India Data Center Market: Comprehensive Analysis and Investment Outlook (Part 2)

04 Feb 2026

Capital Influx: USD 20 Billion+ Investment Pipeline

Between 2020 and 2025, more than USD 14 billion has been invested in India's data center sector, while announced pipeline commitments exceed USD 20 billion. This substantial capital influx could increase India's current data center capacity by 35 to 40 percent, positioning the country as a potential regional hub for AI infrastructure.

The investment landscape is characterised by three distinct patterns. Global hyperscalers, led by AWS, Microsoft Azure, and Google Cloud, are committing over USD 15 billion collectively, driven by cloud adoption and AI workload demands. Indian conglomerates, particularly Reliance Industries and Adani Group, are deploying integrated models that combine data centers with power generation and real estate development. Specialized colocation operators are strategically targeting Tier-2 cities, capitalizing on lower costs and favorable state incentives.

Infrastructure asset status has been a critical enabler, facilitating access to longer-term financing, reducing capital costs, and accelerating regulatory approvals. This classification positions data centers alongside roads, ports, and power plants in India's infrastructure hierarchy.

Major Investment Commitments (2024-2026)

Hyperscale and Conglomerate Investments:

- Reliance Industries: ~USD 30 billion for a ~3 GW AI and data center campus in Jamnagar, Gujarat—the largest single data center commitment in India

- Adani Group: ~USD 10 billion for multi-city expansion across Mumbai, Chennai, and Hyderabad, leveraging integrated power and infrastructure capabilities

- AdaniConneX (Adani-Google JV): Up to USD 15 billion ecosystem investment for vertically integrated data centers, renewable energy, and connectivity

- AWS, Microsoft Azure, Google Cloud: Combined USD 15+ billion for hyperscale capacity across Mumbai, Chennai, and Hyderabad

Colocation and Specialist Operators:

- STT GDC India: ~USD 3.2 billion for colocation footprint expansion

- CtrlS Datacenters: ~USD 2 billion for multi-campus expansion with strong enterprise and government focus

- NTT Global Data Centers: ~USD 1.5 billion to double India capacity

- Yotta Infrastructure: ~USD 1-1.2 billion for hyperscale campuses in Navi Mumbai

- RackBank: USD 360 million for 80 MW AI-focused facility in Raipur, Chhattisgarh—representing the first hyperscale-grade data center in central India

Investment Drivers and Market Dynamics

The capital influx is underpinned by several structural factors. First, data localization mandates under the Digital Personal Data Protection Act (DPDPA) have created non-discretionary demand, particularly from the banking, financial services, and insurance (BFSI) sector. Second, India's cost competitiveness, with development costs around USD 7 per watt and electricity tariffs approximately 20% lower than the United States, enhances investment returns.

Third, the AI revolution is driving a shift from traditional colocation to compute-intensive infrastructure. Rack densities are increasing from 5-10 kW to 50-120 kW for AI workloads, requiring complete redesign of power and cooling systems. This creates opportunities for greenfield investments while posing obsolescence risks for legacy facilities.

Fourth, geographic diversification is gaining momentum. While Mumbai and Chennai remain primary hubs due to subsea cable connectivity, Tier-2 cities offer lower land costs, faster approvals, and growing state-level incentives. This is evidenced by RackBank's Raipur facility and expanding pipelines in Noida, Greater Noida, and Gujarat.

Infrastructure Constraints: The Real Growth Limiter

Multiple research studies consistently indicate that India's data center growth is constrained primarily by infrastructure readiness rather than demand or capital availability. The sector faces a complex matrix of challenges across power, water, land, policy, and human capital dimensions.

Power: The Primary Bottleneck

Although data centers currently consume less than 0.5% of India's total electricity, this share is projected to reach approximately 2% by 2026 and 8% by 2030. The challenge is not absolute capacity but rather grid reliability, regional variability, and the availability of renewable energy at scale.

Mission-critical digital infrastructure requires reliability standards exceeding 99.999% uptime—a benchmark not consistently met by many regional grids. Consequently, operators maintain redundant backup systems, traditionally diesel-based, which introduce both economic and environmental challenges. Grid connection timelines in Tier-1 metros can extend 18-24 months, creating significant execution risk.

Development costs of INR 60-70 crore (USD 7-8 million) per megawatt include substantial power infrastructure investments. Inter-state electricity tariff variations and differential access to renewable energy significantly influence site selection decisions, creating a complex regulatory landscape for operators.

Critical Power Metrics:

- Current consumption: <0.5% of national electricity generation

- Projected 2026 share: ~2% of national demand

- Projected 2030 share: ~8% of national demand (~17 GW IT capacity)

- Grid reliability requirement: ≥99.999% uptime

- Regional reliability: Uneven across states; metro and coastal hubs advantaged

Water: The Emerging Constraint

Water consumption is increasingly recognized as a constraint equal to power, especially in dense urban markets. Evaporative cooling systems may require up to 25 million liters of water per megawatt annually, raising sustainability concerns in water-scarce cities like Chennai and Mumbai.

Water Usage Effectiveness (WUE) has emerged as a critical benchmark, with the Indian Green Building Council (IGBC) setting targets below 2.2 liters per kWh. Mandatory water impact assessments are now required in major metros, and leading operators are implementing closed-loop cooling, rainwater harvesting, and treated sewage water (TSW) systems.

CtrlS Datacenters, for example, has recycled approximately 10 million liters of water, demonstrating the transition from linear to circular water management. Facilities with low WUE and recycling capacity show higher long-term operational resilience, particularly in climate-variable regions.

Water Management Imperatives:

- Typical consumption: Up to 25 million liters per MW annually

- WUE target: <2.2 liters per kWh (IGBC standard)

- Regulatory trend: Mandatory water impact assessments in Chennai, Mumbai

- Leading practices: Rainwater harvesting, TSW, closed-loop cooling

- Strategic implication: Water efficiency becoming resilience metric

Land and Geographic Concentration

Land scarcity and high costs in Tier-1 metros (Mumbai, Chennai, Hyderabad, Bengaluru) are driving geographic redistribution. Urban land prices, combined with zoning and permitting complexity, create cost inflation and execution delays. This is prompting operators to develop data center parks, industrial corridor campuses, and satellite facilities outside core metros.

Tier-2 cities offer structural advantages: lower land costs, faster approvals, proximity to regional demand, and growing fiber connectivity. However, power redundancy, network depth, and water recycling infrastructure are still evolving, creating a trade-off between cost efficiency and infrastructure maturity.

AI-Ready Infrastructure Gap

India generates approximately 20% of global data but hosts only 3% of global data center capacity. More critically, the country has limited GPU-dense facilities capable of supporting high-performance AI training and inference workloads.

This infrastructure gap creates risk of AI workload migration offshore and slower domestic AI ecosystem development. Government initiatives like the IndiaAI Mission (₹10,371 crore allocation for 10,000 GPUs) aim to address this through public compute infrastructure, but execution depends on parallel development of supporting data center capacity.

Incentives for AI-optimized data centers, GPU clusters, and high-density campus zoning are emerging as policy priorities in states like Andhra Pradesh, Telangana, and Uttar Pradesh.

Capital Intensity and Financing

High upfront investment requirements (INR 60-70 crore per MW) create entry barriers and increase reliance on foreign capital. Infrastructure status classification has improved access to long-tenor debt and enabled Real Estate Investment Trusts (REITs), but project financing remains complex.

Public-private partnership models are gaining traction, particularly for AI infrastructure and Tier-2 city development. However, capital intensity combined with 24-30 month development timelines creates significant execution and market risk.

Policy Fragmentation

India's federal structure creates variability in state-level incentives, power tariffs, water access policies, and approval processes. While competitive federalism can accelerate investment in progressive states, it also generates regulatory uncertainty and uneven capacity distribution.

The absence of a harmonized national data center and AI infrastructure policy creates complexity for operators planning multi-state deployments. States like Maharashtra, Telangana, Andhra Pradesh, and Gujarat have established dedicated data center policies, while others remain in early stages.

Talent Scarcity

Despite a large engineering workforce, India faces deficits in specialized expertise for electrical systems, cooling infrastructure, cyber-physical security, and facility operations. Training capacity is increasing through partnerships between operators and technical institutions, but demand for specialized skills continues to exceed supply.

This talent gap is particularly acute for AI-ready infrastructure requiring expertise in high-density rack design, liquid cooling systems, and GPU cluster management.

Infrastructure Constraints: Strategic Summary

| Constraint | Impact | Mitigation Strategy |

|---|---|---|

| Power availability & grid capacity | Delayed commissioning, higher costs, AI deployment constraints | Dedicated power corridors, renewable procurement, captive generation |

| Water scarcity & cooling | Approval delays, sustainability risk, community resistance | Liquid cooling, recycled water, water-positive design |

| Sustainability vs. scale trade-off | ESG exposure, regulatory scrutiny, investor pressure | Renewable PPAs, PUE/WUE benchmarks, ESG financing |

| AI-ready infrastructure gap | Offshore workload migration, slower AI ecosystem | GPU cluster incentives, high-density zoning |

| Capital intensity | Slower scaling, entry barriers, foreign capital reliance | Infrastructure status, REITs, PPP models |

| Land scarcity in metros | Cost inflation, delays, concentration risk | Data center parks, Tier-2 expansion |

| Policy fragmentation | Regulatory uncertainty, uneven capacity | National policy harmonization |

| Talent shortage | Execution constraints, operational risk | Industry-academia partnerships, training programs |

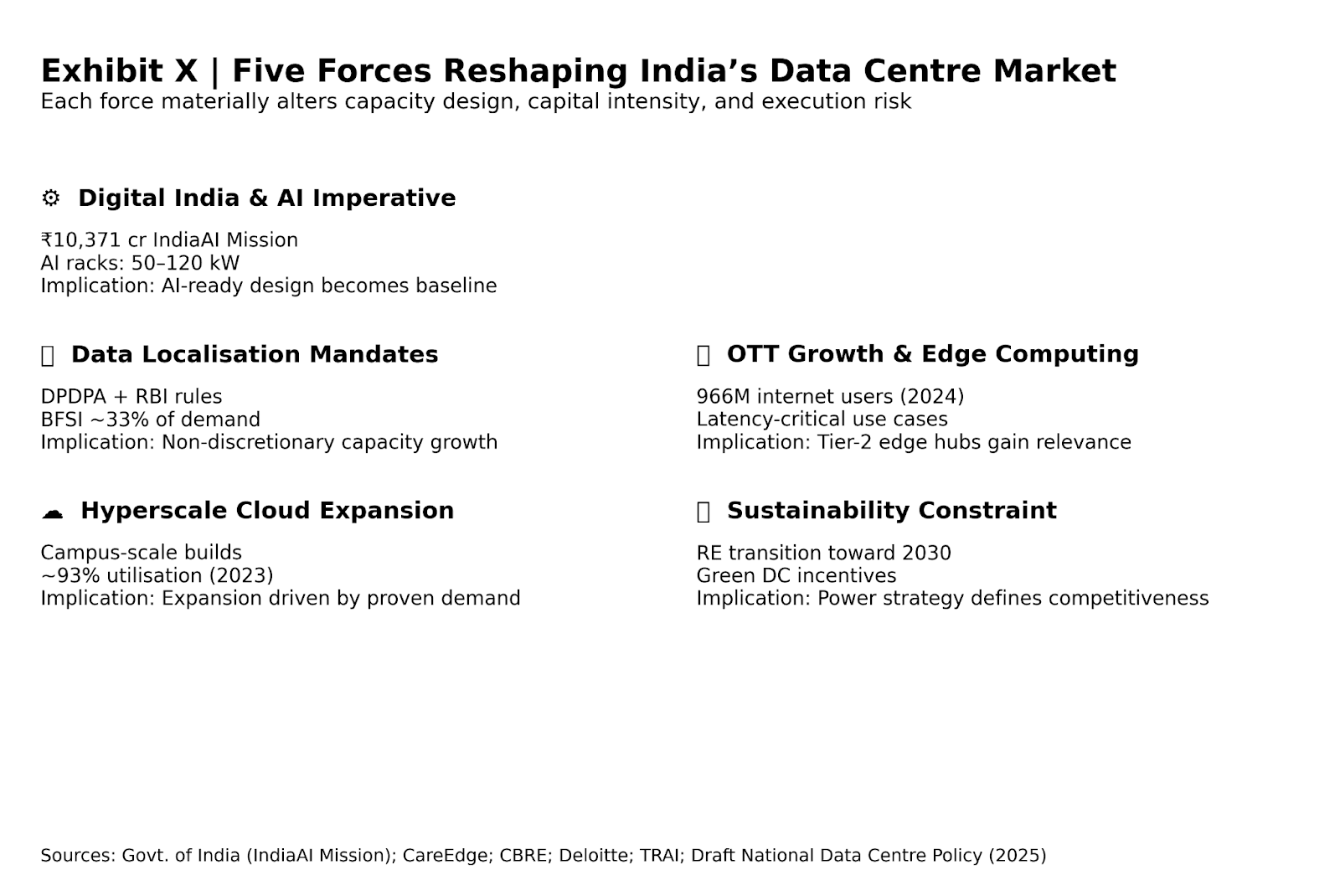

Five Forces Reshaping the Market

1. Digital India & the AI Imperative

The Indian government's IndiaAI Mission, with an allocation of ₹10,371 crore (approximately USD 1.25 billion) for acquiring 10,000 GPUs, signals computing infrastructure's elevation to essential national infrastructure status. This represents a fundamental shift from connectivity-focused digital policy to compute-centric strategy.

AI workloads are transforming data center economics. Rack densities are increasing from 5-10 kW (traditional enterprise) to 50-120 kW per rack for AI training and inference. Industry consensus suggests AI-related workloads could comprise approximately 50% of total data center capacity within the next decade.

This shift necessitates complete facility redesign—power distribution, cooling architecture, and floor loading must be reconceived. Assets not configured for AI workloads face significant obsolescence risk, creating a structural advantage for greenfield developments over brownfield retrofits.

The government's public AI infrastructure initiative creates anchor demand for AI-optimized facilities, reducing risk for early-stage infrastructure investment and potentially stimulating private-sector co-investment in additional capacity.

2. Data Localisation as Non-Discretionary Demand

India's data localization framework, anchored by the Digital Personal Data Protection Act (DPDPA) and sector-specific Reserve Bank of India mandates, has transformed regulatory compliance into a structural demand driver.

The BFSI sector alone accounts for approximately 33% of data center end-user demand. Healthcare, government, and telecommunications sectors face similar domestic storage and processing requirements. Foreign cloud providers that previously served Indian demand from offshore locations must now procure or develop domestic capacity.

This creates sustained, policy-driven demand that is less sensitive to economic cycles than traditional enterprise IT spending. Data sovereignty requirements establish a demand floor that underpins long-term investment confidence.

Compliance complexity is increasing. Organizations must navigate not only national frameworks but also sector-specific regulations and emerging state-level data governance policies. This favors operators with regulatory expertise and multi-jurisdiction capabilities.

3. Hyperscale Cloud Platform Expansion

Hyperscale cloud providers are shifting from incremental capacity additions to campus-scale, platform-level deployments. This reflects growing confidence in India's market fundamentals and infrastructure maturity.

Mumbai and Chennai function as international data gateways, supported by 17 subsea cables and 14 landing stations. This coastal connectivity infrastructure enables high-capacity, low-latency global connectivity, critical for hyperscale operations serving both domestic and international clients.

Market utilization metrics support continued expansion. Capacity utilization increased from approximately 82% in 2019 to 93% in 2023, indicating tight supply-demand balance. Operator revenues grew at a compound annual growth rate of 25% from FY2017 to FY2023, with further acceleration expected.

Importantly, capacity additions are now driven by utilization rather than speculation. Hyperscalers are making build-or-buy decisions based on demonstrated demand and long-term enterprise commitments, reducing market cyclicality and strengthening investment fundamentals.

4. OTT Growth and Edge Computing Decentralization

India's digital consumption patterns are driving infrastructure decentralization. With 966 million internet connections as of June 2024 and accelerating rural broadband adoption, latency-sensitive applications are expanding beyond Tier-1 metros.

While OTT streaming can tolerate moderate latency (100-200ms), applications like interactive gaming, telemedicine, autonomous vehicles, and real-time analytics require near-instant response times (<20ms). This necessitates edge data center deployment in Tier-2 cities including Pune, Jaipur, Kochi, Bhubaneswar, and Lucknow.

Edge computing creates a hub-and-spoke architecture that supplements rather than replaces hyperscale metropolitan centers. Core processing and storage remain centralised, while edge nodes handle latency-sensitive compute and content caching. This distribution reduces backbone network congestion and improves user experience for regional populations.

For operators, edge deployment offers entry points into markets with lower land costs, faster permitting, and state incentives. However, it requires different operational models, smaller facilities, distributed management, and integration with regional fiber networks.

5. Sustainability as Operational Constraint and Competitive Differentiator

Sustainability has evolved from corporate social responsibility to core operational parameter. Hyperscale and enterprise customers increasingly require colocation partners to meet renewable energy and carbon-efficiency thresholds in procurement decisions.

Leading operators have committed to 100% renewable energy by 2030, supported by long-term Power Purchase Agreements (PPAs), on-site solar installations, and grid-scale renewable partnerships. These commitments are backed by operational changes: advanced cooling systems achieving Power Usage Effectiveness (PUE) near 1.3, water recycling targeting WUE below 2.2 liters per kWh, and battery energy storage systems (BESS) replacing diesel generators.

Policy alignment is strengthening this shift. The Draft National Data Center Policy (2025) proposes fiscal incentives for green-certified facilities, integrating sustainability directly into project economics. States like Gujarat and Rajasthan are positioning themselves as renewable-energy-driven data center destinations, leveraging solar potential and lower land costs.

Long-term renewable PPAs provide price stability over 10-20 years, transforming sustainability from cost center to strategic hedge against energy price volatility. In markets with carbon pricing or potential carbon border adjustments, this creates competitive advantage for early movers.

However, renewable integration faces technical challenges. Solar and wind intermittency requires grid-scale storage or hybrid systems to meet 99.999% uptime requirements. Round-the-clock (RTC) renewable products remain limited, and grid evacuation capacity constrains renewable access in some regions.

Strategic Outlook: Balancing Opportunity and Execution Risk

The Structural Opportunity

India's data center market presents a compelling structural opportunity underpinned by non-cyclical demand drivers. Regulatory mandates (DPDPA, RBI guidelines) formalize domestic infrastructure requirements, particularly for BFSI (32% of demand), government, and healthcare sectors. This creates a demand floor insensitive to economic cycles.

Cost competitiveness strengthens India's position. Development costs near USD 7 per watt and electricity tariffs approximately 20% lower than the United States support attractive unit economics. Infrastructure status classification, state-level incentives, and coastal subsea cable connectivity further enhance competitiveness.

The AI revolution adds a growth multiplier. As rack densities increase and AI workloads proliferate, India's 20% share of global data generation combined with only 3% of global data center capacity creates a structural supply-demand imbalance requiring multi-year capacity expansion.

Demand Diversification Reduces Cyclicality

Demand is becoming multi-sectoral and geographically distributed, reducing exposure to single-sector downturns. OTT media consumption, digital payments, e-commerce, government digitalisation, and AI adoption across healthcare, agriculture, and financial services create resilient, diversified revenue streams.

With 966 million internet connections and growing rural penetration, India's digital expansion supports sustained utilization of both hyperscale and edge infrastructure. This diversity enhances demand resilience and promotes long-term asset utilisation, critical for capital-intensive infrastructure with 15-20 year investment horizons.

Key Risks: Execution Trumps Demand

Despite strong demand fundamentals, execution risks are significant and differentiated across operators. Grid reliability varies widely across regions, making site selection and power redundancy critical to project viability. States with proven "five nines" grid reliability and established renewable energy access offer materially lower execution risk.

Water scarcity in major development zones (Chennai, Mumbai) presents increasing operational constraints, exacerbated by climate variability and regulatory scrutiny. Facilities without closed-loop cooling, rainwater harvesting, and treated sewage water systems face approval delays and long-term sustainability risks.

Global supply chain constraints for GPUs, advanced cooling systems, and power electronics introduce schedule and cost uncertainty. Lead times for specialized equipment can extend 12-18 months, creating project delay risk. Operators with established vendor relationships and bulk procurement capabilities have competitive advantage.

Talent scarcity limits scale-up potential. Despite India's large engineering base, specialized expertise in data center electrical systems, cooling infrastructure, cyber-physical security, and AI cluster management remains scarce. This constrains operational excellence and creates dependence on international expertise.

Regulatory risk stems from state-level policy divergence and evolving national compliance requirements. Multi-state operators face complexity navigating different incentive structures, power tariffs, water policies, and environmental approvals. Policy fragmentation creates execution uncertainty absent national harmonization.

Strategic Imperatives for Market Leadership

- Technology and Operations: Long-term renewable PPAs (15-25 years) with round-the-clock supply, advanced liquid or hybrid cooling systems achieving PUE ≤1.3, modular scalable design supporting rapid capacity expansion, and AI-driven DCIM systems for operational optimization are becoming table stakes.

- Geographic Strategy: Multi-location presence across Tier-1 hubs (Mumbai, Chennai, Hyderabad) and Tier-2 cities (Pune, Jaipur, Noida) reduces concentration risk and enables hub-and-spoke edge architectures. Site selection must balance infrastructure maturity, power reliability, water availability, and state incentives.

- Sustainability and Certification: LEED and IGBC certification are shifting from differentiators to baseline procurement requirements. ESG-linked financing, carbon-neutral commitments, and circular water management are increasingly essential for hyperscale and enterprise client acquisition.

- Vertical Integration: Firms integrating power generation, cooling infrastructure, and fiber connectivity achieve lower lifecycle costs and create switching barriers. The Adani-Google AdaniConneX model exemplifies this approach—combining data centers, renewable energy, and telecommunications infrastructure under unified ownership.

Stakeholder-Specific Strategic Guidance

For Investors:

- Prioritize locations with proven grid reliability (Mumbai, Chennai, Hyderabad) and water resilience

- Assess state incentives in conjunction with long-term power and water economics, not incentives alone

- Consider joint ventures with local operators to mitigate regulatory and execution risks

- Evaluate operators' renewable energy strategies and sustainability certifications as risk factors

- Factor in 24-30 month development timelines and potential supply chain delays in return projections

For Enterprise Users:

- Align Tier certification with workload criticality: Tier IV for mission-critical BFSI and AI applications, Tier III for standard enterprise workloads

- Verify renewable energy sourcing and data sovereignty compliance through third-party audits

- Implement multi-region disaster recovery as standard practice given regional grid and climate risks

- Evaluate colocation partners on PUE, WUE, and uptime track records, not just price

- Build AI-ready infrastructure optionality into long-term contracts to avoid migration costs

For Technology Vendors:

- Prioritize liquid cooling solutions supporting >50 kW rack densities for AI workloads

- Develop energy optimization systems targeting PUE ≤1.3 and WUE ≤2.2 liters/kWh

- Integrate water recycling, rainwater harvesting, and closed-loop cooling into standard offerings

- Expand AI-driven DCIM capabilities for predictive maintenance and dynamic load optimization

- Establish local manufacturing or partnerships to mitigate import dependency and supply chain risks

The Path Forward: Infrastructure Governance as Competitive Advantage

India's data center transformation represents both significant growth opportunity and a test of infrastructure governance. Success will favor participants who integrate engineering innovation, energy strategy, regulatory navigation, and operational excellence, not merely capital deployment.

The market is transitioning from capital-driven expansion to execution-driven differentiation. Operators with reliable power access, advanced cooling capabilities, integrated sustainability practices, and multi-location presence will capture disproportionate market share as demand tightens and client requirements become more sophisticated.

For India to realize its potential as a regional AI and data infrastructure hub, coordinated action across government, operators, technology providers, and utilities is essential. This includes national data center policy harmonization, dedicated power corridors, renewable energy transmission infrastructure, water management frameworks, and talent development programs.

The next 3-5 years will determine whether India captures its structural opportunity or cedes AI workloads and digital sovereignty to offshore facilities. Execution will be decisive.