business resources

The State of AI in 2025: Key Trends Shaping the Future of Artificial Intelligence

CB Insights' "State of AI” Report highlights a $79.2 billion surge in AI funding in 2024, a 27% rise. Generative AI firms secured 40% of investments, with OpenAI, xAI, and Anthropic leading. AI’s rapid adoption across industries is driving innovation and shaping key trends for 2025.

In 2024, the artificial intelligence (AI) sector experienced unprecedented expansion, with global funding for AI and cloud companies in the U.S., Europe, and Israel reaching $79.2 billion—a 27% increase from the previous year. Notably, generative AI firms attracted approximately 40% of this investment, underscoring the heightened interest in AI-driven innovations. Leading the funding surge were companies like OpenAI, which secured $6.6 billion, Elon Musk's xAI with $6 billion, and Anthropic, which obtained $4 billion from Amazon.

This surge in investment reflects the growing integration of AI across various industries, from healthcare to finance, where AI applications are enhancing efficiency and driving innovation. The "State of AI Report: 6 Trends Shaping the Landscape in 2025" by CB Insights delves into these developments, highlighting key trends that are poised to influence the future trajectory of AI.

6 trends shaping the landscape in 2025

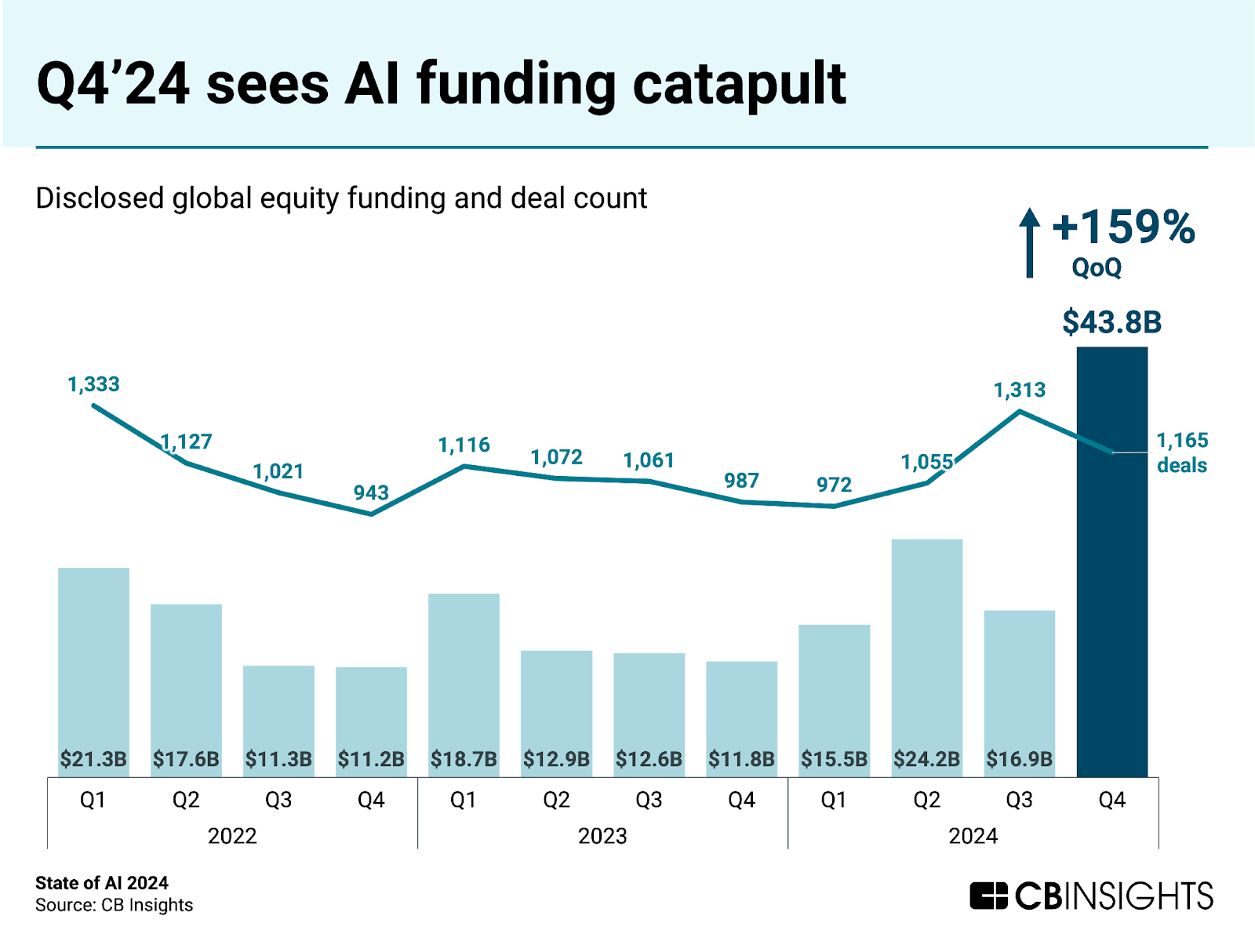

1. Massive deals drive AI funding boom

In 2024, private AI companies raised a record-breaking 100.4billion globally, reflecting the immense investor enthusiasm surrounding AI.The fourth quarter alone saw funding surge to 43.8 billion, more than 2.5 times the previous quarter’s total. This growth was largely driven by mega-rounds, defined as deals worth $100 million or more, which accounted for 80% of Q4 funding and 69% of the total funding for the year.

Thirteen deals exceeded $1 billion, with the majority of these investments directed towards AI models and infrastructure players. Notably, OpenAI, xAI, and Anthropic secured four of the five largest funding rounds in 2024, underscoring the high costs associated with developing frontier AI models. These costs span hardware, staffing, and energy requirements, which are critical to advancing AI capabilities.

Despite the dominance of mega-rounds, early-stage deals remain a significant part of the AI funding landscape. Nearly 74% of AI deals in 2024 were early-stage, a trend that has been rising since 2021. This indicates that investors are keen to capitalise on the next wave of AI innovation by backing startups at the ground level.

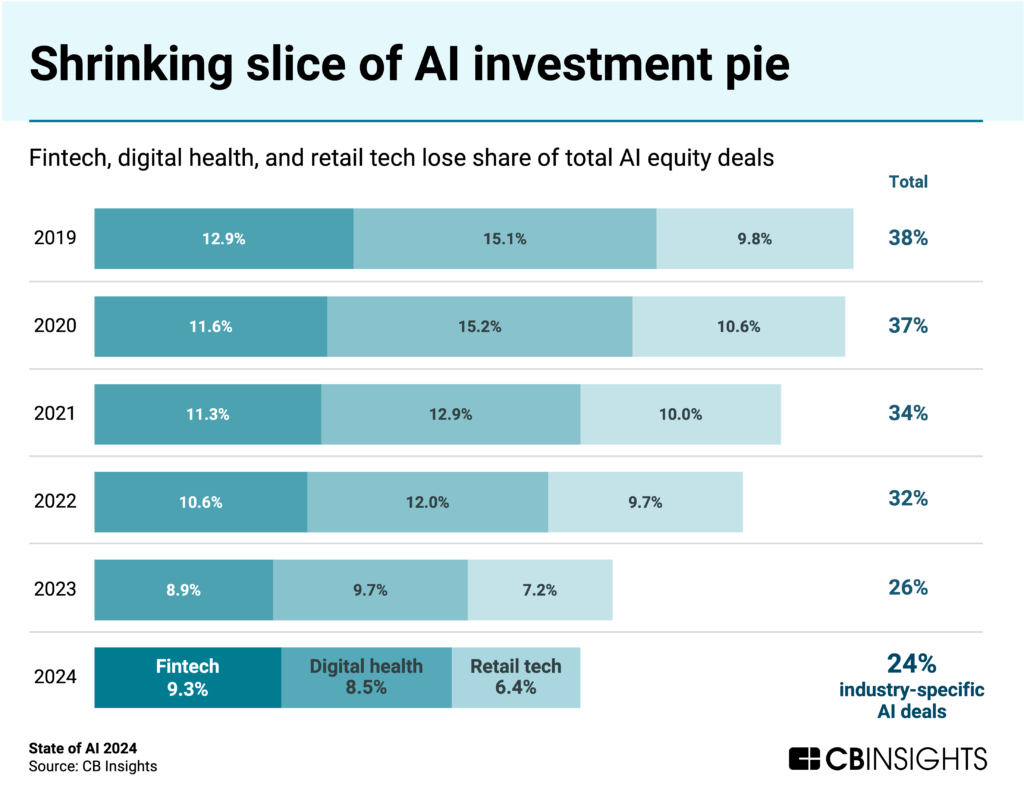

2. Industry tech sectors lose ground in AI deals

While AI continues to permeate various industries, certain sectors are seeing a decline in their share of AI-related deals. Vertical tech areas such as fintech, digital health, and retail tech accounted for just 24% of AI deals in 2024, down from 38% in 2019. This shift suggests that investors are increasingly prioritising companies focused on AI infrastructure and horizontal applications, particularly in light of the generative AI boom.

The data reveals that while AI companies are becoming more prominent within these verticals, their growth has not been sufficient to offset the broader trend. Instead, the focus has shifted towards foundational AI technologies that can be applied across multiple industries, reflecting a belief that the economic benefits of AI will primarily accrue to those building the underlying infrastructure.

Key Observations

- AI deal volume remains above 4,000 annually since 2021.

- Fintech and digital health investments are at multi-year lows.

- AI infrastructure and horizontal applications are attracting greater investor interest.

- Mega-deals indicate confidence that economic benefits will accrue to those building AI foundations.

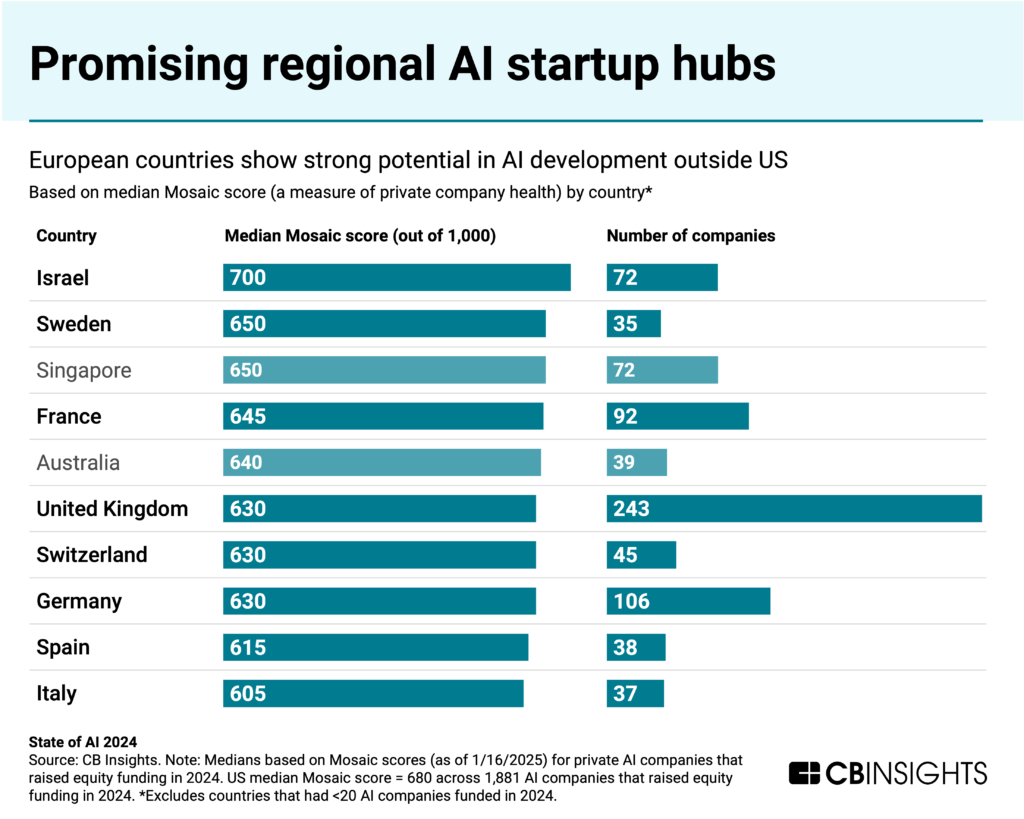

3. Outside of the US, Europe fields high-potential AI startup regions

The United States continues to dominate AI funding, capturing 76% of global investments in 2024. However, deal activity is more evenly distributed, with US startups accounting for 49% of deals, followed by Asia (23.2%) and Europe (22.9%).

Europe, in particular, is emerging as a hub for high-potential AI startups. According to CB Insights’ Mosaic scores, which measure the health and growth potential of private tech companies, European countries dominate the top 10 rankings outside the US. Israel leads the pack with a median Mosaic score of 700, thanks to its strong technical talent pool and established startup ecosystem.

Early-stage deals are driving activity in Europe, accounting for 81% of deals in 2024—a seven-year high. The European Union has identified scaling startups as a top priority, emphasising the need for increased late-stage private investment to remain competitive globally.

Key Regional Insights

- Europe accounted for 22.9% of global AI deals in 2024.

- Israel leads with the highest median Mosaic score (700).

- Early-stage investment in European AI startups is at a 7-year high (81% of deals).

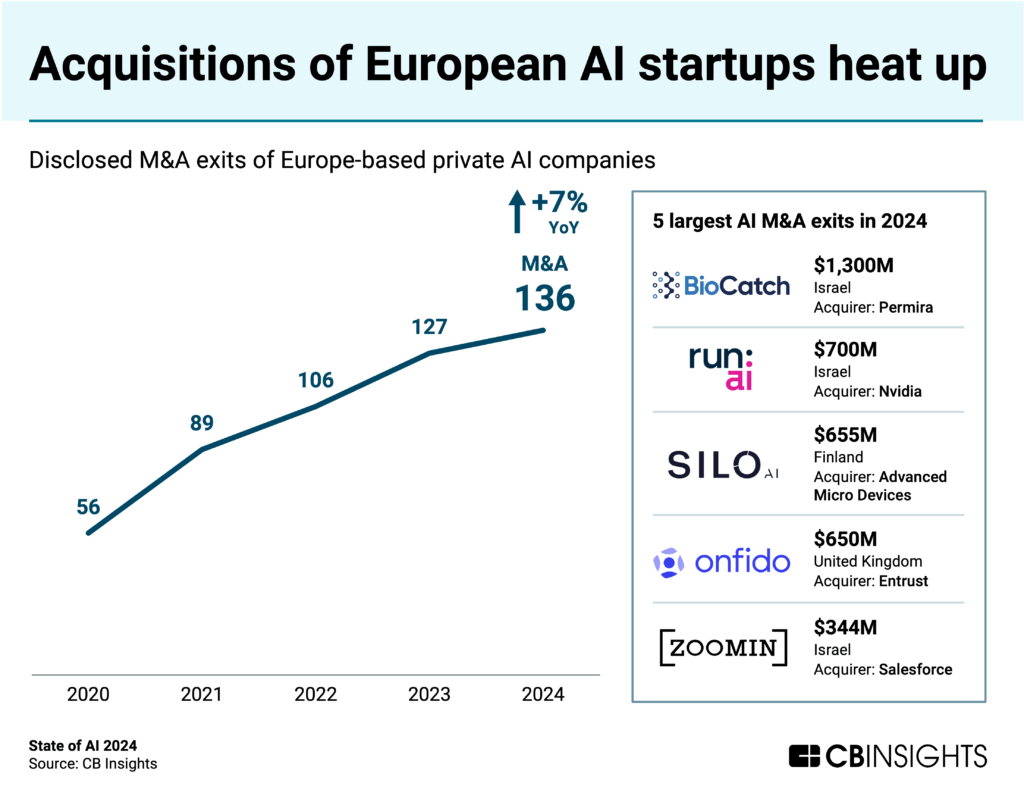

4. AI M&A activity maintains momentum

Mergers and acquisitions (M&A) in the AI sector remained robust in 2024, with 384 exits recorded—just shy of the previous year’s record of 397. Europe-based startups were particularly active, representing over a third of global AI M&A activity. This marks the fourth consecutive year of rising acquisitions in the region.

The UK led European M&A activity with 32 deals, followed by Germany (18), France (16), and Israel (12). Meanwhile, major US tech companies such as Nvidia, Advanced Micro Devices, and Salesforce were involved in some of the largest deals of the year as they sought to integrate AI capabilities into their offerings.

Key M&A Insights

- Europe accounted for over a third of global AI M&A deals.

- The UK led European AI acquisitions with 32 deals, followed by Germany (18), France (16), and Israel (12).

- US-based acquisitions grew by 16% year-on-year (188 deals).

- Nvidia, Advanced Micro Devices (AMD), and Salesforce were among the most active acquirers, integrating AI technologies into their portfolios.

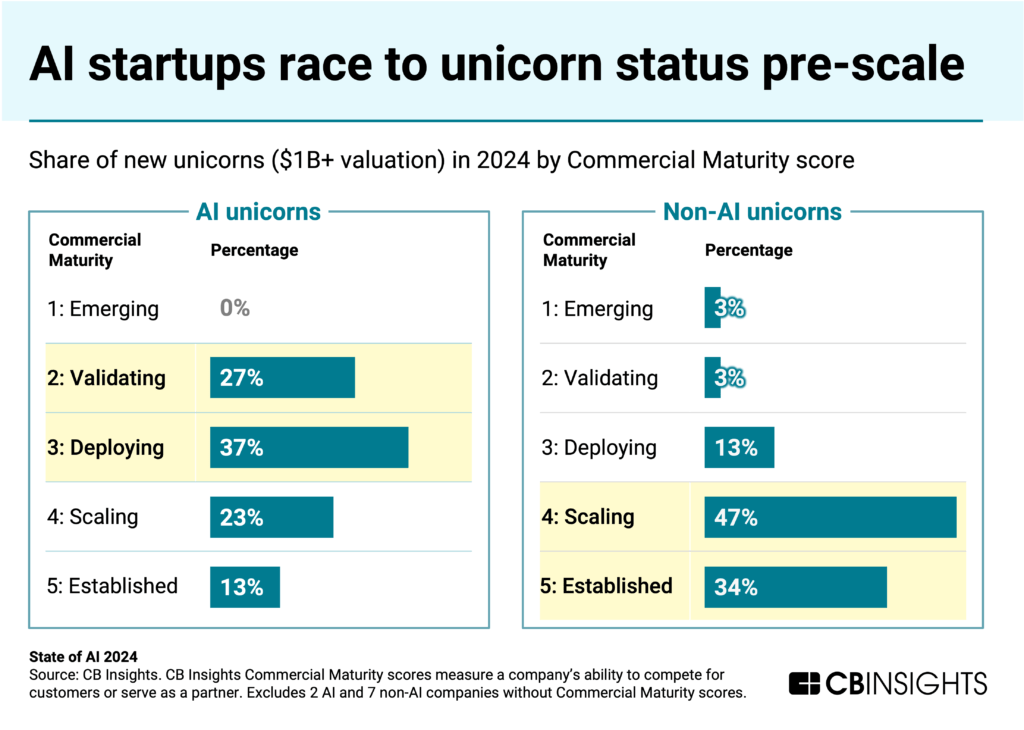

5. AI startups race to $1 billion+ valuations despite early market maturity

AI startups are achieving unicorn status—valuations of $1 billion or more—at an unprecedented rate. In 2024, 32 new AI unicorns were created, representing nearly half of all new unicorns globally. These startups are reaching this milestone with smaller teams and in less time compared to their non-AI counterparts. The median AI unicorn in 2024 had 203 employees and took just two years to achieve unicorn status, compared to 414 employees and nine years for non-AI unicorns.

However, many of these AI unicorns are still in the early stages of commercial maturity. According to CB Insights’ Commercial Maturity scores, over half of the AI unicorns born in 2024 are at the validating or deploying stages, whereas non-AI unicorns typically reach the scaling stage before achieving such valuations. This suggests that investor enthusiasm for AI is driving valuations based on potential rather than proven business models.

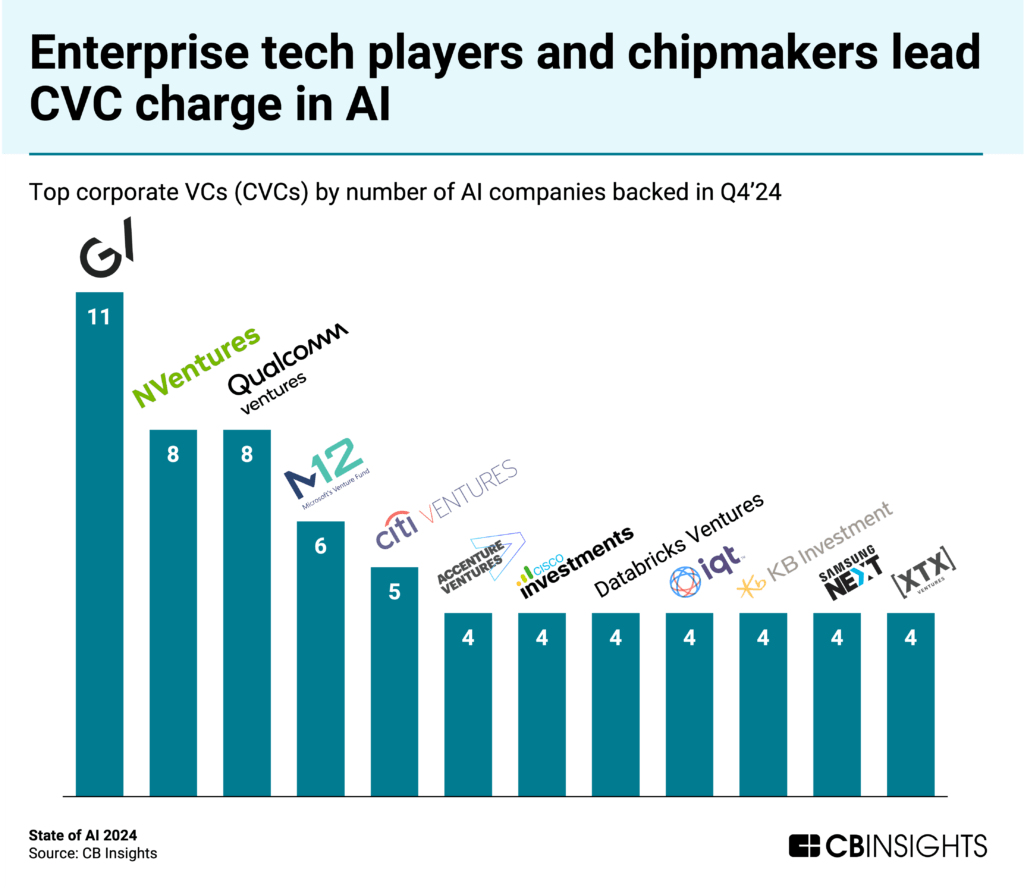

6. Tech leaders embed themselves deeper in the AI ecosystem

Major tech companies and chipmakers are playing an increasingly active role in the AI ecosystem through corporate venture capital (CVC) activities. In Q4 2024, Google (GV), Nvidia (NVentures), Qualcomm (Qualcomm Ventures), and Microsoft (M12) were among the most active investors in AI startups.

These investments reflect a strategic effort by established players to secure access to promising AI technologies while providing startups with essential technical infrastructure, such as cloud computing resources and advanced chips. This symbiotic relationship enables startups to accelerate their development while allowing tech giants to stay at the forefront of AI innovation.

Key takeaways:

- AI funding reached $100.4 billion in 2024, with mega-rounds making up 69% of the total.

- Industry-specific AI deals are declining, as investors focus on infrastructure and horizontal applications.

- Europe and Israel are becoming major AI startup regions, with high Mosaic scores and increasing early-stage investments.

- AI M&A activity remained strong, particularly in Europe and the US.

- AI unicorns are forming at record speed, with smaller teams and shorter timelines than non-AI startups.

- Major tech players, including Google, Nvidia, Qualcomm, and Microsoft, are embedding themselves deeper into the AI ecosystem.