business resources

Why the October 2025 Voluntary Disclosure Changes Open a New Window for Canadian Taxpayers

06 Mar 2026

In the heart of Canada's financial landscape, Toronto stands as a hub where entrepreneurs, professionals, and high-net-worth individuals navigate complex tax obligations amid one of North America's most dynamic economies. With Bay Street's towering institutions and the city's diverse business community spanning tech startups in the MaRS Discovery District to established firms in the Financial District, the pressure to stay compliant with the Canada Revenue Agency (CRA) has never been greater. Recent updates to the Voluntary Disclosure Program (VDP), effective October 1, 2025, mark a significant shift that could benefit many who have delayed correcting past errors or omissions in their tax filings.

The CRA processed around 21,000 VDP applications in recent years, uncovering billions in previously unreported income while providing relief from penalties and partial interest. These changes aim to encourage more voluntary compliance by broadening eligibility, simplifying processes, and offering clearer relief tiers. For Toronto residents and business owners facing mounting CRA stress from unfiled returns, undeclared foreign assets, or misreported income, this update creates a timely opportunity to address issues before enforcement actions intensify.

Understanding the Core Purpose of the Voluntary Disclosure Program

The VDP allows taxpayers and registrants to come forward voluntarily to correct errors, omissions, or non-compliance in their tax filings. In exchange, qualifying applicants typically receive relief from penalties, partial interest forgiveness, and protection from criminal prosecution for the disclosed matters. This program supports Canada's self-assessment tax system, where over 30 million individual and business returns are filed annually, by promoting honesty over forced compliance through audits.

Prior to the October 2025 revisions, the program featured a bifurcated structure with General and Limited streams, which often limited relief, especially for interest and in cases involving prompted disclosures. The CRA's data showed that many potential applicants hesitated due to strict eligibility rules, such as automatic disqualification after receiving certain CRA communications like demand letters. Nationally, non-compliance issues like unreported income or ineligible deductions led to over $5 billion in reassessments yearly, with Ontario accounting for a substantial share given Toronto's economic weight.

The new framework replaces those streams with a more flexible approach centered on whether a disclosure is unprompted or prompted. This change broadens access, particularly for those who received general outreach, educational letters, or initial compliance contacts but had not yet faced a formal audit or demand. In Toronto's competitive environment, where small business owners and self-employed professionals often juggle multiple income sources, this adjustment reduces barriers for proactive corrections.

Key Changes Effective October 1, 2025

Key Changes Effective October 1, 2025

The CRA introduced several enhancements to make the VDP more accessible and generous. Applications received on or after October 1, 2025, fall under the updated rules outlined in Information Circular IC00-1R7 and related GST/HST guidance.

One major shift involves eligibility for prompted applications. Previously, receiving a demand to file a letter or similar targeted communication often disqualified an applicant entirely. Now, even after such a letter, individuals may still qualify if they act promptly. This opens the door for many who are delayed due to fear of immediate disqualification.

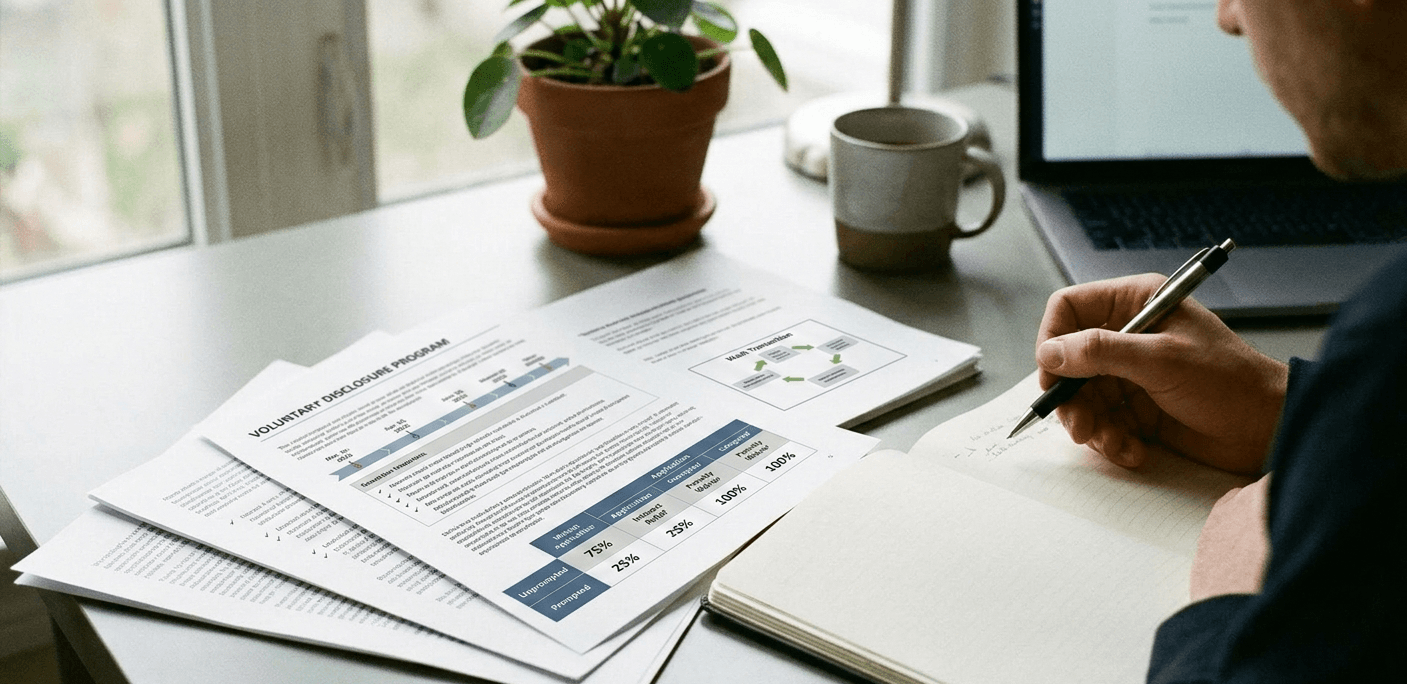

Relief tiers have also evolved. Unprompted applications, submitted without prior CRA contact on the specific issue, normally receive general relief: 75% forgiveness of applicable interest and 100% relief from penalties. Prompted applications, where the taxpayer received some form of CRA communication related to the matter, typically qualify for partial relief: 25% interest relief and up to 100% penalty waiver. Wash transactions, such as certain GST/HST adjustments, continue to attract full relief on both penalties and interest when eligible under existing policies.

The CRA simplified documentation requirements and application processes, including a revised Form RC199 expected to be more user-friendly. These updates address common pain points, as previous versions often required extensive back filings limited to three years in some cases. Now, the focus is on complete, accurate disclosures without arbitrary cutoffs for unintentional errors.

In Toronto, where high living costs and international ties are common, these changes resonate strongly. With average household incomes around $100,000 and significant foreign asset holdings among the city's immigrant population (over 50% of residents), many face complex reporting obligations. The VDP's enhanced accessibility helps mitigate risks from overlooked foreign income reporting under Form T1135 or GST/HST registration thresholds crossed by growing side businesses.

Why These Changes Matter for Those Who Have Delayed

If you've been putting off voluntary disclosure, the October 2025 updates change the calculus. The program is now less strict on eligibility, offers higher interest relief in many cases, and provides a clearer path forward even after initial CRA contact. This window encourages action before potential audits escalate, as the CRA continues to invest in data analytics and international information exchanges that uncover discrepancies more efficiently.

Statistics indicate the CRA's enforcement efforts recovered over $7 billion in additional revenue through compliance actions in recent fiscal years. Lifestyle audits and targeted reviews of high-risk areas like real estate transactions and digital income have increased, particularly in urban centers like Toronto. Delaying corrections can lead to compounding interest (currently around 9-10% annually on reassessed amounts) and penalties up to 50% for gross negligence.

For business owners in Toronto's vibrant sectors, from fintech in the King West area to creative industries in Liberty Village, undeclared income or improper deductions can arise from rapid growth. The VDP's updated relief tiers provide a buffer: general relief for early, unprompted fixes preserves cash flow, while partial relief still offers substantial protection for those prompted to act.

The changes also align with broader CRA goals of fostering compliance rather than punishment for honest mistakes. By expanding prompted eligibility, the agency acknowledges that many taxpayers need a nudge to correct issues without facing full consequences. This approach has already shown promise, with voluntary disclosures rising in periods of policy relaxation.

Practical Implications for Toronto Taxpayers and Businesses

Practical Implications for Toronto Taxpayers and Businesses

Toronto's economic diversity amplifies the relevance of these VDP updates. The city's small business sector, comprising over 100,000 enterprises, often deals with GST/HST complexities, especially in service-based or export-oriented fields. Missing registration thresholds or misclassifying expenses can lead to significant liabilities, but the new partial relief for prompted cases softens the blow for those who receive CRA educational materials or inquiries.

High-net-worth individuals in neighborhoods like Rosedale or Yorkville, with international investments or rental properties, benefit from clearer foreign reporting relief. The CRA's emphasis on complete disclosures, including amended returns for multiple years, helps resolve long-standing issues without arbitrary limits.

Self-employed professionals and gig economy participants, common in Toronto's creative and tech scenes, face unique challenges with irregular income and expense tracking. The VDP's interest relief (up to 75% for unprompted) can prevent erosion of savings from accumulated charges on back taxes.

Overall, these reforms signal a more balanced enforcement stance, encouraging corrections in a high-cost city where every dollar counts toward business sustainability or personal financial health.

Steps to Consider a Voluntary Disclosure

Assessing eligibility starts with gathering records: past returns, bank statements, foreign asset details, and any CRA correspondence. Completeness is crucial, as incomplete applications risk rejection.

Determining if your situation qualifies as unprompted or prompted guides expectations for relief. General outreach letters typically do not disqualify, preserving general relief potential.

Preparing the application involves detailing the non-compliance, calculating adjustments, and providing supporting documents. The simplified process aims to reduce administrative burden.

Timing matters. With the changes now in effect, acting sooner maximizes benefits before any further CRA contacts narrow options.

In Toronto, local resources like business networks and professional associations offer guidance, but personalized review ensures accuracy given provincial tax layers.

Real-World Context and Broader Trends

Across Canada, the VDP has facilitated corrections for billions in income, with Ontario leading due to population and economic activity. The 2025 updates build on this by addressing feedback about rigidity, aiming to increase participation rates.

For many, the fear of penalties and interest has deterred action. Now, with higher relief thresholds and expanded prompted eligibility, the program aligns better with real-life scenarios where taxpayers discover errors post-CRA contact.

This evolution supports long-term compliance in an era of enhanced data sharing and analytics. Toronto's global connections make timely corrections especially valuable for avoiding cross-border complications.

Navigating Forward with Confidence

Navigating Forward with Confidence

The October 2025 changes represent a meaningful opportunity for those with unresolved tax matters. By broadening access and enhancing relief, the CRA encourages proactive steps that benefit both taxpayers and the system.

In a city like Toronto, where economic opportunities abound alongside compliance complexities, staying informed and addressing issues promptly safeguards financial futures.

Consulting a Professional tax consultant can provide clarity on applying these updates to individual circumstances, ensuring disclosures meet requirements for maximum relief.

Frequently Asked Questions

What qualifies as an unprompted versus prompted VDP application under the new rules?

An unprompted application occurs without prior CRA communication on the specific issue, qualifying for 75% interest relief and 100% penalty relief. A prompted application follows some CRA contact, like an educational letter or demand, but still offers up to 100% penalty relief and 25% interest relief.

How much interest and penalty relief can I expect from a qualifying VDP disclosure?

General relief for unprompted cases provides 75% interest forgiveness and full penalty waiver. Partial relief for prompted cases grants 25% interest relief and up to 100% penalty relief. Wash transactions may receive full relief on both.

Does receiving a CRA demand letter still disqualify me from the VDP?

No, under the October 2025 changes, you may still qualify even after a demand letter, provided you submit promptly. This expands eligibility compared to previous rules.

What should I do if I suspect errors in past tax filings?

Gather relevant documents, assess the scope of non-compliance, and consider submitting a VDP application soon to benefit from the updated relief tiers. Professional review helps ensure completeness and eligibility.