The Businessabc UK SME Lending Atlas 2026: Top UK 100-Lender Intelligence Report

UK SME lending, Business loans UK, SME finance, Business funding, Alternative finance UK, Businessabc

08 Jul 2026

From High-Street Term Debt to Embedded Revenue Finance — A Strategic Map of the £68 Billion UK SME Finance Market

Capital is the oxygen of enterprise. Today, the challenge is no longer whether funding exists, but whether businesses can find the right lender, on the right terms, at the right time.

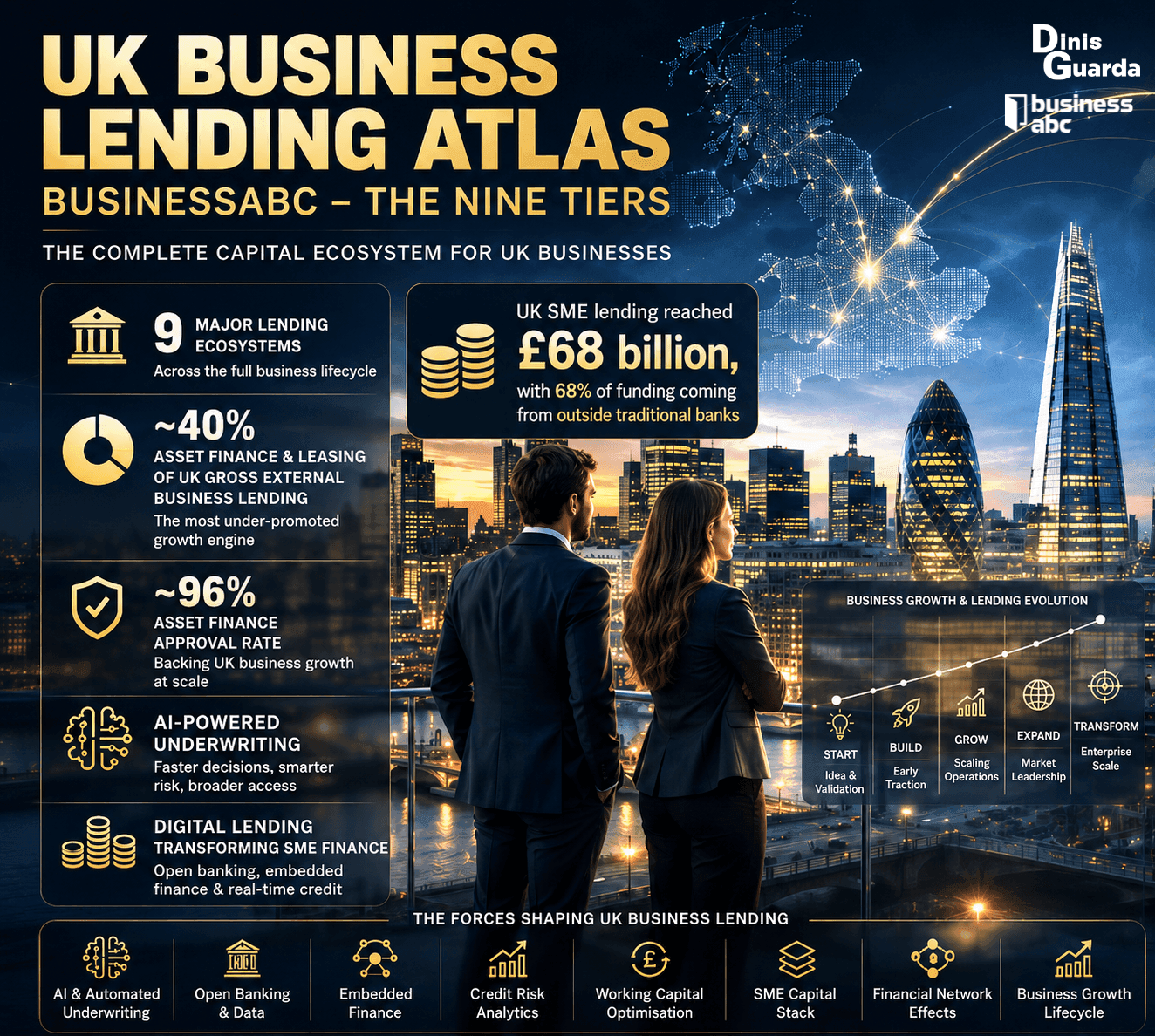

This atlas was created to help UK SMEs navigate an increasingly complex lending landscape. The market has evolved beyond the high street into a diverse ecosystem of challenger banks, specialist lenders, fintechs, brokers, and alternative finance providers. In 2025, UK SME lending reached £68 billion, with 68% of funding coming from outside traditional banks. More choice has created greater opportunity but also greater complexity.

Technology has transformed business finance. Open banking, embedded finance, alternative-data underwriting, and AI-driven decision-making have made funding faster and more accessible than ever before. Yet the UK still faces a £22 billion SME funding gap, with four in five businesses reporting missed growth opportunities due to limited access to capital.

That is why this atlas exists.

It provides a practical guide to the UK's 100 most significant business lenders, helping founders, brokers, advisers, investors, and policymakers understand the market and identify the right financing partner.

This publication also forms part of the Businessabc.net Capital Hub, our initiative to build trusted digital infrastructure that connects businesses with funding, expertise, and growth opportunities.

This atlas can be used as a working resource to compare lenders, understand the market, and find the funding partner best suited for a business.

The right capital, at the right moment, can transform ambition into growth.

The UK business lending market in 2026 is a £68 billion, nine-tier, structurally fragmented ecosystem in which non-bank and challenger lenders now provide more than two-thirds of all SME debt finance.

This document maps the 100 most consequential active lenders, classifies them into nine functional tiers, and provides a strategic framework for matching businesses to capital sources by stage, sector, security, and speed-of-funding requirements.

Key Market Findings

- UK SME lending reached £68 billion in 2025, the second-highest level in 13 years, with 68% provided by challenger banks, specialist lenders, and non-bank finance providers.

- Asset finance has the highest approval rate (96%), compared with 61% for overdrafts and 44% for bank loans.

- UK SMEs face a £22 billion funding gap, with four in five businesses reporting missed growth opportunities due to limited access to capital.

- Brokered lending totalled £33 billion in 2025, up 25% year-on-year, making brokers a key distribution channel for SME finance.

- Funding Circle accounts for over half of UK non-bank business lending, highlighting the growing importance of digital lending platforms.

- The Bank Referral Scheme requires the UK's largest banks to refer declined SME applicants to designated finance platforms, expanding access to alternative funding.

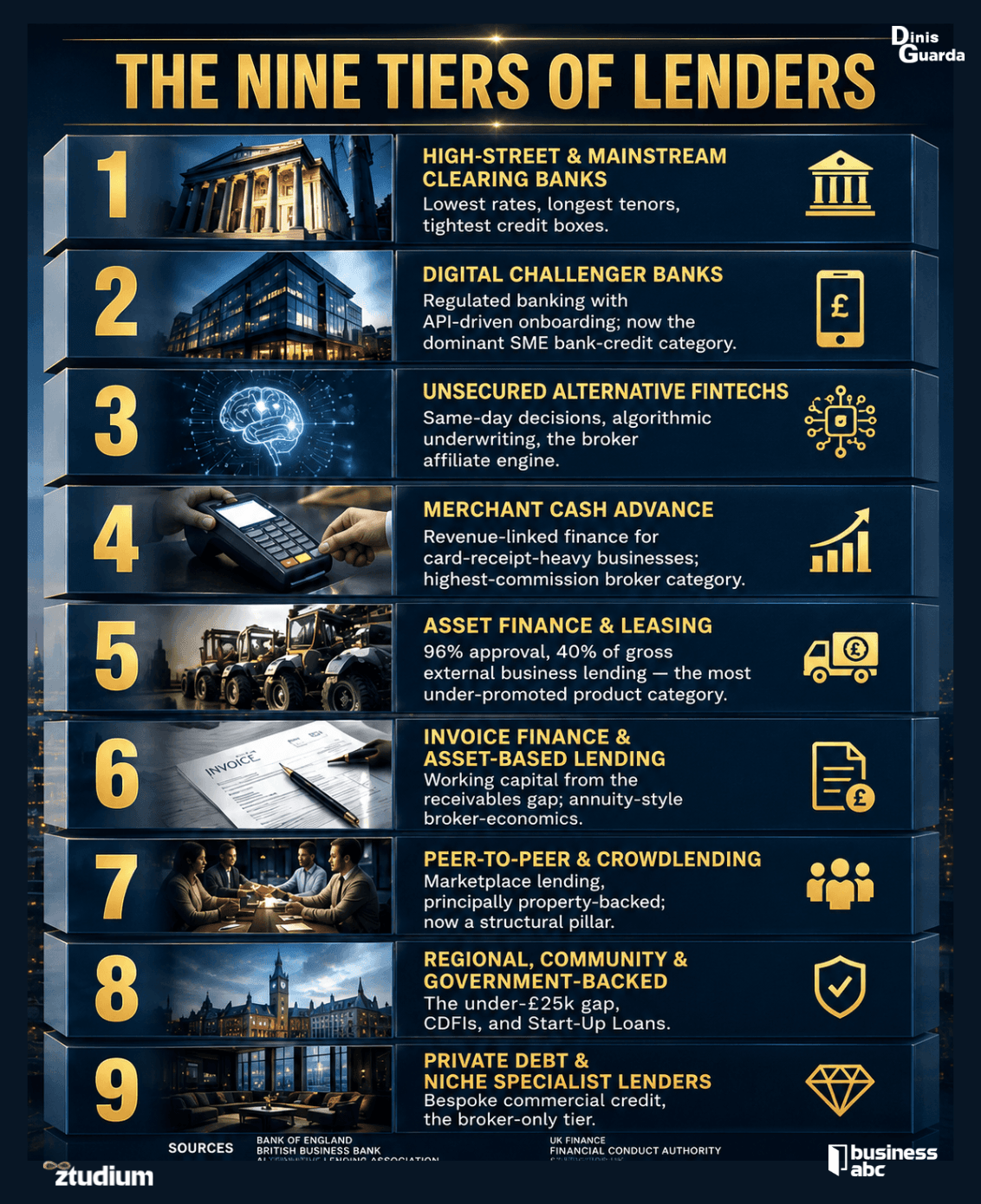

The Nine Tiers of Lenders

- Tier 1 — High-Street & Mainstream Clearing Banks: lowest rates, longest tenors, tightest credit boxes.

- Tier 2 — Digital Challenger Banks: regulated banking with API-driven onboarding; now the dominant SME bank-credit category.

- Tier 3 — Unsecured Alternative FinTechs: same-day decisions, algorithmic underwriting, the broker affiliate engine.

- Tier 4 — Merchant Cash Advance: revenue-linked finance for card-receipt-heavy businesses; the highest-commission broker category.

- Tier 5 — Asset Finance & Leasing: 96% approval, 40% of gross external business lending — the most under-promoted product category in the market.

- Tier 6 — Invoice Finance & Asset-Based Lending: working capital from the receivables gap; annuity-style broker economics.

- Tier 7 — Peer-to-Peer & Crowdlending: marketplace lending, principally property-backed; now a structural pillar.

- Tier 8 — Regional, Community & Government-Backed: the under-£25k gap, CDFIs, and Start-Up Loans.

- Tier 9 — Private Debt & Niche Specialist Lenders: bespoke commercial credit, the broker-only tier.

Strategic Implications

For business owners, the operating principle is sequencing: high-street first if speed is not critical and security exists; challenger second if speed matters and the credit story is clean; alternative-finance third if either the timeline or the credit box demands it.

For brokers and introducer-network operators, affiliate economics are concentrated in Tiers 3, 4, 5 and 6 — these are the tiers where lender-direct programmes pay commission, where decision speed drives conversion, and where aggregator panels provide deal flow.

For platforms, the opportunity is curatorial: to become the trusted intelligence layer that routes intent to capacity. That is the role Businessabc.net is building.

The UK Lending Market

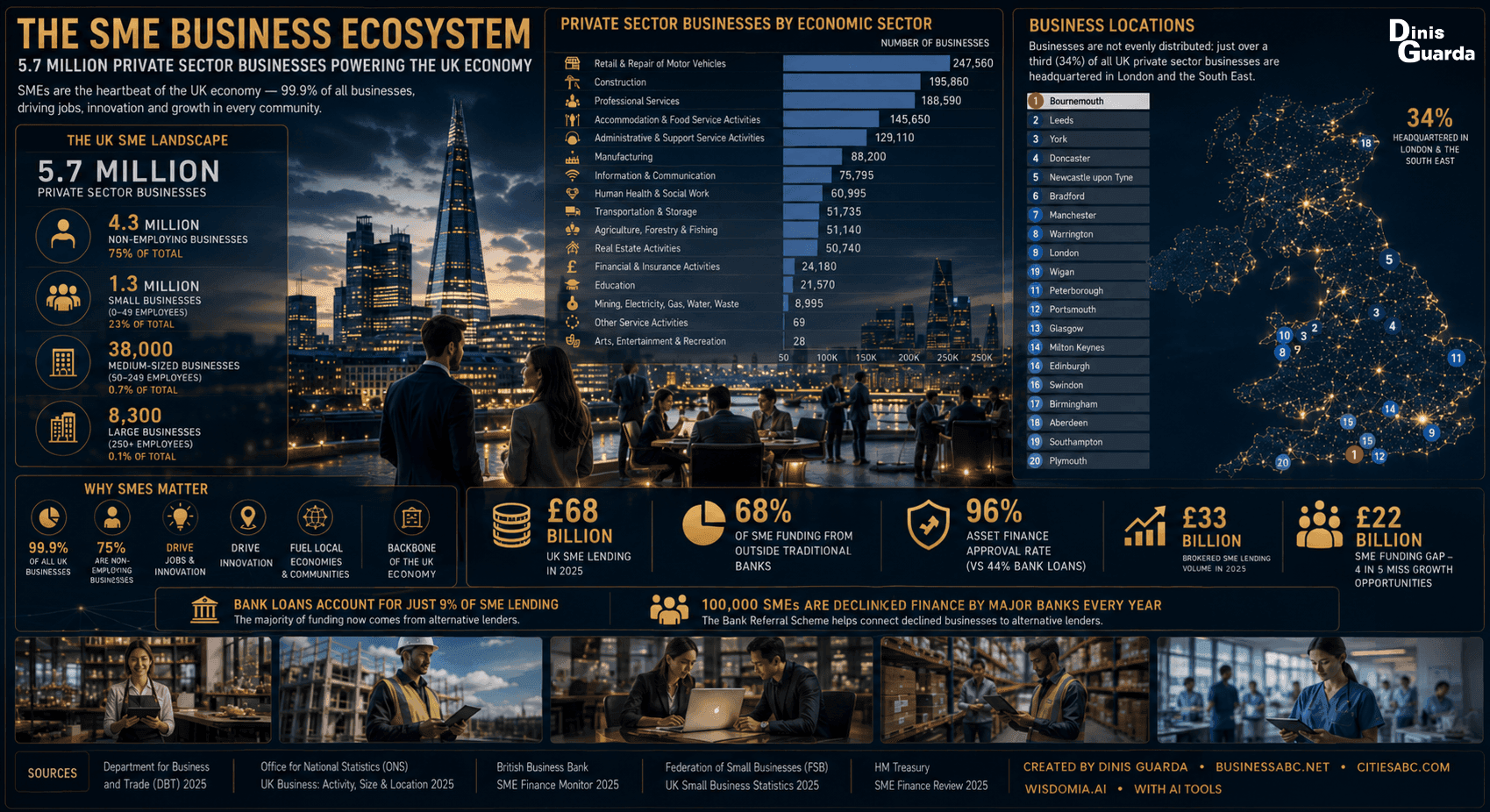

There are an estimated 5.7 million private sector businesses in the UK. The vast majority (99.9%) are small and medium-sized enterprises (SMEs).

The makeup of the UK's business population is as follows:

- Non-employing businesses: ~4.3 million (75% of the total) have no employees other than the owner(s).

- Small businesses (0 to 49 employees): ~1.3 million.

- Medium-sized businesses (50 to 249 employees): ~38,000.

- Large businesses (250+ employees): ~8,300.

Businesses are not evenly distributed; just over a third (34%) of all UK private sector businesses are headquartered in London and the South East of England.

To understand the lender landscape, the market must first be sized accurately and read structurally. The UK SME credit market in 2026 is not the same as it was in 2016. The composition, the pricing logic, the distribution architecture, and the regulatory framework have each shifted in directions that compound to favour informed borrowers and intermediated demand — and that disadvantage those who continue to operate as if Lloyds, Barclays, and HSBC were the only three doors in the building.

Market Size, Composition, and Growth

Gross SME lending reached approximately £68 billion in 2025, according to the British Business Bank, making it the second-highest level in thirteen years after the 2020 pandemic peak. Behind this headline lies a major structural shift.

Challenger and specialist banks increased their share of SME lending from 39% in 2012 to 60% in 2025. Including non-bank lenders, more than two-thirds of SME finance now comes from outside the traditional high-street banks, marking a lasting transformation of the market.

The product mix has evolved as well. Traditional bank loans now account for just 9% of SME lending, while asset finance represents around 40% of gross external business lending, with the industry book reaching £44.5 billion.

Leasing adoption has more than doubled, rising from 6% in 2012 to 13% in 2025, particularly for equipment and machinery. Today's SMEs increasingly finance assets, factor invoices, and access revenue-based funding rather than relying on conventional term loans.

The £22 Billion Funding Gap

Behind the growth numbers, the structural shortfall remains. The funding gap — defined as the difference between SME demand for capital and the capital actually advanced — sits at approximately £22 billion.

Four in five UK SMEs report having missed growth opportunities because they could not access the required funding. Loan approval rates, which sat at seventy-four per cent in 2019, have recovered only to fifty-three per cent in 2025. Persistent structural gaps affect smaller loans (under £25,000), early-stage businesses, and intellectual-property-heavy companies for which traditional credit models perform poorly.

The British Business Bank estimates that 100,000 SMEs are declined for finance each year by the major banks alone. Many cancel their growth plans rather than explore alternatives.

This is the structural inefficiency that the Bank Referral Scheme, the broker market, and the platform layer collectively exist to solve — and the inefficiency that any business or intermediary that operates intelligently can convert into a competitive advantage.

The Bank Referral Scheme — A Regulated Traffic Engine

Introduced in November 2016 under the Small Business, Enterprise and Employment Act 2015, the Bank Referral Scheme requires the UK's nine largest banks to offer rejected SME loan applicants the option of being referred to one of three designated finance platforms: Funding Options, Funding Xchange, and Alternative Business Funding.

These platforms share applicants' details with panels of alternative lenders, transforming a bank rejection into a direct route to other funding providers. For lenders and brokers, the scheme is a high-quality source of qualified demand. For SMEs, accepting a referral can significantly improve access to finance.

The Bank Referral Scheme has helped establish alternative finance as a mainstream complement to traditional banking, strengthening competition and expanding funding options for UK businesses.

The Broker Economy

Brokered SME lending reached £33 billion in 2025, up 25% year-on-year. According to the National Association of Commercial Finance Brokers (NACFB), 32% of SMEs secured funding through brokers, a ten-point increase from the previous year, making brokers the primary distribution channel for non-bank business finance.

Commission structures vary by product. Unsecured business loans typically pay 1–6% of funded value, while merchant cash advances offer the highest commissions at 4–8%. Asset finance and invoice finance combine upfront commissions with recurring fees, while specialist and private debt remains a broker-led market with lower volumes but higher fees.

For platforms serving business audiences, the implication is clear: connecting qualified borrowers with suitable lenders has become both a valuable commercial opportunity and a better service for SMEs seeking finance.

The Diamandis Frame — From Scarcity to Abundance

Peter Diamandis describes abundance as technology transforming scarcity into widespread availability. UK business finance is undergoing exactly that shift. Where securing a business loan once required branch visits, extensive paperwork, and weeks of waiting, businesses can now access algorithmically underwritten loans in under two hours, merchant cash advances within 24 hours, invoice finance within hours, and asset finance before equipment is delivered.

Technology has made capital far more accessible, but accessibility does not guarantee transparency. Pricing remains opaque, lending terms vary widely, and choosing the wrong finance solution can be costly.

The role of intelligence layers, atlases like this one, Businessabc.net, finance platforms, and professional brokers, is to turn abundant capital into informed decisions, helping businesses find the right funding, not simply more funding.

The Nine-Tier Atlas

What follows is the complete 100-lender intelligence dossier, structured into nine functional tiers. Within each tier, lenders are profiled by loan range, decision-speed band, sector specialism, and affiliate distribution route. The four route codes operate as a guide for both businesses (where do I apply?) and intermediaries (how do I get paid?):

- Direct — the lender operates its own affiliate or broker programme accepting direct applications and paying commission.

- Aggregator — distribution is principally via panel-based aggregators such as Swoop, Funding Options, Funding Xchange, and Tide Funding.

- BRS / Aggregator — bound by the Bank Referral Scheme as a participating bank; alternative-finance routes accept inbound flow from designated platforms.

- Institutional — relationship-led with no public affiliate programme; access via direct corporate finance teams or specialist broker introductions.

Decision-speed bands reflect typical funding times from the complete application to drawdown for a borderline-qualifying applicant: same day to 48 hours, 3–10 days, 2–6 weeks, or 6+ weeks.

Tier 1 — High-Street & Mainstream Clearing Banks

The bedrock. Lowest pricing, longest tenors, deepest balance sheets — but tightest credit boxes and slowest decisions. Best for established businesses with 2+ years of audited accounts, tangible security, and patience for committee-led underwriting.

Sweet spot: £250k–£25m+ secured term loans, commercial mortgages, asset finance, treasury and FX. Affiliate dynamics: Direct affiliate programmes are rare. Reach is through the Bank Referral Scheme (rejected applicants flow to designated platforms) and through aggregator panels.

# | Lender | Loan Range | Speed | Specialism | Route |

| 1 | NatWest | £25k–£10m+ | 2–6 weeks | Comprehensive commercial loans, asset finance, structured corporate lending | BRS / Aggregator |

| 2 | HSBC UK | £10k–£50m+ | 2–6 weeks | International trade finance, business loans, commercial mortgages | BRS / Aggregator |

| 3 | Barclays Business Banking | £1k–£25m+ | 2–6 weeks | Unsecured loans to £25k, larger secured commercial debt | BRS / Aggregator |

| 4 | Lloyds Bank | £1k–£25m+ | 2–6 weeks | Fixed and variable rate business loans up to 25-year terms | BRS / Aggregator |

| 5 | Santander UK | £2k–£25m+ | 2–6 weeks | Growth capital, tailored asset-backed corporate solutions | BRS / Aggregator |

| 6 | Bank of Scotland | £1k–£25m+ | 2–6 weeks | Regional business banking, agricultural finance, development loans | BRS / Aggregator |

| 7 | Royal Bank of Scotland | £1k–£25m+ | 2–6 weeks | SME overdrafts, capital enterprise loans, invoice finance | BRS / Aggregator |

| 8 | Virgin Money | £25k–£10m+ | 2–6 weeks | Base-rate-linked and fixed business loans, commercial mortgages | BRS / Aggregator |

| 9 | TSB Bank | £1k–£1m | 3–10 days | Flexible business loans and overdraft facilities for local SMEs | BRS / Aggregator |

| 10 | Metro Bank | £25k–£25m | 3–10 days | Commercial loans with dedicated relationship managers | BRS / Aggregator |

| 11 | Co-operative Bank | £25k–£10m | 2–6 weeks | Ethical business banking, variable asset finance options | Institutional |

| 12 | Clydesdale Bank | £25k–£10m+ | 2–6 weeks | Asset finance, working capital, commercial property loans | BRS / Aggregator |

| 13 | Ulster Bank | £25k–£10m+ | 2–6 weeks | Primary commercial and corporate debt for Northern Ireland | BRS / Aggregator |

| 14 | Danske Bank UK | £25k–£10m+ | 2–6 weeks | Corporate facilities and flexible term loans | Institutional |

| 15 | AIB (UK) | £25k–£10m+ | 2–6 weeks | Corporate commercial loans, structured asset-backed lines | Institutional |

Tier 2 — Digital Challenger Banks

Fully regulated banks built tech-first. Combine the legal protections of a UK banking licence with API-driven onboarding, faster decisioning, and live data integrations. The fastest-growing share of the UK SME lending stack — they now write roughly 60% of gross SME bank lending versus 39% in 2012.

Sweet spot: £25k–£10m secured and unsecured loans, commercial mortgages, asset finance — digitally underwritten. Affiliate dynamics: Several operate dedicated broker portals; many primarily distribute through aggregator panels and accredited intermediary networks.

# | Lender | Loan Range | Speed | Specialism | Route |

| 16 | Starling Bank | £25k–£250k | 3–10 days | FCA-regulated, fast-tracked business loans and overdrafts | Aggregator |

| 17 | Monzo | £1k–£25k | Same day–48h | Micro-business loans, working capital overdrafts for sole traders | Institutional |

| 18 | Tide | £500–£200k | Same day–48h | Credit facilities, cash lines integrated with the SME accounting platform | Direct |

| 19 | Allica Bank | £250k–£5m | 3–10 days | Commercial mortgages and asset finance for established SMEs | Direct |

| 20 | OakNorth Bank | £250k–£50m | 3–10 days | Scale-up corporate debt, property development loans | Direct |

| 21 | Atom Bank | £100k–£5m | 3–10 days | Digital commercial mortgages, secured business loans | Direct |

| 22 | Shawbrook Bank | £25k–£50m | 3–10 days | Structured corporate, development, and specialist real estate finance | Direct |

| 23 | Revolut Business | £1k–£250k | Same day–48h | Corporate credit cards, merchant lines, multi-currency tools | Institutional |

| 24 | Cashplus Bank | £500–£20k | Same day–48h | Credit lines and short-term business cash cards | Institutional |

| 25 | Bunq Business | Multi-currency only | Same day–48h | European digital-first multi-currency business accounts | Institutional |

Tier 3 — Unsecured Alternative FinTechs

Algorithmic underwriting from accounting, banking and card-processor data. Speed is the product: decisions in hours, funds the same week. Pricing is higher than banks, but the credit box is wider — and they answer the calls banks no longer take.

Sweet spot: £1k–£1m unsecured working capital, growth funding, and revolving credit. Trading history thresholds are typically 6–12 months. Affiliate dynamics: Strongest affiliate density in the market. Most operate explicit broker programmes that pay commissions of 1–6% of the funded principal. This tier is the engine room of broker economics in the UK.

# | Lender | Loan Range | Speed | Specialism | Route |

| 26 | iwoca | £1k–£1m | Same day–48h | Flexi-loans with zero early-repayment fees, instant automated approvals | Direct |

| 27 | Funding Circle | £10k–£500k | 3–10 days | UK's largest online SME term-loan platform, deep broker API integration | Direct |

| 28 | Fleximize | £5k–£500k | 3–10 days | Customisable unsecured and secured loans, penalty-free early payoff | Direct |

| 29 | Capify | £5k–£500k | 3–10 days | Working capital loans for businesses with 6+ months of trading history | Direct |

| 30 | Boost Capital | £3k–£500k | Same day–48h | Fast, flexible short-term unsecured business loans | Direct |

| 31 | Uncapped | £10k–£10m | 3–10 days | Non-dilutive working capital for inventory, marketing, e-commerce scaling | Direct |

| 32 | Outfund | £10k–£10m | 3–10 days | Algorithmic funding for online businesses via direct data integrations | Direct |

| 33 | YouLend | £3k–£1m | Same day–48h | Embedded merchant financing via corporate checkout integrations | Direct |

| 34 | Esme Loans | £10k–£250k | Same day–48h | Digital automated unsecured lending, NatWest Group technology | Aggregator |

| 35 | Propl | £5k–£250k | Same day–48h | Tech-driven platform for unsecured expansion cash injections | Aggregator |

| 36 | Merchant Money | £5k–£300k | 3–10 days | Short-term unsecured business loans and bridge lines | Direct |

| 37 | Capital on Tap | £5k–£250k | Same day–48h | Business credit cards, revolving lines of credit | Direct |

| 38 | Sling | £500–£25k | Same day–48h | Fintech micro-lending for cash flow management | Aggregator |

| 39 | Nucleus Commercial Finance | £3k–£25m | 3–10 days | Property-backed and unsecured cash injections, full spectrum | Direct |

Tier 4 — Merchant Cash Advance (MCA) Providers

Capital advanced against future card sales. Repayments flex with revenue — quiet weeks repay less, busy weeks repay more. Built for hospitality, retail, beauty, and any business where card receipts are the dominant revenue rail. Factor rates (not APRs) apply; total cost is higher than secured debt, but speed and revenue flexibility offset it for the right operator.

Sweet spot: £3k–£500k advances against 3–18 months of card-processing history. Typical retrieval rate is 10–20% of daily card take. Affiliate dynamics: MCA is one of the most broker-driven product categories in UK finance. Commission structures are typically the most generous in the market — frequently 4–8% of the advance value paid to introducers.

# | Lender | Loan Range | Speed | Specialism | Route |

| 40 | Liberis | £1k–£300k | Same day–48h | Embedded revenue-based finance, BBB-backed | Direct |

| 41 | 365 Business Finance | £5k–£500k | Same day–48h | Specialist MCA provider with a strong broker network | Direct |

| 42 | YouLend MCA | £3k–£1m | Same day–48h | White-labelled revenue-linked advances via merchant gateways | Direct |

| 43 | SellersFi | £5k–£10m | 3–10 days | Cash advances and inventory funding for Amazon and online retail | Direct |

| 44 | QuickCapital | £3k–£300k | Same day–48h | Rapid merchant financing from card-machine processing volumes | Direct |

| 45 | Merchant Loan Advance | £3k–£250k | Same day–48h | MCA for hospitality, pubs, and high-street retail | Direct |

| 46 | Clearco UK | £10k–£10m | 3–10 days | Equity-free revenue-share advances for high-growth e-commerce | Direct |

| 47 | Vectis Finance | £5k–£250k | Same day–48h | Bespoke merchant card financing for seasonal retail | Direct |

| 48 | Funding Invoice MCA | £5k–£250k | Same day–48h | Blended asset-and-merchant cash tools for omni-channel retail | Direct |

Tier 5 — Asset Finance & Leasing Specialists

The highest-approval product category in UK SME lending — 96% of asset finance applications succeed, versus 44% for bank loans. The asset itself is the collateral, so credit boxes widen and decisions accelerate. Asset finance now represents around 40% of gross external business lending in the UK.

Sweet spot: £5k–£10m+ hire purchase, finance lease, operating lease, and refinance of existing assets — vehicles, plant, machinery, IT, agricultural, marine, aviation. Affiliate dynamics: Asset finance brokers are a regulated professional class with deep affiliate economics — NACFB-accredited intermediaries facilitated £33bn of SME lending in 2025, up 25% year-on-year, with asset finance the largest single category.

# | Lender | Loan Range | Speed | Specialism | Route |

| 49 | Lombard | £5k–£25m+ | 3–10 days | UK's premier asset finance brand, NatWest Group | Direct |

| 50 | White Oak UK | £25k–£10m+ | 3–10 days | Asset financing, vehicle leasing, and commercial term funding | Direct |

| 51 | Close Brothers Asset Finance | £10k–£10m+ | 3–10 days | Leasing and hire-purchase across engineering, print, aviation | Direct |

| 52 | Aldermore Bank | £25k–£5m | 3–10 days | Asset finance, invoice factoring, commercial property mortgages | Direct |

| 53 | Paragon Bank | £10k–£5m | 3–10 days | Commercial vehicles, plant machinery, technology upgrades | Direct |

| 54 | Haydock Finance | £5k–£1m | 3–10 days | Asset funding via a nationwide broker portal | Direct |

| 55 | Renaissance Asset Finance | £25k–£5m | 3–10 days | Premium asset financing for high-value equipment, luxury, fleets | Direct |

| 56 | Ultimate Finance | £10k–£5m | 3–10 days | Flexible asset leasing and cash flow funding | Direct |

| 57 | Compass Business Finance | £5k–£1m | 3–10 days | Independent specialist: manufacturing, print, packaging | Direct |

| 58 | Genesis Asset Finance | £5k–£500k | 3–10 days | Bespoke hire purchase and leasing for niche operations | Direct |

| 59 | Investec Asset Finance | £100k–£25m+ | 3–10 days | Corporate asset finance for industrial, infrastructure, healthcare | Direct |

| 60 | Propel Finance | £1k–£500k | Same day–48h | Asset finance tech engine for UK small business equipment | Direct |

| 61 | Shire Leasing | £1k–£500k | 3–10 days | Independent equipment leasing with a broker support framework | Direct |

| 62 | Bibby Asset Finance | £10k–£1m | 3–10 days | Asset refinancing for working capital extraction | Direct |

| 63 | Triple Point | £100k–£10m+ | 3–10 days | Impact-focused corporate asset leasing, public sector funding | Direct |

| 64 | Arkle Finance | £5k–£500k | 3–10 days | Asset funding from small operations to commercial property | Direct |

Tier 6 — Invoice Finance & Asset-Based Lending

Working capital is unlocked from the gap between sales and collections. Selective invoice discounting, whole-book factoring, confidential invoice discounting, and asset-based lending against debtor books, stock, plant, and property. The most underused product category given that UK B2B average days-to-pay continue to stretch.

Sweet spot: £10k–£25m+ advances of 70–90% of approved invoice value, released within 24 hours of invoicing. Affiliate dynamics: Invoice finance brokers operate a professional commission model — typically a percentage of the first-year service fee plus trailing commissions — the most annuity-like economics in commercial finance broking.

# | Lender | Loan Range | Speed | Specialism | Route |

| 65 | Bibby Financial Services | £25k–£25m | 3–10 days | Global leader: invoice factoring, discounting, supply chain finance | Direct |

| 66 | Novuna Business Finance | £50k–£10m | 3–10 days | Digital-first invoice discounting and asset finance | Direct |

| 67 | Pulse Cashflow Finance | £10k–£3m | 3–10 days | Selective and full invoice factoring for growth firms | Direct |

| 68 | Skipr | £10k–£1m | Same day–48h | Tech-forward digital invoice management and spot factoring | Direct |

| 69 | Penny | £5k–£500k | Same day–48h | App-based instant invoice funding for outstanding trade invoices | Direct |

| 70 | MarketFinance | £10k–£5m | 3–10 days | Selective invoice discounting paired with business loans | Direct |

| 71 | Sancus | £100k–£10m+ | 3–10 days | Working capital, supply chain financing, property bridging | Direct |

| 72 | Optimise Finance | £25k–£5m | 3–10 days | Independent specialist: invoice discounting | Direct |

| 73 | Satago | £10k–£1m | Same day–48h | All-in-one debtor tracking with selective invoice finance | Direct |

| 74 | Skipton Business Finance | £25k–£5m | 3–10 days | Invoice factoring backed by Skipton Building Society | Direct |

| 75 | Leisures Trust Cashflow | £25k–£3m | 3–10 days | Niche cash flow for travel, hospitality, and corporate supply | Direct |

| 76 | Peak Cashflow | £25k–£5m | 3–10 days | Independent working capital, asset-backed factoring | Direct |

| 77 | Advantedge Commercial Finance | £25k–£3m | 3–10 days | Invoice discounting with a nationwide regional footprint | Direct |

Tier 7 — Peer-to-Peer & Crowdlending Networks

Marketplace lending: institutional and private capital pooled into syndicated facilities, primarily property and SME term debt. Funding Circle alone holds a low-to-mid 50% share of UK non-bank business loan volumes — the category is no longer experimental, it is structural.

Sweet spot: £25k–£10m+ property-secured loans, development finance, bridging, and SME term debt. Affiliate dynamics: P2P platforms run formal Introducer Appointed Representative (IAR) and broker partner programmes with clear commission schedules and FCA-aligned compliance frameworks.

# | Lender | Loan Range | Speed | Specialism | Route |

| 78 | Folk2Folk | £100k–£5m | 3–10 days | UK's largest P2P land and property-backed lender for rural businesses | Direct |

| 79 | CrowdProperty | £100k–£10m | 3–10 days | P2P residential development bridge loans for property professionals | Direct |

| 80 | Proplend | £250k–£5m | 3–10 days | P2P commercial property mortgages, income-secured bridging | Direct |

| 81 | Assetz Capital | £100k–£10m+ | 3–10 days | Marketplace lending for housebuilders, developers, and commercial | Direct |

| 82 | Kuflink | £50k–£3m | 3–10 days | P2P real estate bridging loans with flexible drawdowns | Direct |

| 83 | Blend Network | £250k–£5m | 3–10 days | Bespoke P2P development funding for experienced developers | Direct |

Tier 8 — Regional, Community & Government-Backed

Patient capital with social-purpose mandates: regional development funds, community development financial institutions (CDFIs), the Start-Up Loans Company, and BBB-backed schemes. Often, the only source of capital for early-stage, underserved, or non-bankable propositions. Critical for under-£25k funding gaps where commercial economics do not work.

Sweet spot: £500–£250k personal loans for business use (Start-Up Loans), CDFI growth funding, and accredited Recovery Loan Scheme drawdowns. Affiliate dynamics: Delivery partners (Virgin StartUp, regional CDFIs) operate accredited introducer networks. Lower commission economics but higher conversion rates on first-time founders and disadvantaged demographics.

# | Lender | Loan Range | Speed | Specialism | Route |

| 84 | British Business Bank / Start-Up Loans | £500–£25k | 3–10 days | Government-backed 7.5% fixed-rate, <3 years trading | Direct |

| 85 | Virgin StartUp | £500–£25k | 3–10 days | Official Start-Up Loans delivery partner with mentoring | Direct |

| 86 | DSL Business Finance | £5k–£100k | 3–10 days | Not-for-profit micro-loans and growth funds for Scottish SMEs | Direct |

| 87 | GC Business Finance | £500–£100k | 3–10 days | North West regional lender for non-bankable firms | Direct |

| 88 | Enterprise Answers | £500–£50k | 3–10 days | Independent CDFI covering northern England | Direct |

| 89 | Finance for Enterprise | £500–£250k | 3–10 days | Regional lender across Yorkshire and the Midlands | Direct |

| 90 | Let's Do Business Group | £500–£100k | 3–10 days | Accredited enterprise agency for the South East coast | Direct |

| 91 | Borders Regional Development Fund | £5k–£100k | 3–10 days | Locally focused community finance for regeneration projects | Institutional |

| 92 | ART Business Loans | £10k–£150k | 3–10 days | Midlands CDFI: responsible business loans to sustain jobs | Direct |

| 93 | BCRS Business Loans | £10k–£150k | 3–10 days | Supportive finance for viable businesses across the West Midlands | Direct |

| 94 | Purbeck Personal Guarantee Insurance | Insurance product | 3–10 days | Specialist PG insurance underwriter for SME borrowers | Direct |

Tier 9 — Private Debt & Niche Specialist Lenders

The bespoke end of the market: private commercial banks, specialist real-estate lenders, hospitality finance, classic-vehicle asset specialists, and structured commercial credit lines for cases business banks underwrite poorly. Slower than fintech, but the relationship economics and structuring flexibility justify the cost for complex transactions.

Sweet spot: £500k–£50m+ bespoke commercial credit, structured property debt, classic vehicle, hospitality, and specialist real estate. Affiliate dynamics: Distribution is overwhelmingly through accredited specialist brokers — direct affiliate programmes are minimal, but commercial finance brokers that carry these lender panels command the highest fees in the market.

# | Lender | Loan Range | Speed | Specialism | Route |

| 95 | Fira Finance | £100k–£5m | 3–10 days | Cash flow credit for digital-first media and content studios | Direct |

| 96 | Arbuthnot Latham | £500k–£25m+ | 2–6 weeks | Private commercial banking, structured property and media debt | Institutional |

| 97 | Cynergy Bank | £100k–£10m | 3–10 days | Specialist business term loans, property acquisition finance | Direct |

| 98 | Cumberland Building Society | £100k–£5m | 2–6 weeks | Commercial property and hospitality mortgages, hotels, holiday lets | Direct |

| 99 | Cambridge & Counties Bank | £100k–£15m | 3–10 days | Specialist real estate investment, classic vehicle finance | Direct |

| 100 | Secure Trust Bank | £250k–£25m | 3–10 days | Comprehensive asset-based lending and real estate finance | Direct |

The Decision Framework

A 100-lender atlas is only as useful as the decision logic that routes any given borrower to the correct subset. This section provides three layers of decision support: a five-question diagnostic that narrows the field; a situation-to-tier matrix that maps common scenarios to recommended lender categories; and a set of frequent mistakes to avoid.

The Five-Question Diagnostic

Any borrower searching for capital can locate themselves on the lender map by answering five questions in order. Each answer eliminates tiers and concentrates the search.

- How much, and for what? Loan size, purpose, and whether the funds are asset-attached (equipment, vehicle, property) or general working capital.

- How fast? Same-week, same-month, or same-quarter — speed requirements rule out high-street banks at the top end and concentrate decisions into Tiers 3, 4, and 5.

- What security can you offer? Personal guarantee only, debtor book, fixed asset, real estate, or none. Security availability determines whether secured or unsecured products are viable.

- How long have you been trading, and what does your last 12 months look like? Under 6 months trading rules out Tiers 1–3 almost entirely; under 2 years narrows commercial debt to specialist tiers.

- What is your revenue rhythm? Steady B2B contracts favour invoice finance; lumpy or seasonal revenue favours revenue-based and merchant cash; project-driven income favours bridge and development finance.

Situation-to-Tier Matrix

Situation | Best-Fit Tier | Why | Secondary | Avoid |

| Established SME seeking a £500k+ commercial mortgage | Tier 1 or 2 | Lowest rates and longest repayment terms | Tier 9 private debt | Tier 4 MCA |

| £25k–£250k unsecured working capital, 1–3 years trading, decision in days | Tier 3 | Fast, algorithmic underwriting and same-week funding | Tier 7 P2P, Tier 8 Start-Up Loans | Tier 1 (slow) |

| Hospitality or retail with strong card sales needing £20k–£200k quickly | Tier 4 | Revenue-based repayments suit seasonal cash flow | Tier 3 unsecured | Tier 1 (will reject) |

| Equipment, machinery or vehicle finance (£10k–£5m) | Tier 5 | 96% approval rate with the asset as collateral | Tier 1 asset arms | Tier 4 (cost) |

| B2B business with a £250k+ debtor book | Tier 6 | Unlocks working capital from invoices, often within 24 hours | Tier 3 unsecured top-up | Tier 1 overdraft (declining) |

| Property development (£250k–£10m) | Tier 7 or 9 | Designed for development finance and structured lending | Tier 2 OakNorth, Shawbrook | Tier 1 (slow, restrictive) |

| Startup under 2 years trading needing <£25k | Tier 8 | Government-backed Start Up Loans (7.5% fixed) with mentoring | Tier 3 (if 6+ months trading) | Tier 1, 7, 9 |

| Complex £2m+ property or specialist transaction | Tier 9 | Bespoke structuring and private lending flexibility | Tier 2 OakNorth, Allica | Tier 1 (won't structure) |

| Rejected by a high-street bank | Bank Referral Scheme | Redirects businesses to approved alternative lenders | Direct application to Tier 3 | Giving up |

Five Costly Mistakes to Avoid

- Don't default to your existing bank. If you don't meet its lending criteria, you could lose 2–6 weeks. Identify the right lending tier before applying.

- Don't accept the first offer. SME finance pricing varies widely. Compare at least two or three quotes, ideally through broker or aggregator platforms.

- Don't overlook asset finance. With a 96% approval rate, it is often the most accessible and cost-effective option when funding equipment or vehicles.

- Understand factor rates vs. APR. Merchant cash advances often quote a factor rate rather than an APR. Always calculate the total repayment cost over the full term.

- Always use the Bank Referral Scheme. If declined by a major bank, accept the referral to a designated finance platform to maximise your chances of securing alternative funding.

Outlook 2026–2030

Five trends will shape UK business lending over the next five years.

1. Embedded finance becomes mainstream

Embedded finance—capital offered within platforms businesses already use—will become a dominant lending channel. Solutions from Shopify, Amazon Lending, Square, and YouLend are turning e-commerce, payment, and accounting platforms into loan-origination engines. As access becomes easier, transparent cost comparison will become even more important.

2. AI underwriting expands access to credit

AI-powered underwriting using open banking, accounting software, and alternative data will widen access to finance, particularly for SMEs overlooked by traditional credit scoring. UK fintech attracted £2.9 billion across 323 deals in the first three quarters of 2025, with AI playing an increasingly important role. Businesses with strong digital financial records will benefit most.

3. Specialist lenders continue to lead

Rather than consolidating, the market is becoming more specialised. OakNorth leads scale-up lending, Allica commercial mortgages, iwoca and Funding Circle unsecured finance, Liberis and YouLend embedded merchant finance, and Bibby invoice finance. Competition is increasingly driven by expertise within each niche.

4. High-street banks become more digital

Banks including NatWest, HSBC, and Lloyds are investing heavily in digital onboarding, APIs, and faster approvals. By 2030, the speed gap between traditional banks and challenger lenders is expected to narrow, strengthening competition across the market.

5. Regulation increases transparency

The FCA Consumer Duty and the continued evolution of the Bank Referral Scheme will raise standards for brokers, lenders, and finance platforms. Businesses that prioritise transparent comparisons, borrower outcomes, and clear disclosures will be best positioned to succeed. Businessabc.net's editorial-led approach aligns closely with this direction.

A Closing Reflection

Every business reflects the wider economy, and every funding decision shapes its future. Mapping the UK's lenders is, ultimately, mapping the choices available to entrepreneurs.

As Peter Diamandis argues, technology transforms scarcity into abundance. In UK business finance, that transformation is already underway. Capital that once required weeks of meetings and paperwork can now be accessed in hours through digital platforms and AI-driven underwriting.

Products once reserved for large corporations—invoice finance, asset finance, and structured lending—are now accessible to SMEs through faster, technology-enabled models. But access alone is not enough. Businesses still need trusted guidance to navigate an increasingly complex market.

This atlas aims to provide that guidance. Alongside professional brokers, lenders, and finance platforms, it helps turn an abundant but often opaque lending landscape into one that is transparent, accessible, and actionable.

For every business reading this with a funding question, the message is simple: the door you need exists. It is on this map. Walk through it.

Sources & Further Reading

- British Business Bank — Small Business Finance Markets 2025/26 report (March 2026).

- HM Treasury — Bank Referral Scheme: Official Statistics (gov.uk/government/collections/bank-referral-scheme-official-statistics).

- National Association of Commercial Finance Brokers (NACFB) — Annual Broker Statistics 2025.

- Financial Conduct Authority — Small Business Lending publications and the FCA-commissioned research, The Future of Funding for Small and Medium-Sized Enterprises in the UK.

- Bank of England — Money and Credit statistical releases (monthly).

- UK Finance — Quarterly SME Lending Data.

- Alternative Credit Investor — Non-bank lenders drive UK SME lending growth to £68bn (March 2026).

- Business Matters Magazine — Challenger banks hold 60% of SME lending as high street banks fight back (March 2026).

- Ken Research — UK FinTech SME Lending Market 2019–2030 outlook (January 2026).

- Funding Agent — UK SME Lending Statistics for 2026.

- Merchant Savvy — UK Business Finance Statistics (April 2026).

- Funding Options — fundingoptions.com (designated BRS platform).

- Funding Xchange — fundingxchange.co.uk (designated BRS platform).

- Alternative Business Funding — alternativebusinessfunding.co.uk (designated BRS platform).

- Swoop — swoopfunding.com (multi-lender aggregator).

- Tide Funding — tide.co/funding (SME platform aggregator).

Companion Reading — Ztudium Group Authored Works

- Guarda, Dinis — 4IR: AI, Blockchain, Fintech, IoT — Reinventing a Nation.

- Guarda, Dinis — The 5th Industrial Revolution.

- Guarda, Dinis — LifesDNA: The Longevity Atlas.

- IntelligentHQ.com — AI, Fintech and the Future of Banking series.

- HedgeThink.com — Alternative Credit Markets quarterly analysis.