business resources

The Transformative Role Of Artificial Intelligence In Fintech

AI is leveraging data like never before. From credit scoring that considers more than traditional metrics to robo-advisers providing personalised investment strategies, AI is enhancing financial products and services.

The fintech industry, currently valued at $340.1 billion globally, owes a significant portion of its momentum to AI, which alone accounts for a $44.08 billion market value as of 2023. Artificial intelligence (AI) in fintech has catalysed a paradigm shift, driving growth, innovation, and efficiency across financial services.

"The only thing that’s constant in fintech is change", says Piyush Gupta, CEO of DBS Group.

According to the industry analysis through 2023-28, AI in Fintech market is predicted to reach $49.43 Billion by 2028 with evolving fraud detection technologies.

Approximately 72% of companies leverage AI in at least one aspect of their business, including fraud detection, customer engagement, data analytics, and operational optimisation.

What is AI in Fintech?

Artificial Intelligence (AI) is transforming the fintech landscape by integrating advanced technologies such as machine learning (ML), natural language processing (NLP), and predictive analytics to revolutionise traditional financial operations. It has become a powerful tool for delivering tailored solutions, automating processes, and enhancing decision-making.

This creates a growing demand for a reliable Fintech app development company that can integrate AI solutions seamlessly into financial platforms.

Here are the underlying technologies that power AI applications in fintech:

Machine Learning (ML): With the largest contribution of 40%, ML is widely used in fraud detection, credit scoring, and algorithmic trading, where it identifies patterns and automates complex processes. Machine Learning (ML) drives innovation in fintech by analysing, predicting, and adapting to vast financial data. It processes structured and unstructured data to identify patterns and make intelligent predictions.

Preprocessing techniques, like normalisation and feature engineering, ensure raw data is usable for ML models. Supervised learning algorithms map inputs, such as historical trends, to outputs like price predictions, while unsupervised learning finds hidden patterns, including customer segments or anomalies. Advanced methods like reinforcement learning optimise decision-making by learning from feedback, and time-series models such as RNNs predict trends from sequential data. NLP processes financial text data, enabling sentiment analysis and document parsing.

ML systems adapt through incremental and online learning, ensuring models stay relevant. Techniques like ensemble learning combine models for accuracy, while probabilistic methods and deep learning tackle uncertainties and complex tasks. Scalability, interpretability, and API integrations further enhance ML's role, making it indispensable for fintech advancements.

Natural Language Processing (NLP): Accounting for 25%, NLP plays a crucial role in customer support through chatbots and virtual assistants, improving communication and customer experience.

Large Language Models (LLMs) and Natural Language Models (NLMs) are transforming the fintech industry by processing and generating human-like language while handling both structured and unstructured data. A key feature is Natural Language Understanding (NLU), where LLMs can read and understand financial documents, user queries, and texts. This allows them to interpret complex financial terms and context, improving efficiency.

LLMs use contextual embeddings, like BERT, to understand relationships between words, which helps in tasks like analysing market sentiment from news and reports. They also use Sequence-to-Sequence (Seq2Seq) models for summarising texts and generating responses to customer inputs.

Retrieval-augmented generation (RAG) helps LLMs fetch relevant real-time data, improving accuracy, especially when responding to queries needing up-to-date information. Pre-training on financial data enhances their sector knowledge. LLMs can also integrate text with numerical data, such as analysing earnings reports alongside financial figures. They learn from user feedback (Reinforcement Learning from Human Feedback), which adapts them to user needs and financial trends.

The efficiency of transformer-based models enables LLMs to process vast amounts of financial data quickly, turning complex information into accessible summaries. Few-shot and zero-shot learning allow them to adapt to new tasks with little extra training. They also represent and infer knowledge, helping synthesise financial insights and answer complex queries. These capabilities make LLMs and NLMs powerful tools for improving decision-making, data interpretation, and user engagement in the fintech sector.

Data Mining is crucial in fintech as it uncovers patterns and insights from large datasets, aiding better decisions and personalised services. It plays a key role in fraud detection by analysing transaction anomalies to identify suspicious activities. By segmenting customers based on their behaviour and demographics, fintech firms can customise products and services, improving customer engagement. Predictive analytics driven by data mining helps forecast market trends for investment strategies. It also streamlines credit scoring and loan approvals by efficiently assessing creditworthiness.

Computer Vision boosts automation, security, and customer experience in fintech by processing visual data like images and videos. It supports KYC compliance with document verification, uses facial recognition for secure authentication, and automates cheque processing. In fraud prevention, it detects tampered visuals and counterfeit documents. In insurance fintech, it assesses damages from uploaded images, while sentiment analysis during video calls provides deeper customer insights.

How AI and advanced tech is transforming the finance industry?

Advanced technologies are significantly transforming the finance industry, enhancing efficiency, personalisation, and security. Key technological advancements include:

Artificial Intelligence (AI) and Machine Learning (ML):

- Risk assessment and management: Financial institutions employ AI algorithms to analyse vast datasets, improving credit scoring accuracy and enabling proactive fraud detection. For instance, AI-driven systems can identify patterns indicative of fraudulent activities, allowing for swift intervention.

- Customer service enhancement: AI-powered chatbots and virtual assistants provide 24/7 customer support, addressing queries and facilitating transactions, thereby enhancing customer experience.

Blockchain and Distributed Ledger Technology (DLT):

- Transaction transparency and security: Blockchain ensures immutable and transparent records of transactions, reducing the need for intermediaries and enhancing trust in financial operations. This technology underpins cryptocurrencies and is being explored for various financial services, including cross-border payments and smart contracts.

- Decentralised Finance (DeFi): DeFi platforms leverage blockchain to offer financial services without central authorities, enabling peer-to-peer lending, borrowing, and trading, thus broadening access to financial services.

Cloud computing:

- Scalability and cost efficiency: Financial firms utilise cloud services to store and process large datasets, facilitating rapid scaling of operations and reducing infrastructure costs. This flexibility allows for the efficient deployment of new services and applications.

- Enhanced collaboration: Cloud platforms enable seamless collaboration across different departments and geographies, fostering innovation and improving time-to-market for financial products.

Big data analytics:

- Personalised financial products: By analysing customer data, financial institutions can tailor products and services to individual needs, enhancing customer satisfaction and loyalty. For example, AI-driven analytics can provide insights into spending patterns, enabling the offering of customised financial advice.

- Predictive analysis: Big data facilitates the forecasting of market trends and customer behaviours, aiding in strategic decision-making and risk management.

Robotic Process Automation (RPA):

- Operational efficiency: RPA automates repetitive tasks such as data entry and compliance reporting, reducing errors and freeing up human resources for more strategic activities. This leads to cost savings and improved accuracy in operations.

- Regulatory compliance: Automated systems ensure adherence to regulatory requirements by consistently monitoring and updating compliance protocols.

Cybersecurity Enhancements:

- Advanced threat detection: Utilising AI and ML, financial institutions can detect and respond to cyber threats in real-time, safeguarding sensitive financial data. For instance, AI-driven cybersecurity solutions monitor network behaviour to identify anomalies and prevent attacks such as phishing and ransomware.

- Secure authentication methods: The adoption of biometric verification and multi-factor authentication enhances the security of financial transactions.

Quantum Computing (Emerging):

- Complex problem solving: Quantum computing holds the potential to solve intricate financial problems, such as portfolio optimisation and risk analysis, at unprecedented speeds. While still in developmental stages, its future applications could revolutionise financial modelling and cryptography.

How is fintech different from finance?

Fintech (financial technology) is a sector that leverages technology to innovate and improve financial services. It focuses on streamlining operations, enhancing customer experience, and creating new financial products, distinguishing it from traditional finance in the following ways:

1. Technology Integration

- Fintech Approach: Fintech relies heavily on cutting-edge technologies such as Artificial Intelligence (AI), Blockchain, Internet of Things (IoT), Big Data, and Cloud Computing to develop smarter, faster, and more adaptive financial services.

- AI: Used for personalised financial advice, fraud detection, and predictive analytics.

- Blockchain: Facilitates secure, transparent transactions, including cryptocurrency trading and smart contracts.

- IoT: Enables payment systems embedded in devices, such as smartwatches and connected appliances.

- Traditional Finance Approach: Conventional financial institutions like banks rely on legacy systems, which are often decades old. These systems are less flexible, slower to adapt to new trends, and costly to upgrade. Processes like loan approvals and account management are often manual, requiring significant human intervention.

Example: A fintech app might provide instant loan approval through AI-driven credit scoring, while traditional banks could take days or weeks due to manual underwriting processes.

2. User-Centric Design

- Fintech Approach: Fintech companies design their products with a customer-first mindset, ensuring ease of use and accessibility. Mobile apps, chatbots, and intuitive user interfaces are commonplace, allowing customers to perform tasks like opening accounts, transferring money, or applying for loans in a few clicks.

- Features like real-time spending insights, gamified savings goals, and investment tracking enhance engagement.

- Fintech platforms also leverage multi-channel support (e.g., in-app chats, and social media) to offer seamless customer service.

- Traditional Finance Approach: Traditional finance focuses less on user experience and more on standardised procedures, often requiring customers to visit physical branches or navigate cumbersome online portals. The lack of personalised interaction and convenience limits their appeal, especially to tech-savvy and younger demographics.

Example: A fintech like Revolut provides an instant virtual card for online purchases directly after account creation, whereas a traditional bank may take days to issue a physical card.

3. Speed and Efficiency

- Fintech approach: Fintech platforms leverage automation to deliver fast and efficient services. Processes like opening an account, processing loans, or executing transactions are done in real-time, often without the need for human intervention.

AI-powered decision-making speeds up credit approvals, while blockchain ensures faster and more secure cross-border payments.

- Traditional finance approach: Traditional institutions are typically slower because they rely on paper-based processes, manual reviews, and multiple layers of authorisation. Even online banking options provided by traditional banks often mimic the slower workflows of their offline counterparts.

Example: Platforms like PayPal or Stripe allow merchants to accept payments globally in minutes, whereas traditional banks require lengthy onboarding procedures for merchant accounts.

4. Market Reach

- Fintech approach: Fintech leverages mobile-first and cloud-based solutions to reach underserved and unbanked populations, including those in rural or remote areas. By using alternative credit scoring methods, such as social media activity or smartphone usage patterns, fintech expands access to financial services like micro-loans and digital wallets.

These innovations make fintech a game-changer for emerging economies where access to traditional banking infrastructure is limited.

- Traditional finance approach: Traditional financial services often exclude those without formal employment, credit histories, or access to physical bank branches. Geographic and socioeconomic barriers limit their reach, leaving millions of people without access to essential financial services.

Example: A company like M-Pesa provides mobile money services to millions of people in Africa who do not have access to bank accounts, enabling them to save, transfer money, and pay bills directly from their phones.

Examples of AI-powered fintech tools & services

Alphasense: A financial research tool powered by AI, Alphasense uses natural language processing to extract insights from financial documents, news articles, and earnings calls. It assists investment professionals by identifying trends, key themes, and risks, streamlining their research processes. The platform’s advanced search capabilities enable users to make informed investment decisions more efficiently.

Zest AI: Zest AI specialises in enhancing credit underwriting through its machine learning models. It allows financial institutions to assess creditworthiness with greater accuracy and transparency, even for customers with limited credit history. By improving loan approval rates while maintaining risk standards, Zest AI helps lenders expand their customer base.

Klarna: The popular buy-now-pay-later service incorporates AI algorithms to personalise payment plans for users and assess credit risk in real time. Klarna also utilises machine learning for fraud detection, helping prevent unauthorised transactions while ensuring a seamless user experience.

Darktrace: Darktrace’s AI-driven cybersecurity solution protects financial institutions against evolving cyber threats. Its self-learning technology monitors network behaviour to identify anomalies and prevent attacks such as phishing, ransomware, and insider threats. Darktrace is widely adopted by banks and fintech companies to safeguard sensitive financial data.

Mint: Mint is an AI-powered personal finance management tool that aggregates data from multiple accounts to offer budgeting insights. It leverages machine learning to analyse spending patterns, provide personalised saving tips, and alert users to unusual account activity, helping them stay on top of their finances.

PayPal's Fraud Protection: PayPal employs advanced AI to detect and prevent fraudulent transactions across its platform. The system analyses millions of data points in real time, recognising patterns that indicate potentially suspicious activities. This ensures secure payments for both businesses and consumers.

Upstart: An AI-driven lending platform, Upstart evaluates loan applicants by analysing non-traditional data points such as education, employment history, and area of study. This innovative approach allows borrowers with thin credit histories to access loans while minimising default risk for lenders.

Stripe Radar: Integrated with Stripe’s payment processing service, Radar is an AI-based fraud prevention tool. It uses machine learning to detect and block fraudulent transactions, leveraging data from millions of businesses worldwide to improve accuracy and reduce false positives.

Finastra FusionFabric.cloud: Finastra’s open innovation platform combines AI and cloud technology to enable financial institutions to create and deploy customised fintech solutions. It supports tasks such as risk modelling, customer engagement, and loan underwriting while integrating seamlessly with existing systems.

Revolut: Revolut integrates AI across its services to offer features such as budgeting tools, instant spending alerts, and fraud prevention. Its AI algorithms analyse customer transactions in real time, flagging unusual activity and offering tailored financial insights to enhance user experience.

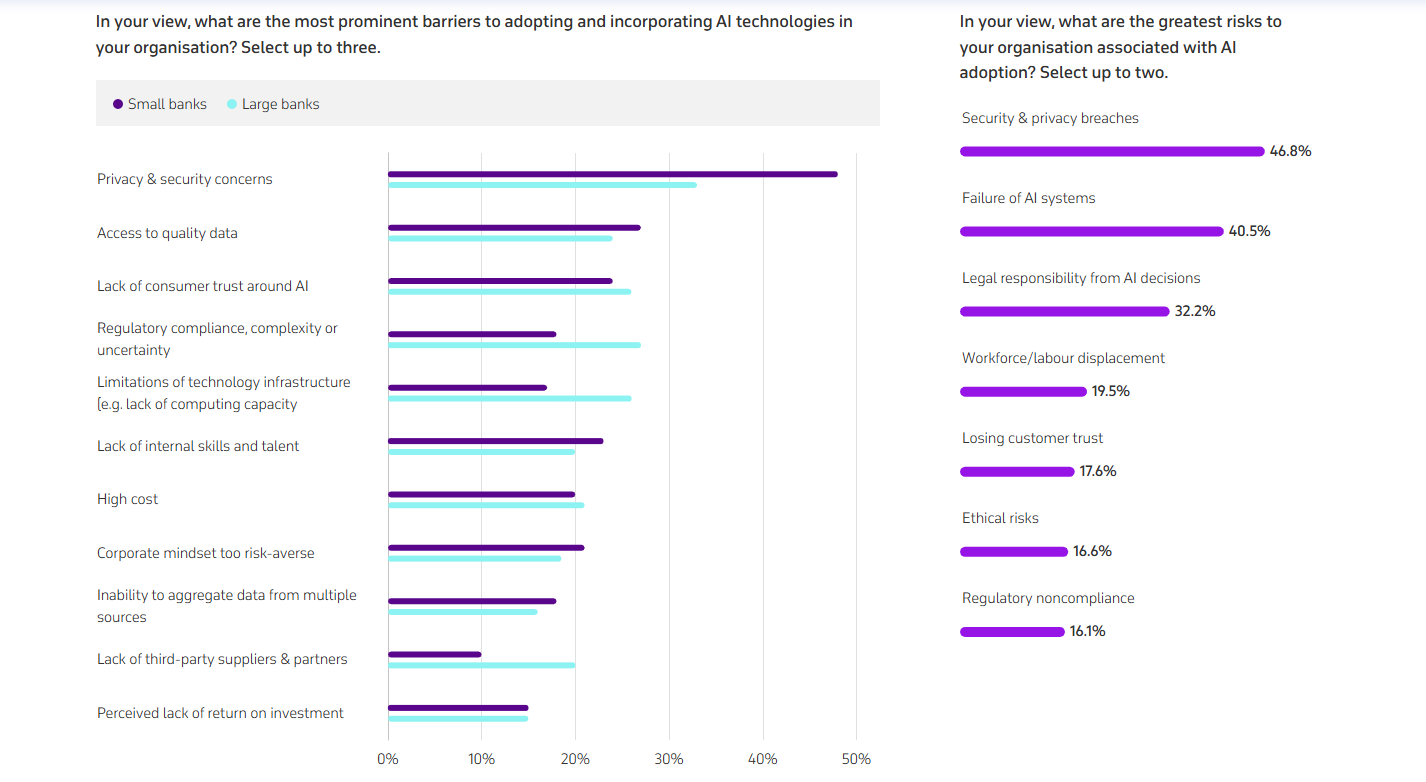

Common challenges of implementing AI in fintech

The integration of Artificial Intelligence (AI) into fintech has the potential to revolutionise the industry. However, it also presents significant challenges that financial institutions must address to successfully adopt and incorporate AI technologies. Below is a detailed breakdown of these challenges, along with case studies to illustrate each.

Credit: itransition

1. ROI & management buy-in

Challenge:

AI-powered solutions are often expensive, complex, and time-consuming to implement. They require substantial computational resources and lengthy training processes, making it difficult to justify the return on investment (ROI). Securing buy-in from stakeholders and executives is challenging due to budget constraints and the uncertainty of measurable outcomes.

Best practices:

- Engage AI consultants during the early project stages to evaluate costs and benefits.

- Prioritise AI applications that target critical inefficiencies or high-profit areas.

- Learn from early adopters’ initiatives and monitor AI trends.

The Commonwealth Bank of Australia (CBA) invested heavily in AI technologies to enhance operations. Their AI systems reduced call centre wait times by 40% and halved scam losses, showcasing tangible benefits that facilitated management buy-in for further AI initiatives.

2. Data & software integration

Challenge:

AI systems require seamless integration of structured and unstructured data from diverse sources. Inconsistent data formats and incompatible communication protocols often complicate the process.

Best practices:

- Use ETL pipelines to standardise and consolidate data into suitable storage systems.

- Leverage APIs and cloud-based services for efficient data exchange.

- Employ middleware or data virtualisation techniques for compatibility.

JPMorgan Chase developed an in-house AI tool, the LLM Suite, to enhance productivity across its workforce. The tool's integration into existing systems required careful planning to ensure it complemented current workflows, ultimately leading to increased efficiency and widespread adoption among employees.

3. Data processing and algorithm selection

Challenge:

Selecting the appropriate algorithms for specific tasks and managing the computational demands of deep learning models can be complex. Finance often requires maximum transparency, making black-box models like neural networks less ideal.

Best practices:

- Match algorithms to tasks (e.g., random forests for trend prediction, K-Means for customer segmentation).

- Use cloud-based AI platforms for scalable computing resources.

- Monitor and validate models for transparency and accuracy.

The Commonwealth Bank of Australia utilised AI to power its messaging services and live customer chats, enhancing customer service. This implementation required selecting suitable algorithms to process and respond to customer inquiries effectively.

4. AI model reliability

Challenge:

AI models require reliable, high-volume datasets for training. Overfitting, bias, and model drift can affect their performance. The lack of transparency in decision-making processes is another critical concern.

Best practices:

- Regularly retrain models with updated data.

- Use cross-validation and feature selection to minimise overfitting.

- Establish metrics to monitor performance during and after deployment.

BBVA integrated ChatGPT Enterprise to boost productivity, with 80% of users saving over two hours weekly. The bank continues to monitor and refine the AI's performance to maintain reliability and effectiveness.

5. Cybersecurity and compliance

Challenge:

AI implementation must comply with stringent data management standards and legislation, such as GDPR and PCI-DSS. Moreover, AI models are susceptible to cyber risks, including data breaches and adversarial attacks.

Best practices:

- Implement encryption, multi-factor authentication, and regular risk assessments.

- Train AI models on obfuscated or anonymised data.

- Develop data governance policies for secure data handling.

The National Australia Bank (NAB) is exploring AI applications while addressing potential risks, including data security and compliance with regulations. This proactive approach aims to mitigate cyber threats and ensure adherence to legal standards.

6. Skill gap and resistance to change

Challenge:

AI adoption often requires retraining staff and overcoming resistance to new technologies. A lack of skilled professionals in AI and machine learning compounds the problem.

Best practices:

- Invest in upskilling and retraining initiatives.

- Foster a culture of digital literacy through workshops and incentives.

- Establish centres of excellence to oversee AI adoption.

JPMorgan Chase's rollout of the LLM Suite fostered "healthy competition" among teams, encouraging adoption. The bank facilitated this transition through dedicated courses and superusers within teams, addressing skill gaps and resistance.

The future of fintech with AI

The evolution of artificial intelligence (AI) promises transformative advancements for the fintech industry, redefining how financial institutions operate, engage with customers, and address challenges. As AI continues to mature, its applications in fintech are poised to expand, fostering innovation and driving growth. Key future trends highlight the vast potential of AI in shaping the financial sector:

Hyper-personalisation: Meeting unique customer needs

AI is set to revolutionise personalisation in financial services by leveraging real-time data to predict and cater to individual customer needs. Advanced AI algorithms will analyse a combination of transactional data, spending habits, and life events to offer highly customised solutions. For instance, AI could proactively suggest investment opportunities or tailored savings plans based on a customer's unique financial goals and behaviours. This level of personalization not only enhances user satisfaction but also fosters deeper trust and loyalty, enabling financial institutions to differentiate themselves in a competitive market.

Advanced fraud detection: Staying ahead of cyber threats

As cyber criminals adopt increasingly sophisticated methods, AI will play a crucial role in fortifying the financial sector against fraud. Enhanced machine learning models will analyse vast datasets to identify subtle patterns indicative of fraudulent activity, enabling preemptive action. Real-time monitoring systems will evolve to detect and mitigate threats instantly, minimizing potential losses and safeguarding customer data. Additionally, AI-driven biometric authentication methods, such as facial recognition and voice analysis, will provide robust security measures, ensuring that financial transactions remain secure in an ever-changing threat landscape.

Predictive analytics: Enabling smarter decisions

AI will refine predictive analytics, providing deeper insights into market trends and customer behaviour. By processing massive amounts of historical and real-time data, AI systems will forecast economic shifts, enabling financial institutions to make informed investment decisions and effectively manage risks. Predictive analytics will also support portfolio optimisation by identifying high-potential opportunities and mitigating exposure to market volatility. This enhanced decision-making capability will empower both financial institutions and individual investors to navigate complex markets with greater confidence and precision.

Blockchain integration: Unlocking transparency and efficiency

The integration of AI with blockchain technology is expected to bring unparalleled transparency, security, and efficiency to financial transactions. AI algorithms can analyse blockchain data to detect anomalies, predict transaction trends, and enhance fraud prevention mechanisms. Blockchain, in turn, will ensure data integrity and create an immutable record of transactions, complementing AI’s analytical capabilities. Together, these technologies will streamline processes such as cross-border payments, smart contract execution, and supply chain financing, paving the way for a more reliable and efficient financial ecosystem.

Ethical AI development: Building trust and accountability

As AI adoption accelerates, there will be a growing emphasis on developing ethical and unbiased AI systems. Transparent and explainable AI models will be essential to building trust among users and regulators. Financial institutions will need to ensure that AI-driven decisions are fair, compliant with regulations, and free from unintended biases. This shift towards ethical AI will also involve robust oversight mechanisms, including regular audits and monitoring, to maintain accountability. The fintech industry can foster widespread acceptance and trust in AI-powered solutions by prioritising transparency and fairness.