citiesabc, first_page

Real Estate Tokenisation (Part 1): Digitising the $379 Trillion Industry with Programmable Property

02 Jun 2026

Since the first human hand pressed clay into the shape of a wall at Jericho, nearly eleven thousand years ago — property has been the bedrock grammar of civilisation. Land demarcated the passage from nomad to citizen, from survival to society. The deed, the register, the lease: these were humanity's first programmable contracts, written not in silicon but in stone, papyrus, and the accumulated weight of law.

We stand at a juncture where that ancient grammar is being rewritten. Not destroyed, rewritten. Blockchain technology and the tokenisation of real-world assets represent the most significant structural transformation of property ownership since the Magna Carta codified rights against arbitrary seizure in 1215. Where once a deed required a notary, a registry, and weeks of administrative friction, a smart contract executes instantaneously, autonomously, and with mathematical precision that no human institution can rival.

Tokenisation is not a cryptographic trend. It is the foundational architecture for the next global financial cycle, the moment when the oldest store of human value becomes programmable, auditable, and universally accessible.

This research does not merely document platforms, protocols, and percentages. It argues a philosophical position: that the democratisation of real estate ownership through tokenisation is a moral as much as a financial transformation. Across history, the ownership of land has been among the most reliable mechanisms for inter-generational wealth accumulation and among the most systematically denied to the many in favour of the few. A farmer in the Mekong Delta, a teacher in Lagos, a software engineer in Lisbon: none has historically possessed the capital to participate in the commercial real estate markets of London, Singapore, or New York. Tokenisation changes that axiom.

Drawing on direct experience co-founding and leading the LynKey platform in Vietnam, one of the pioneering tokenised time-sharing and real estate ecosystems in Southeast Asia, alongside a decade of research published across Businessabc.net, IntelligentHQ.com, Citiesabc.com, and the AI.DNA Newsletter series, this analysis synthesises global case studies, technical architecture, academic scholarship, and philosophical conviction into a single coherent argument: the programmable city is not coming. It is already being built.

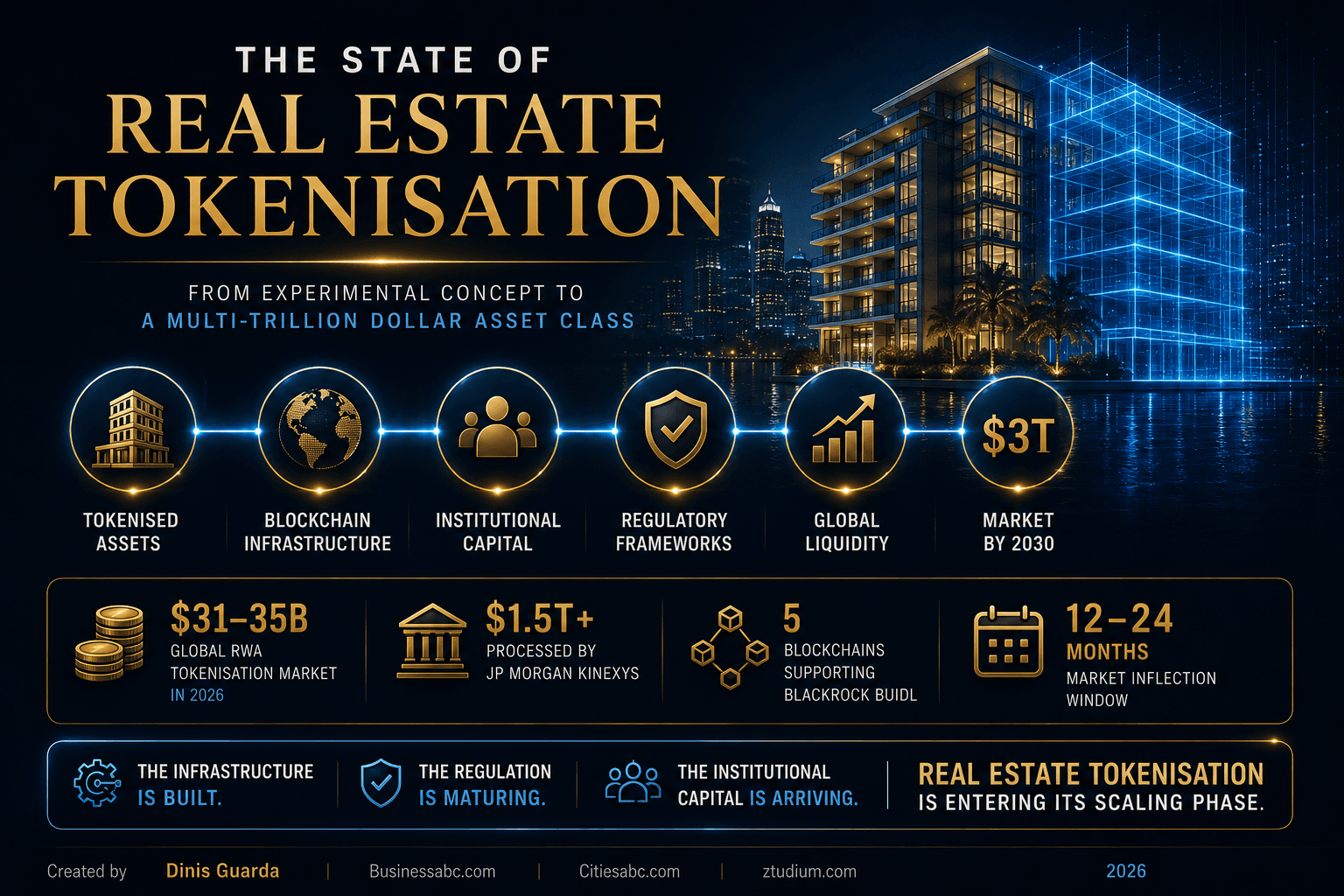

The State of the Market

Real estate tokenisation — the conversion of property ownership rights into digital tokens recorded on a distributed ledger — has transitioned from experimental proof-of-concept into a multi-billion-dollar asset class. The global Real-World Asset (RWA) tokenisation market reached approximately $31–35 billion in 2026, with real estate constituting one of its primary growth vectors. Leading forecasters project the sector reaching a standalone market capitalisation of $3 trillion by 2030 under favourable regulatory conditions (Boston Consulting Group, 2024; Citi GPS, 2023; McKinsey & Company, 2024).

The infrastructure pipes are already built. JP Morgan's Kinexys platform has processed over $1.5 trillion in transaction volume on permissioned Ethereum. BlackRock's BUIDL fund operates across five blockchains. The United States and European Union are finalising securities treatment for tokenised assets. The 12-to-24-month inflection window is not approaching, it has opened.

The Architecture of Property: From Deed to Digital Token

What Is Real Estate Tokenisation?

Real estate tokenisation is the process of converting the ownership rights of a physical property, whether a parcel of land, a commercial office tower, a residential apartment, or the rental cash flows generated by it, into digital tokens recorded on a blockchain network. Each token represents a fractional, mathematically precise share of the underlying asset, governed by immutable smart contract logic rather than paper-based trust and institutional intermediaries.

The asset itself does not move onto the blockchain. What moves is the legal claim to it. Through a carefully engineered combination of off-chain legal structures and on-chain digital representations, tokenisation creates a programmable proxy that confers the economic rights of ownership, income distributions, capital appreciation, and governance voting, without requiring the wholesale reform of national land registry systems.

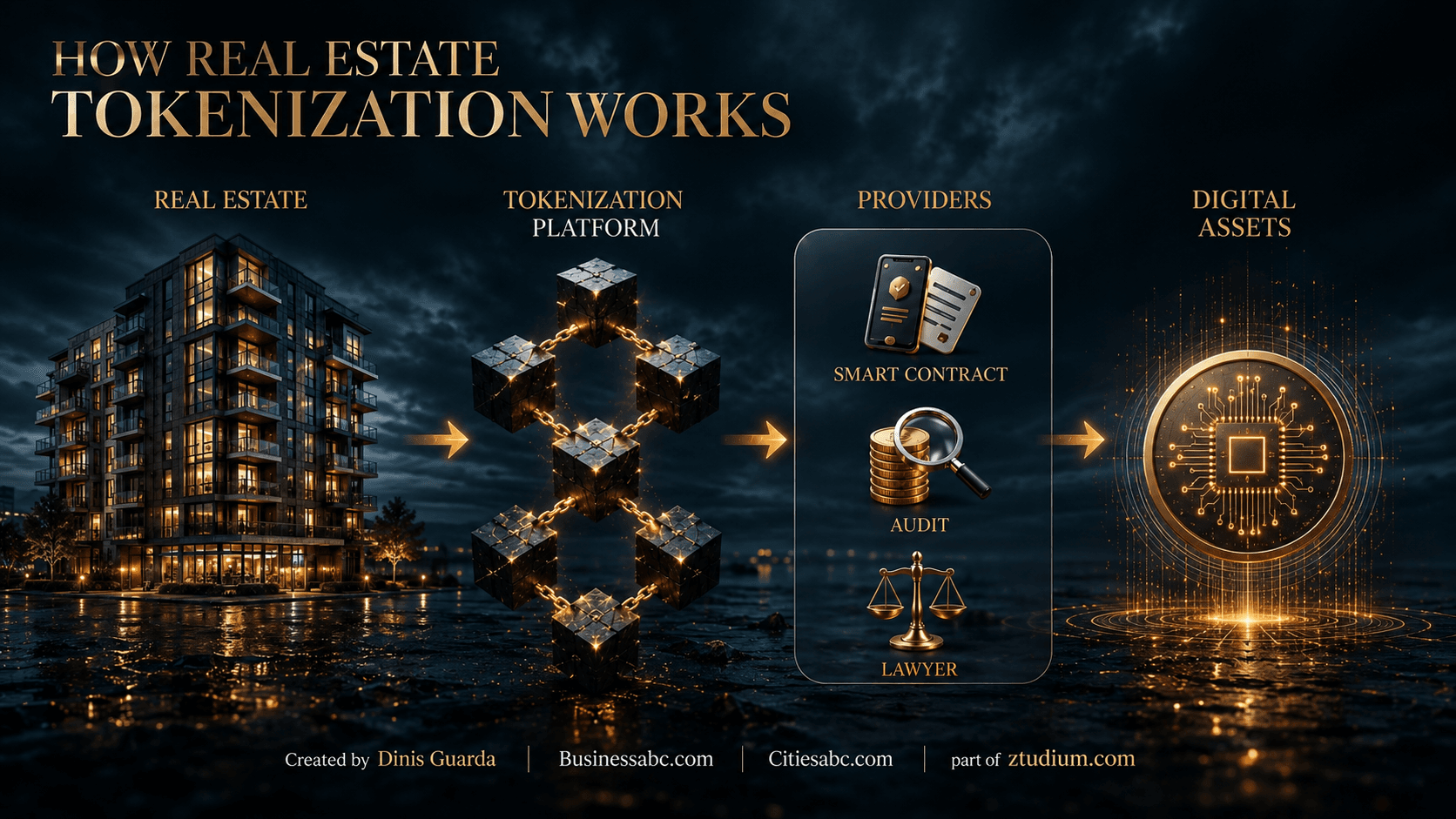

How It Works: The Full Architecture

The mechanics unfold in five distinct layers.

- Asset Selection. A developer, fund manager, or platform identifies a specific property, a commercial skyscraper in Zurich, a resort villa in Bali, a multi-family residential building in Detroit, or a premium beachfront in Vietnam. Due diligence is performed on title, valuation, existing encumbrances, and rental yield projections.

- Legal Wrapper Creation. Because direct on-chain tokenisation of a property's legal title remains heavily restricted under traditional real estate law in most jurisdictions, platforms universally employ a proxy structure: the Special Purpose Vehicle (SPV). The property is transferred into an SPV, typically a Wyoming LLC, a Cayman Islands entity, or a DAO LLC, which becomes the legal owner of record. Investors then acquire tokens representing equity stakes in the SPV rather than the property directly. This separation between digital instrument and physical asset is the legal cornerstone of the entire industry.

- Smart Contract Deployment. Smart contracts are written to govern the lifecycle of the digital assets: how fractional shares are allocated, how rental income is distributed, how voting on property decisions is conducted, and under what conditions tokens may be transferred or redeemed. These contracts are audited, deployed to a chosen blockchain network, and become the binding operational rules of the investment.

- Token Generation and Primary Sale. The equity of the SPV is divided into thousands of digital "security tokens." These are offered to investors via a primary marketplace, either a regulated security token offering (STO) or a compliant private placement, typically at minimum entry points ranging from $50 to £1,000.

- On-Chain Management. Once issued, token holders receive automated income distributions — rental yields, hotel revenue shares, paid directly to their crypto wallets, typically in stablecoins. Governance rights may allow holders to vote on property decisions. Secondary market sales can be executed 24/7 on compliant digital trading platforms.

The Five Structural Pillars

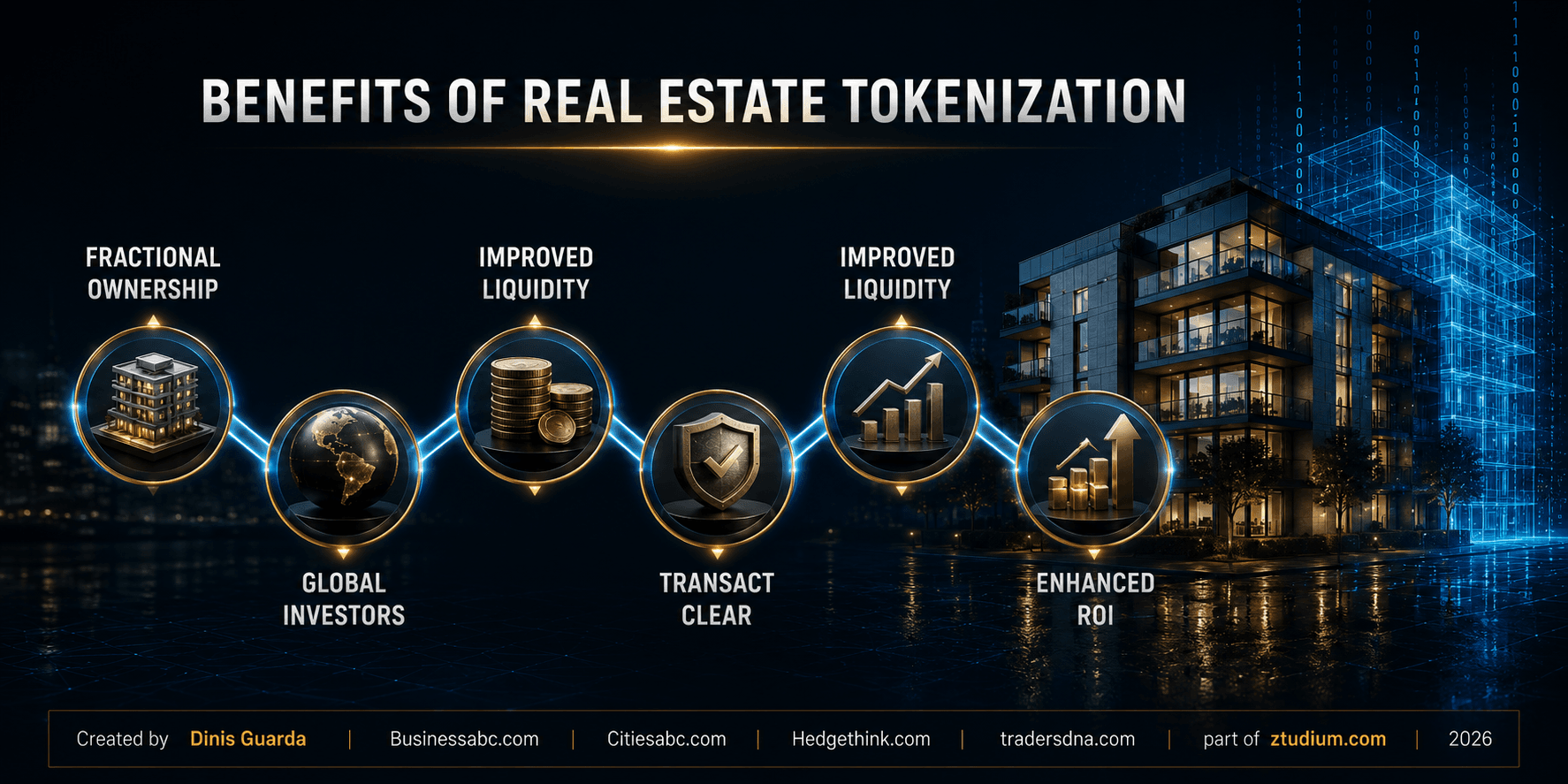

The transformative value proposition of real estate tokenisation rests on five core dimensions.

- Fractional Ownership enables investors to acquire meaningful stakes in premium commercial buildings or luxury developments with entry capital as low as $50, markets that previously required six-figure minimum investments.

- Democratisation opens an asset class historically restricted to institutions, sovereign wealth funds, and the ultra-wealthy to retail and mid-income investors globally.

- Liquidity Injection compresses timelines that once stretched across months. Tokenised stakes can be listed and transferred on 24/7 digital secondary marketplaces, rewriting the fundamental illiquidity assumption of physical real estate.

- Operational Efficiency flows from smart contracts automating the administrative stack — ownership tracking, KYC/AML verification, dividend calculation, governance tabulation — eliminating expensive intermediaries.

- Programmable Finance is perhaps the most far-reaching dimension. Tokenised real estate can serve as programmable collateral, be deployed as staking instruments, integrated with AI treasury agents, or combined with stablecoins into sophisticated yield-bearing financial structures. This is where real estate ceases to be a passive store of value and becomes an active component of a programmable financial architecture.

Tokenised Real Estate vs. REITs

The natural comparison for real estate tokenisation is the Real Estate Investment Trust, the dominant vehicle for retail property exposure over the past half-century. The differences are structural, not cosmetic.

Where a REIT offers indirect exposure to a diversified portfolio, a tokenised instrument delivers direct investment in a single, identified property, with embedded governance rights over that specific asset rather than the standard corporate governance of a public equity structure. Fee structures are materially lower through smart contract automation. Trading operates on decentralised ledgers and secondary digital markets rather than traditional stock exchanges. And regulatory oversight falls under security token frameworks, FCA, SEC, MAS, MiCA, rather than the established securities architecture that governs REITs.

The honest caveat: secondary market liquidity in tokenised real estate remains maturing, while REIT liquidity on major exchanges is deep and established. This distinction matters.

Barriers, Risks, and Honest Assessment

The enthusiasm for real estate tokenisation must be tempered by a rigorous accounting of the obstacles that remain. This analysis does not traffic in techno-utopianism. The following barriers are structural, not superficial.

Regulatory Fragmentation

Most tokenised real estate instruments are legally classified as regulated securities. Platforms must navigate a labyrinthine patchwork of national frameworks: the Financial Conduct Authority (FCA) in the United Kingdom, the Securities and Exchange Commission (SEC) in the United States under Regulation D and Regulation A+, the Markets in Crypto-Assets Regulation (MiCA) in the European Union, the Monetary Authority of Singapore (MAS) under the Securities and Futures Act, and a constellation of emerging frameworks across Asia-Pacific, the Gulf, and Latin America.

The absence of a harmonised global standard creates structural friction for cross-border offerings. A token legally structured under Wyoming LLC law may not satisfy German securities law. A platform regulated by the FCA may face re-licensing costs to serve Singapore retail investors.

Land Registry Integration

Property ownership records in most jurisdictions still rely on localised, paper-based, or non-blockchain land registries. The critical link between the on-chain digital token and the off-chain legal title remains mediated by traditional institutions — notaries, land registries, courts. Until national land registries themselves migrate onto interoperable digital infrastructure (as Bergen County, New Jersey is beginning to do with Avalanche), this gap represents both a legal risk and an operational bottleneck.

The Liquidity Myth

Perhaps the most commonly misrepresented aspect of real estate tokenisation is secondary market liquidity. While blockchain enables 24/7 trading in principle, practical liquidity depends upon a sufficiently large pool of daily active buyers. As empirical analysis of RealT token pricing demonstrates, secondary market prices can diverge meaningfully from underlying Net Asset Value (NAV) due to thin order books and varying pricing methodologies. The promise of instant liquidity remains aspirational in most markets; the reality is a spectrum from near-liquid, mature platforms with thousands of active users, to effectively illiquid, where smaller offerings face limited secondary market activity.

Smart Contract Vulnerability

The same immutability that makes smart contracts powerful makes their errors catastrophic. Code bugs, oracle manipulation, reentrancy attacks, and key management failures have collectively cost the broader DeFi ecosystem billions of dollars. Real estate tokenisation platforms must invest heavily in formal code verification, third-party security audits, and insurance protocols to safeguard the underlying property rights embedded in smart contract logic.

What Developers and Retail Investors Must Know

For property developers seeking capital, token offerings can access a global retail investor base that traditional private placements cannot reach, potentially lowering the cost of capital. But SPV structuring costs, legal opinions, smart contract audits, and regulatory compliance represent material upfront expenses that must be modelled into the capital raise. Developers surrender a degree of governance: token holders may have contractual rights to vote on material property decisions. And reputational and regulatory risk accrues if secondary market token prices depart significantly from advertised valuations.

For retail investors in fractional digital assets, the checklist is equally unforgiving. Rigorous due diligence on the legal wrapper is non-negotiable: who owns the SPV, under which jurisdiction, and what legal recourse exists if the platform fails? Secondary market liquidity must be assessed realistically, not against theoretical blockchain capability, but against daily active user counts and 30-day average trading volumes. The yield structure must be verified: are rental distributions genuinely automated and auditable on-chain, or reliant on manual platform management? And regulatory status must be confirmed: is the platform registered with the relevant securities authority?

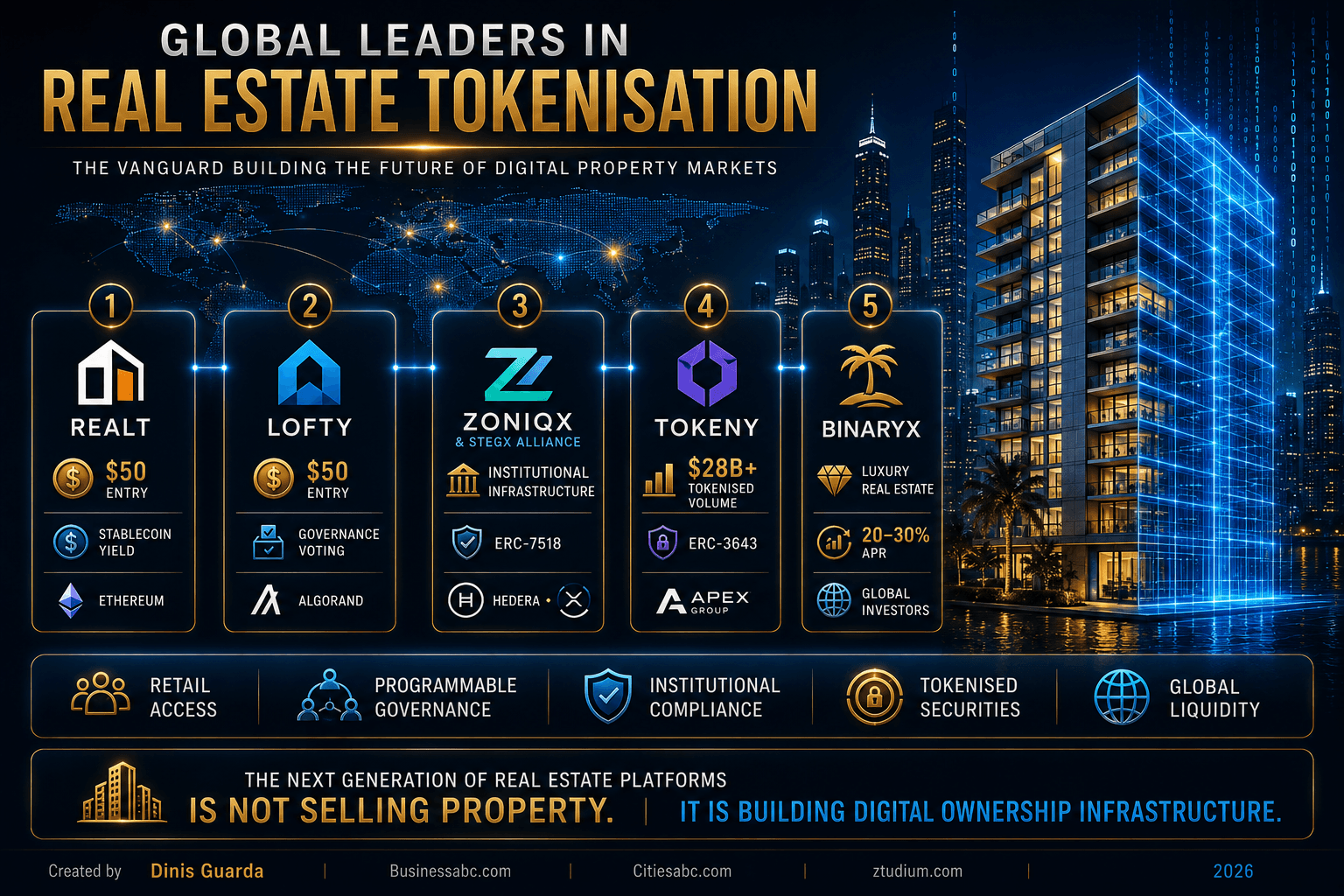

The Global Platforms: The Vanguard of Real Estate Tokenisation

RealT (United States)

One of the world's most successful retail-facing tokenisation platforms, RealT has systematically fractionalised U.S. residential and multi-family rental properties into micro-tokens available from $50 per unit. Employing Wyoming LLC Special Purpose Vehicles to legalise fractional shareholding, the platform automates daily rental yields in stablecoins directly to investors' wallets via Ethereum and Gnosis Chain. RealT demonstrates that the mechanics of automated property income distribution — once the province of institutional funds — can be delivered to a retail investor with a crypto wallet and a $50 note.

Lofty (United States)

Built on the Algorand blockchain, Lofty enables instant fractional investment in U.S. residential real estate with $50 minimum entry. Its distinguishing architectural feature is direct token-holder governance: investors can vote on property management decisions — whether to raise rents, authorise repairs, or adjust leasing terms — via smart contract ballots. This represents an early model of what this analysis describes as the "programmable governance layer" of tokenised assets: not merely income distribution but distributed decision-making encoded into ownership itself.

Zoniqx & StegX Alliance (Global Institutional)

A compliance-first institutional powerhouse, Zoniqx operates Tokenised Asset Lifecycle Management (TALM) architecture — digitising commercial real estate using institutional standards (ERC-7518) across the Hedera and XRP Ledger networks. Its alliance with StegX has generated over $100 million in institutional real estate tokenisation pipeline, targeting European and U.S. asset managers with automated multi-chain compliance engines. Zoniqx represents the B2B infrastructure layer that enables traditional fund managers to tokenise without building proprietary blockchain infrastructure.

Tokeny (Europe)

Backed by the Apex Group and operating as Europe's leading institutional tokenisation engine, Tokeny provides white-label smart contract technology and modular compliance architecture based on the ERC-3643 standard — the industry benchmark for permissioned, KYC/AML-enforced security tokens. Having facilitated over $28 billion in tokenised volume across real estate and other asset types, Tokeny has become the foundational infrastructure provider for institutional issuers seeking regulatory-grade token issuance without reinventing the compliance wheel.

Binaryx (Global / APAC)

Specialising in luxury real estate and international rental properties — most famously fractionalising luxury resort villas in Bali — Binaryx combines fractional ownership of high-demand vacation rentals with Wyoming DAO legal wrappers. Its headline yields, frequently in the 20–30% APR range, reflect the premium pricing of high-occupancy tourism real estate rather than speculative token mechanics, offering a compelling case study in how tokenisation can package niche hospitality economics for global retail capital.

The programmable city is not a future hypothesis. It is a present construction. The platforms enumerated above are not experiments , they are operational infrastructure, processing real transactions, distributing real yields, and encoding real governance into the oldest store of human value. The philosophical transformation that began when the first deed was pressed into clay at Jericho is entering its next chapter — and for the first time in eleven thousand years, the architecture of that chapter is open to everyone.

Regulation and Governance: The Legislative Architecture

The transition of real estate tokenisation from private platform experimentation to government-endorsed infrastructure represents the most significant structural signal in the sector. Regulatory frameworks across the world's major economies are no longer asking whether tokenised property instruments are legitimate — they are asking how to classify, supervise, and scale them.

In the United States, the Securities and Exchange Commission's progressive alignment of capital treatment frameworks for tokenised securities — alongside the Office of the Comptroller of the Currency's issuance of a National Bank Charter to BitGo, creating BitGo Bank & Trust in the same federal regulatory tier as traditional banks — signals a fundamental shift in the regulatory posture of the world's largest financial market toward on-chain asset infrastructure.

In the European Union, the Markets in Crypto-Assets Regulation (MiCA), effective 2024, provides the first comprehensive regulatory framework for crypto-assets in a major economy. MiCA's treatment of asset-referenced tokens and e-money tokens creates regulatory clarity for stablecoin-denominated real estate yield distributions operating across EU member states — a critical enabling condition for cross-border property tokenisation at scale.

In Vietnam, Resolution No. 05/2025/NQ-CP established a five-year nationwide sandbox for trading digital tokens backed by real economic assets, making Vietnam one of the first Southeast Asian nations to explicitly legitimise tokenised real estate and tourism instruments and the legislative framework within which the LynKey platform operated.

Singapore's Monetary Authority of Singapore (MAS), through its Project Guardian wholesale market tokenisation initiative, has produced foundational frameworks for tokenised fund structures and cross-border settlement, establishing the city-state as the de facto regulatory hub for APAC real estate tokenisation. And in the UAE, the Virtual Assets Regulatory Authority (VARA) in Dubai and the Abu Dhabi Global Market's Financial Services Regulatory Authority have enacted comprehensive virtual asset frameworks that explicitly accommodate real estate tokenisation, opening the Gulf's substantial sovereign wealth and private real estate capital to blockchain-based instruments.

The legislative direction across all major jurisdictions is consistent: tokenised real estate is being absorbed into the formal architecture of financial regulation, not treated as an exemption to it. That transition from regulatory ambiguity to regulatory clarity is, historically, the precondition for institutional capital at scale.

Sources

- Baum, A. (2021). Tokenisation: The Future of Real Estate Investment? Oxford Future of Real Estate Initiative, Saïd Business School, University of Oxford.

- Benedetti, H. & Rodríguez-Garnica, G. "Real Estate Tokenization: A Conceptual Framework." Journal of Property Research.

- Boston Consulting Group. (2024). Relevance of On-Chain Asset Tokenization.

- Citi GPS. (2023). Money, Tokens, and Games: Blockchain's Next Billion Users and Trillions in Value. Citigroup Global Perspectives and Solutions.

- McKinsey & Company. (2024). Tokenized Financial Assets: From Pilot to Scale.

- Roland Berger. Approaching the Tokenization Tipping Point.

- Tokeny & ERC-3643 Association. Real Estate Tokenization Handbook.

- Vietnam Resolution No. 05/2025/NQ-CP — National Sandbox for Digital Token Trading.

- Avalanche / AvaCloud. Bergen County, New Jersey Land Registry Initiative.

- BlackRock. BUIDL Tokenised Fund — Multi-Chain Deployment Documentation.

- JPMorgan. Kinexys (formerly Onyx) — Platform Transaction Volume Reports.

- BitGo. OCC National Bank Charter Filing and Custody Architecture Documentation.

- Guarda, D. "The Programmable Economy: Tokenisation, AI Agents and the Future of Value." Businessabc.net / IntelligentHQ.

- Guarda, D. "Smart Cities, Digital Twins, and the Urban Tokenisation Agenda." Citiesabc.

- Guarda, D. "Web3, Blockchain, and the Architecture of Trust." IntelligentHQ / Businessabc.net.