citiesabc, first_page

The Process and Infrastructure to Tokenise Real Estate and Multi-Assets on a Trading and Investing Platform (Part 1)

25 Jun 2026

Tokenisation is the future of real estate that is redefining ownership, investment, and urban finance. It is the biggest transformation of property ownership since land registries. How does tokenisation democratise property ownership?

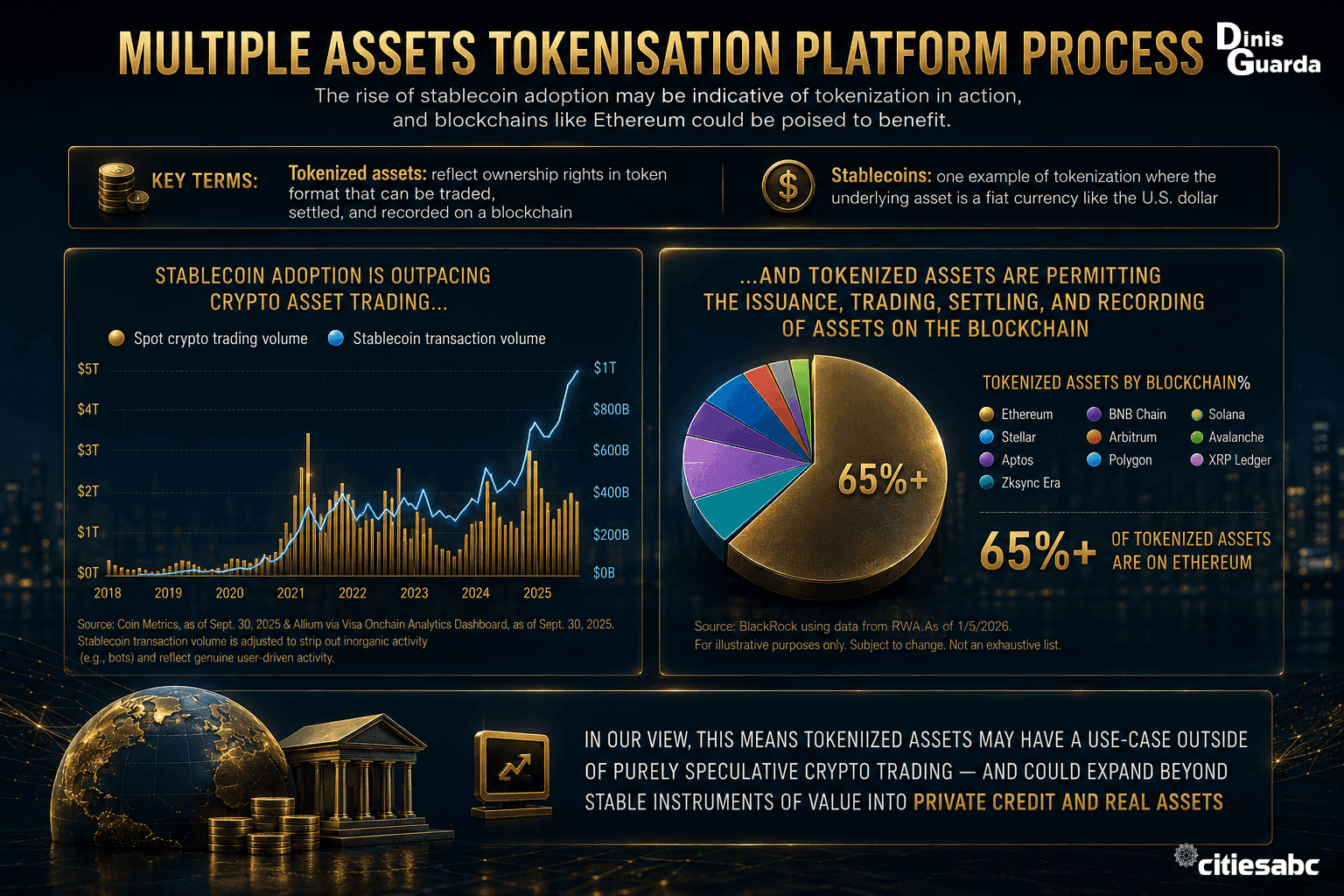

Tokenisation is the path global organisations are taking for the next stage of digital transformation of the global economy and its assets. The market is growing at an incredible pace, and 2026 has been the year of maturity, as Stablecoins have become mainstream, and global financial players and governments are taking this seriously.

For cities and urban economies, this matters more than most people realise. The global financial architecture is undergoing a foundational rewrite as tokenisation transitions from an experimental phase into a standard operational framework. Driven by clear regulatory parameters, an influx of institutional-grade structures, and the ubiquity of stablecoins acting as the default liquidity layer, tokenisation is driving a historic shift in how global assets, including the real estate that defines our cities, are issued, cleared, and managed.

The 2026 Tokenisation Landscape: Market Snapshot

The Real-World Asset (RWA) tokenisation market has moved aggressively past early proof-of-concept constraints to become a multi-billion dollar ecosystem.

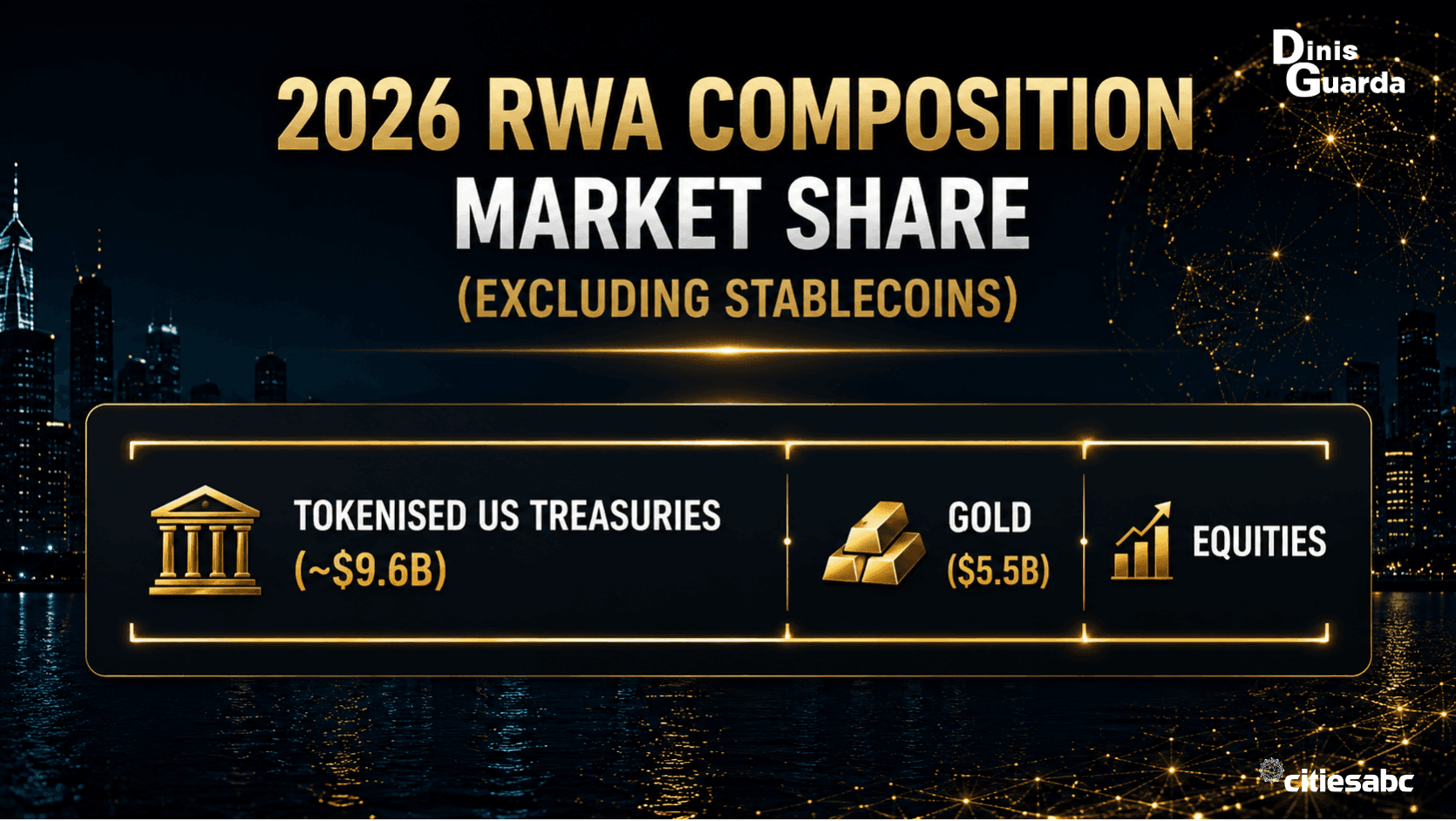

- Total RWA Market Valuation: The non-stablecoin tokenised RWA sector has expanded rapidly, reaching an active valuation exceeding $25 billion and is on track to reach $2 trillion by 2030.

- The Yield Engine (U.S. Treasuries): High interest rates have made tokenised sovereign debt the fastest-growing sector. Tokenised U.S. Treasuries represent the single largest category, sitting at ~$9.6 billion.

- Commodities & Precious Metals: Tokenised commodities reached $5.55 billion, with institutional-grade gold tokens (like XAUT and PAXG) capturing 70% of that volume.

- Tokenised Equities: Public equity wrapped in digital security layers grew into a $960 million market sector, doubling from mid-2025 levels.

Stablecoins as Institutional Settlement Rails

Stablecoins have evolved from simple speculative crypto on-ramps into systemic infrastructure for global commerce. Total circulating stablecoin supply has crossed $320 billion (led by Tether at $185.5B and Circle at $78.6B).

This is infrastructure cities should be watching closely, because it underpins how urban capital will move in the next decade.

- Unprecedented Volume: In Q1 alone, stablecoin transfer volume reached a record $4.5 trillion. This rapid scaling is prompting legacy financial processors to view the sector as an immediate operational challenge for traditional credit card and clearinghouse architectures.

- Geographic Centres: The real velocity of money resides in the Asia-Pacific region. Nearly two-thirds of global stablecoin transaction volume originates from hubs such as Singapore, Hong Kong, and Japan — three cities that are also among the most aggressive in piloting tokenised public infrastructure.

- B2B Payment Rails: According to corporate payment processors like Stripe and BVNK, cross-border freelancers and digital businesses receive roughly 35% of their income directly in stablecoins, bypassing slow, multi-day legacy bank wires.

Major Industry Players

The ecosystem is split between traditional banking monoliths implementing decentralised ledgers and native fintech infrastructures providing the core programmatic tooling:

- The Asset Aggregators (Ondo Finance & BlackRock): Ondo dominates the tokenised equity sector with a 60% market share. Concurrently, BlackRock's BUIDL fund remains the largest institutional product on-chain, commanding over $1.7 billion in assets.

- The Transfer Powerhouses (Securitise & Tokeny): These firms act as the regulated tech layers. They oversee digital compliance workflows, verify investor allowlist data, and coordinate multi-chain issuances.

- The Clearinghouses (DTCC & Canton Network): Traditional finance's back-end giants are deploying unified interoperability layers to sync private banking mainframes with public chains seamlessly.

Global Government Adoption & Case Studies

This is the part I find most important for our cities and governance audience. Governments have stopped viewing tokenisation as a regulatory challenge and have instead embraced it to upgrade public sovereign debt architectures and increasingly, urban infrastructure finance.

Case Study 1: Hong Kong's Project Ensemble

The Hong Kong Monetary Authority (HKMA) transitioned its financial sandbox, Project Ensemble, into full live deployment. Commercial banks natively utilise tokenised interbank deposits to clear tokenised money market fund transactions in real time. Simultaneously, the Hong Kong government institutionalised its framework to regularise the formal issuance of tokenised green government bonds directly on-chain, a model other dense, capital-intensive cities will likely study closely.

Case Study 2: The Anglo-French Wholesale Digital Euro Initiatives

The Banque de France and the UK authorities accelerated financial tokenisation by aligning with the European Savings and Investments Union (SIU) framework. This collaborative agenda supports the deployment of a central bank digital interbank money system (wholesale CBDC), allowing European tier-1 banks to execute high-value cross-border settlements with absolute finality using tokenised euros.

Case Study 3: The United States Legislative Foundation

Following the passage of structural digital asset legislation by Congress, the regulatory landscape has cleared the path for U.S. financial institutions. The Federal Reserve and commercial banks are actively managing the intersection in which tokenised money market funds serve as eligible collateral or reserve backing for regulated stablecoins.

How do we tokenise real estate and real-world physical assets?

This is the question I get asked most by city planners, developers, and investors alike. The best process for tokenising real estate infrastructure on a platform follows a strict 5-step blueprint that prioritises legal structure, infrastructure configuration, and capital operations. Because tokenised real estate is classified as a regulated security, the technical deployment (the smart contract) is built after the legal wrapper is locked down.

➔ 1. Legal Structuring and asset preparation

➔ 2. Tech & Standard Setup

➔ 3. Onboarding & Compliance

➔ 4. Token Minting

➔ 5. Post-Launch & Secondary Liquidity

Set up the foundation for Tokenisation

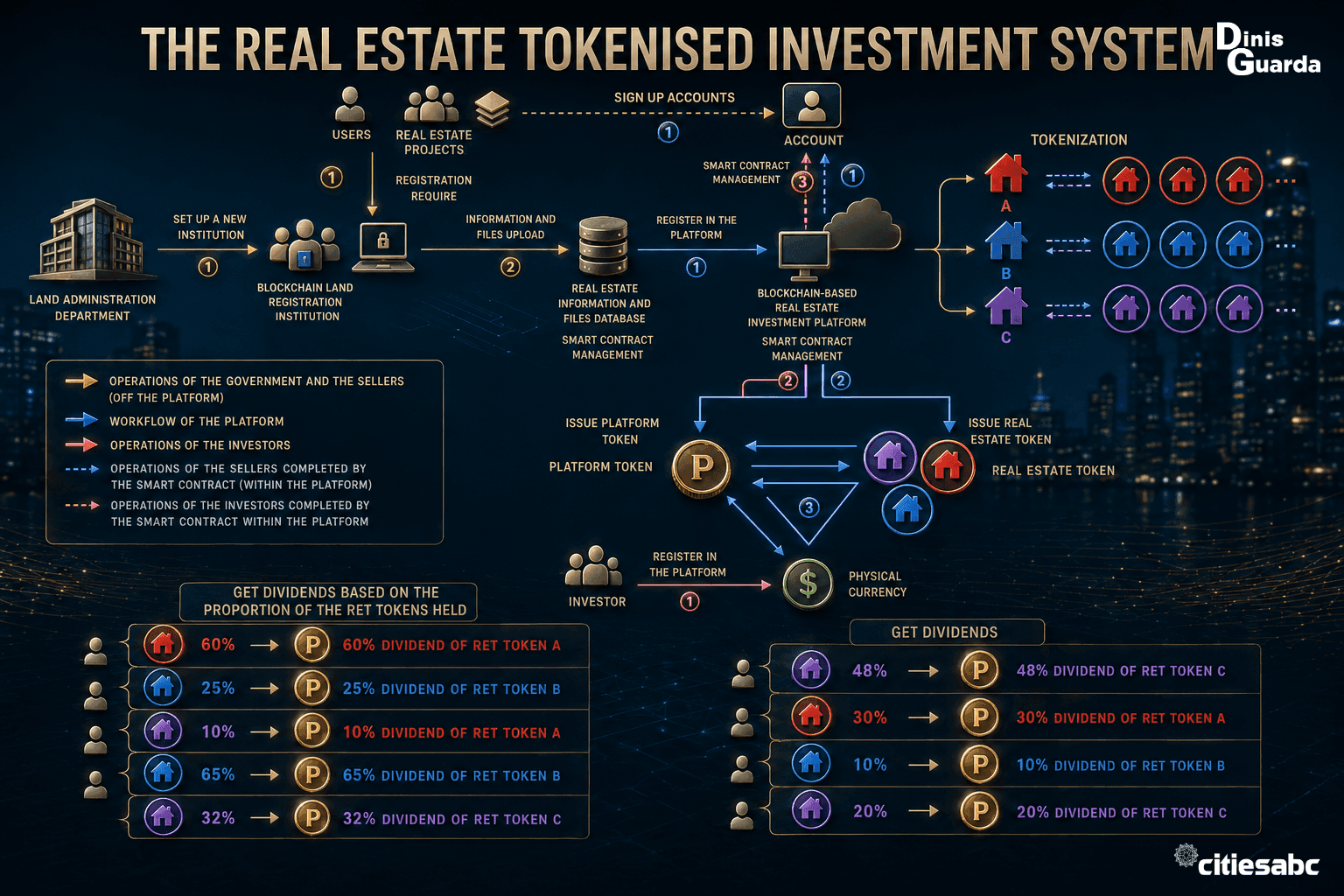

1. Legal Structuring & Asset Valuation

- Establish a Special Purpose Vehicle (SPV): Real estate tokens rarely represent the physical land directly. Instead, you create a dedicated legal entity (such as an LLC or SPV) that owns the property, and the tokens represent equity or debt interests in that entity.

- Perform a Comprehensive Valuation: Secure a formal appraisal to determine the Net Asset Value (NAV). This value establishes the exact initial price per token relative to the fractionalised pool.

- Map Jurisdictional Compliance: Determine the legal framework based on the asset's location and the investors' residence. This includes frameworks such as Reg D or Reg S in the US, MiFID II/AIFMD in Europe, and local regulations as outlined in the Zoniqx Architecture Guide.

2. Technology Selection & Token Standards

- Choose a Tokenisation Platform Tier: Decide whether to build a custom dApp using an internal development team, utilise a Software-as-a-Service (SaaS) tool, or deploy a pre-configured white-label portal such as the Tokeniser Estate Framework.

- Select a Permissioned Token Standard: Avoid standard public tokens (like ERC-20) which cannot enforce trading restrictions. Use security token standards like ERC-3643 (T-REX) for single-asset SPVs with on-chain identity checks, or ERC-1400 for complex multi-tranche structures, as outlined in the Tokeniser Estate Infrastructure Analysis.

- Pick the Blockchain Protocol: Select a blockchain network that matches your target ticket size and investor profile. Avalanche, Ethereum and Layer-2 scaling solutions are common, while institutional platforms often prefer dedicated asset-specific chains such as the Polymesh Network.

3. Compliance Framework & Investor Onboarding

- Integrate Identity Registries: Connect decentralised identities (such as ONCHAINID) directly to smart contracts. This ensures that the token automatically rejects any transfer request to an unverified wallet.

- Automate KYC/AML Workflows: Build an investor dashboard that handles automated identity verification, anti-money-laundering checks, and accredited-investor validation before users can link their wallets.

4. Smart Contract Deployment & Token Minting

- Program Operational Rules: Code the smart contracts to govern dividend distribution schedules, shareholder voting rights, and transfer lock-ups into the blockchain ledger.

- Integrate Off-Chain Real-World Assets Data: Use decentralised oracle frameworks like Chainlink Proof of Reserve to bridge off-chain bank accounts or property values to the on-chain tokens, preventing the minting of unbacked shares.

- Execute the Initial Token Offering (ITO): Launch the primary investor portal to distribute fractional property tokens to successfully allowed participants.

Post-Launch Management & Liquidity

- Synchronise Capital Tables: Connect your on-chain token transactions to an off-chain registry via Token Asset Lifecycle Management (TALM) software to keep legal records accurate.

- Automate Fiat and Tokens Cash Flows: Map out rent or dividend payments. Rental income arrives in fiat into a traditional bank account, requiring the platform to execute automated payouts via on-chain stablecoins or direct wire transfers.

- Enable Regulated Secondary Markets: Provide secondary liquidity options by integrating your platform with Alternative Trading Systems (ATS) or Multilateral Trading Facilities (MTFs), allowing investors to exit positions legally.

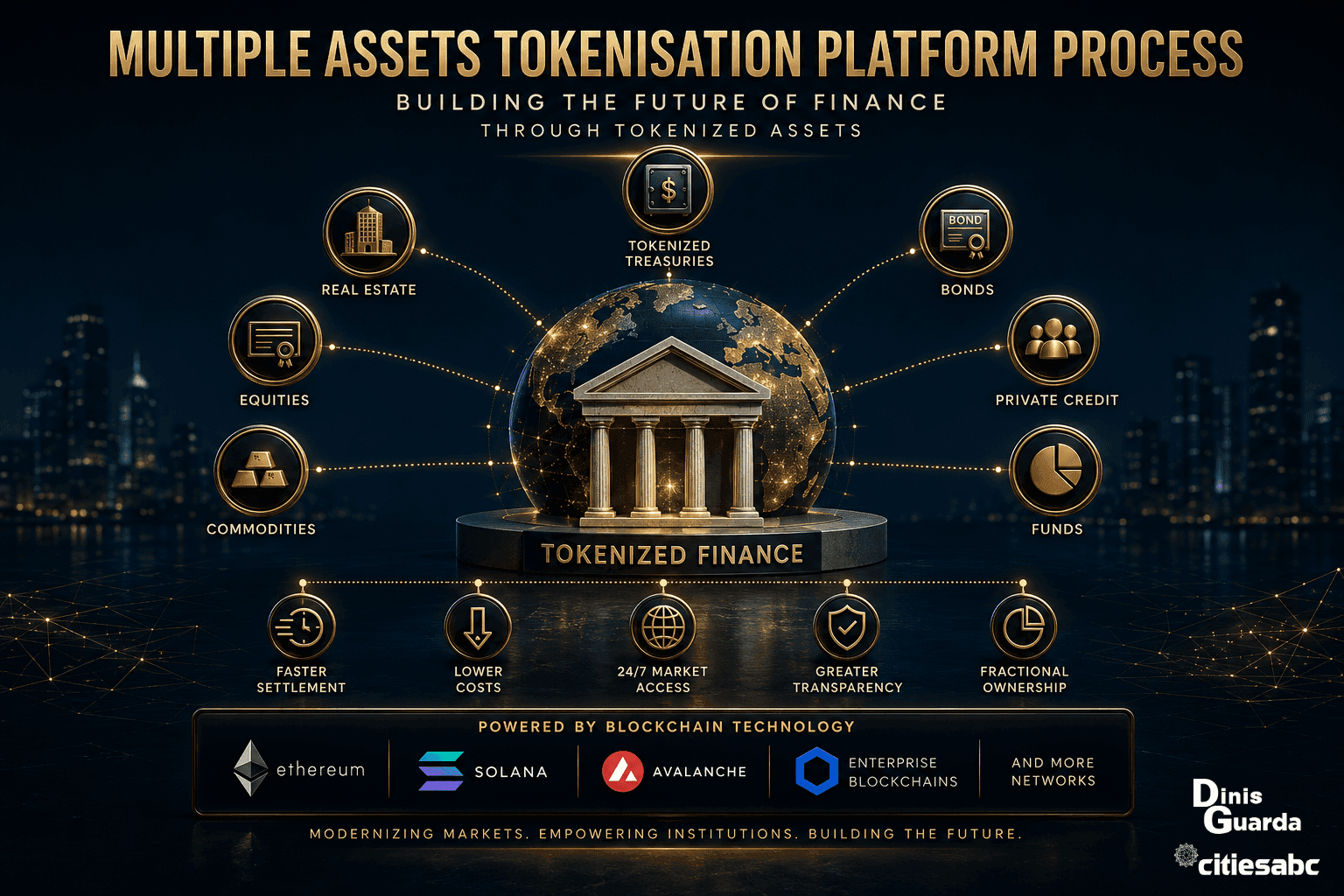

Multi-asset tokenisation

Single-Asset vs Multi-Asset Tokenisation Core Differences

The primary difference lies in the underlying composition, complexity, and legal risk distribution of the digital security.

Feature | Single-Asset Tokenisation (e.g., Real Estate) | Multi-Asset Tokenisation (e.g., Diversified Fund) |

| Asset Composition | One distinct, isolated asset (e.g., a specific commercial building). | A basket of diverse asset classes (e.g., real estate + private credit + bonds). |

| Risk Profile | High concentration risk; returns depend entirely on that single entity. | Diversified risk; another offsets underperformance in one sector. |

| Valuation (NAV) | Appraisals are episodic (quarterly/annually), causing stagnant pricing. | Dynamic and real-time; feeds synthesise public prices and private asset values. |

| Legal Framework | Single Special Purpose Vehicle (SPV) holding a property title. | Complex Umbrella Fund, Mutual Fund, or multi-tiered LP/GP matrix. |

| Rebalancing | Static; tokens represent a permanent fixed slice of the property. | Active or Algorithmic; smart contracts trigger asset swaps within the basket. |

Step-by-Step Architecture of Multi-Asset Tokenisation

Tokenising a diverse basket of assets requires bridging disparate liquidity timelines, legal jurisdictions, and oracle data streams into a unified on-chain ledger.

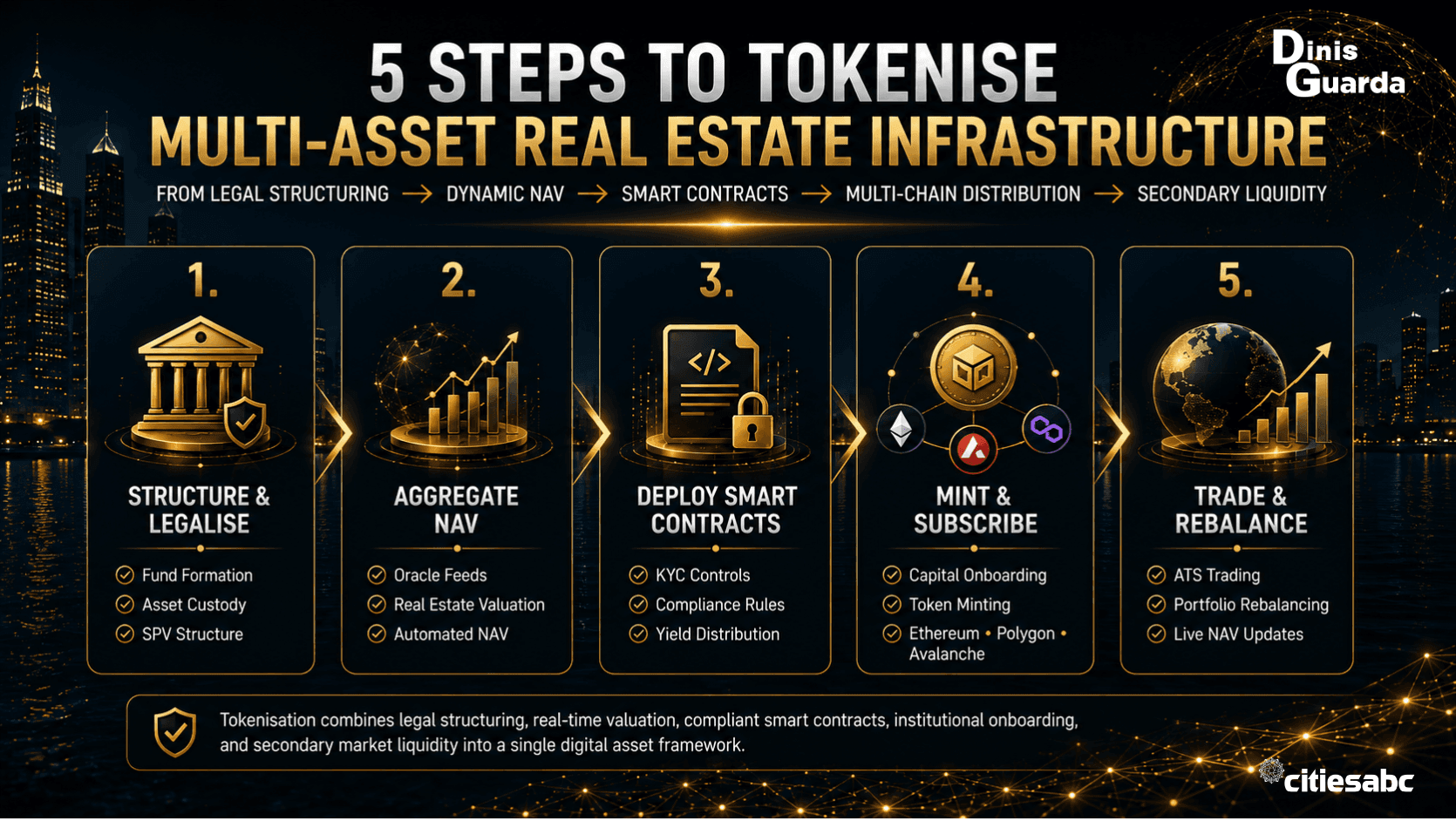

Step 1: Structural Setup & Fund Legalisation

Instead of using a property-specific LLC, issuers set up an Umbrella Fund, Mutual Fund, or Variable Capital Company (VCC). This entity holds the custodial accounts for liquid securities, as well as specialised SPVs for private, illiquid holdings such as physical real estate or infrastructure contracts.

Step 2: Dynamic NAV (Net Asset Value) Aggregation

Because the basket contains both highly liquid assets (e.g., US Treasuries) and slow-moving physical real estate, the platform establishes decentralised data connections. Platforms plug in oracles like Chainlink to pull real-time feeds from traditional markets, alongside scheduled appraised values for physical structures, and consolidate them into an aggregated, automated NAV calculation.

Step 3: Security Token Smart Contract Logic

Developers deploy multi-compliant smart contracts (such as ERC-3643 or custom security token standards). Unlike simple tokens, multi-asset contracts include embedded functions to dictate:

- Regulatory Permissions: Enforcing automated restrictions so that only whitelisted, KYC-vetted addresses can execute trades.

- Yield Distribution Waterfall: Automatically dispersing diverse inflows, such as bond interest, stock dividends, and real estate rental revenue, to token holders proportionally.

Step 4: Multi-Chain Minting & Subscription

Vetted institutional capital arrives via fiat wire or stablecoins. The minting platform interacts with the blockchain to issue fractional shares of the fund. To capture maximum capital pools, tokens are often distributed across multiple networks natively (e.g., utilising Avalanche subnets, Ethereum, and Polygon) via specialised bridging architectures.

Step 5: Secondary Market Trading & Rebalancing

The basket is traded continuously on regulated alternative trading systems (ATS). If the asset manager decides to rebalance the portfolio (e.g., selling bonds to buy more real estate), the internal corporate action takes place behind the scenes. The on-chain token contract remains identical; only its underlying metadata and oracle-driven NAV change.

Major Industry Players in Multi-Asset Tokenisation

The institutional ecosystem is dominated by heavily regulated issuance platforms, decentralised capital networks, and clearinghouse infrastructures:

- Securitise: The dominant transfer agent and issuance platform for tokenised institutional funds. They facilitate compliance, cap table management, and minting for high-profile, multi-asset corporate funds.

- Tokeny: A major institutional software infrastructure provider utilising the ERC-3643 standard to execute multi-chain, on-chain compliance management for real-world asset portfolios.

- Centrifuge: A specialised protocol that pools diverse real-world credit, structured finance, and yield-bearing assets into transparent on-chain investment pools.

- Ondo Finance: An investment platform targeting structured multi-asset tokenisation by packaging cash equivalents, high-yield corporate bonds, and equities into institutional-grade digital wrappers.

- tZERO: A premier secondary market marketplace and technology provider that hosts multi-asset institutional trading infrastructure with full SEC compliance.

- DTCC (Depository Trust & Clearing Corporation): The traditional financial system's clearing powerhouse, actively deploying foundational multi-asset infrastructure to smoothly move tokenised assets between legacy bank ledgers and public blockchains.

Sources:

- Zoniqx — Real Estate Tokenisation Architecture & Compliance Guides

https://www.zoniqx.com/resources/how-to-tokenize-real-estate-in-2025-a-step-by-step-guide - Zoniqx — Tokenisation and Compliance: Multi-Jurisdictional Best Practices (ERC-3643/ERC-7518 standards)

https://www.zoniqx.com/resources/tokenization-and-compliance-multi-jurisdictional-best-practices - Hong Kong Monetary Authority — EnsembleTX / Project Ensemble Launch (Pilot Phase)

https://www.hkma.gov.hk/eng/news-and-media/press-releases/2025/11/20251113-3/ - Hong Kong Monetary Authority — HKSAR Government's Third Digital Green Bonds Offering

https://www.hkma.gov.hk/eng/news-and-media/press-releases/2025/11/20251111-6/ - Banque de France — Rethinking Central Bank Money in the Digital Age (Pontes/Appia, wholesale CBDC, SIU)

https://www.banque-france.fr/en/governors-interventions/rethinking-central-bank-money-digital-age - Global Government Finance — UK and French Authorities Step Up Financial Markets Tokenisation Efforts

https://www.globalgovernmentfinance.com/uk-france-financial-tokenisation-step-up-efforts/ - DTCC — DTCC and Digital Asset Partner to Tokenize DTC-Custodied U.S. Treasury Securities on the Canton Network

https://www.dtcc.com/news/2025/december/17/dtcc-and-digital-asset-partner-to-tokenize-dtc-custodied-us-treasury-securities