums.

Severe weather events also cause significant damage to cars. They lead to costly repairs and replacements. As a result, auto insurers adjust their rates higher. As insurers raise rates, drivers can explore alternatives like pay-as-you-go plans (detailed in this usage-based insurance comparison article) or compare traditional policies to identify affordable options.

Keeping track of discounts or bundling policies can help manage these costs better.

Managing Rising Insurance Costs

Rising insurance costs can be tough to handle. You can save money by bundling your policies or looking for discounts.

Bundle Policies and Seek Discounts

Bundling insurance policies can save you money. Discounts are often available when you combine different types of coverage.

- Many insurers offer discounts for bundling. You can combine home, auto, and other policies with the same company. This often leads to lower overall premiums.

- Always ask about available discounts. Some companies provide lower rates for safe driving or paying your premium in full. Taking time to check these options helps reduce costs.

- Review your coverage regularly. Make sure your current policies match your needs and budget. Adjusting them can help lower your premiums.

- Use online tools like Loya Insurance to compare prices and policy features. These platforms let you evaluate multiple insurers side-by-side, helping you find the best deals for bundled policies. Some websites even suggest discounts based on your profile.

- Contact your insurance agent yearly to discuss savings options. They can inform you about new discounts or policy changes that could save you money.

Managing rising costs is crucial in today’s economy. Understanding how inflation affects insurance is important at this time.

Review and Adjust Coverage

Insurance coverage should match your needs. Regular reviews can help you save money.

- Reassess your home’s worth. Your home's value can change over time. Higher values may mean higher premiums if not updated.

- Check your auto insurance limits. If you drive less or have an older car, adjust your coverage to fit.

- Look for overlapping policies. You might have similar coverage in different places. Remove one to lower costs.

- Evaluate extras you don’t use often. Consider dropping items like rental car coverage if they are unnecessary.

- Update personal belongings lists regularly. Keeping track ensures proper protection and could lower costs if values decline.

- Consider raising deductibles wisely. A higher deductible usually means lower monthly payments but be sure you can pay it in case of a claim.

Finding the right balance in coverage helps manage rising costs effectively, which leads us to how discounts and bundling can further ease financial strain on your premiums.

Conclusion

Inflation affects our daily lives. It also hits insurance premiums hard. Higher repair costs and more extreme weather events push prices up. To keep your rates in check, consider bundling policies or looking for discounts.

Always review your coverage to ensure it meets your needs without breaking the bank. Stay informed and proactive about your insurance choices.